Advertisement

Is Codan (ASX:CDA) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Codan Limited (ASX:CDA) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

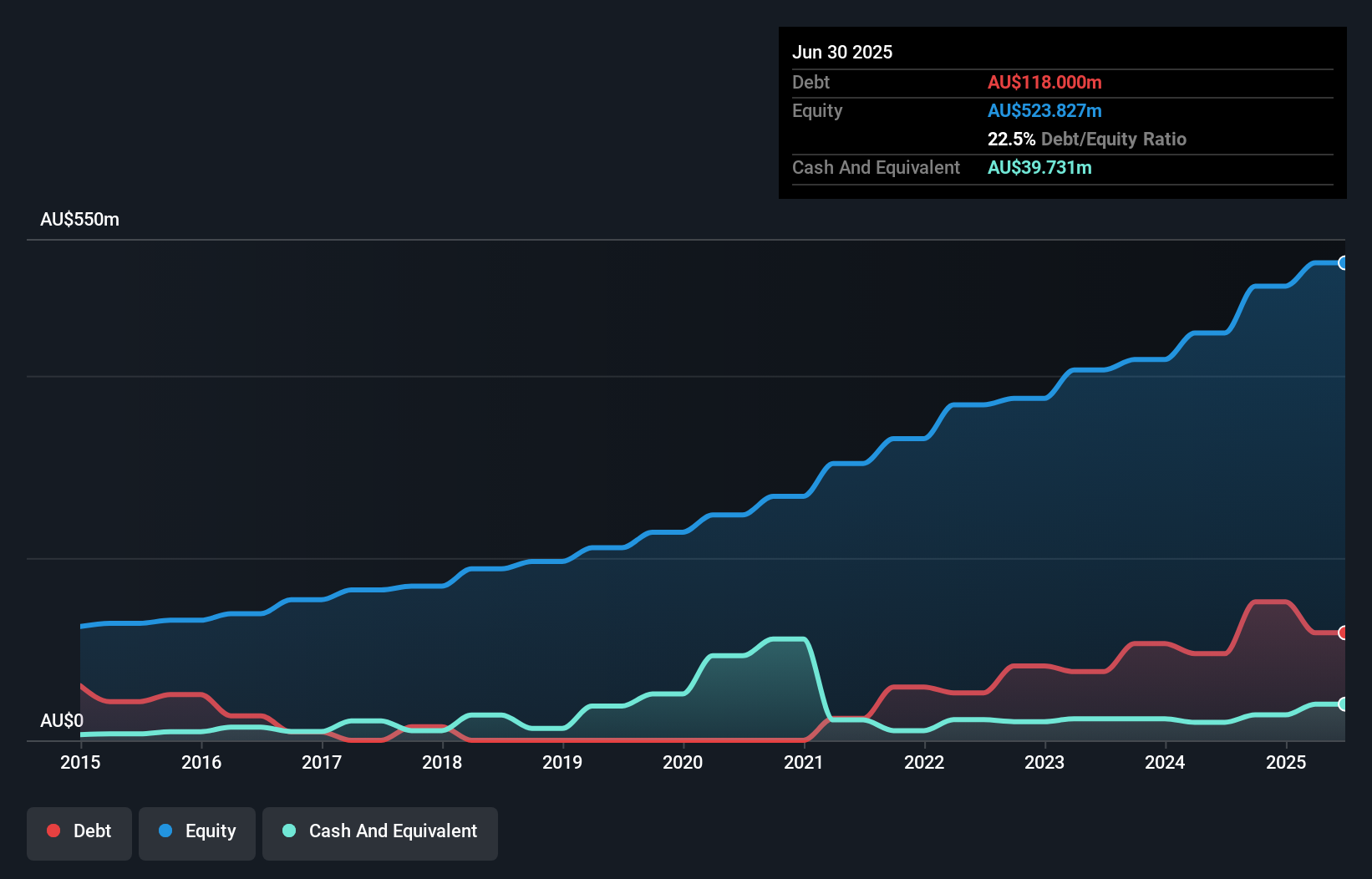

What Is Codan's Net Debt?

The image below, which you can click on for greater detail, shows that at June 2025 Codan had debt of AU$118.0m, up from AU$95.1m in one year. However, it also had AU$39.7m in cash, and so its net debt is AU$78.3m.

How Strong Is Codan's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Codan had liabilities of AU$194.0m due within 12 months and liabilities of AU$186.9m due beyond that. Offsetting this, it had AU$39.7m in cash and AU$121.4m in receivables that were due within 12 months. So its liabilities total AU$219.8m more than the combination of its cash and short-term receivables.

Of course, Codan has a market capitalization of AU$6.18b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Carrying virtually no net debt, Codan has a very light debt load indeed.

See our latest analysis for Codan

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Codan's net debt is only 0.50 times its EBITDA. And its EBIT easily covers its interest expense, being 12.1 times the size. So we're pretty relaxed about its super-conservative use of debt. Also positive, Codan grew its EBIT by 28% in the last year, and that should make it easier to pay down debt, going forward. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Codan's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Codan's free cash flow amounted to 48% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

The good news is that Codan's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its EBIT growth rate also supports that impression! Zooming out, Codan seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. Over time, share prices tend to follow earnings per share, so if you're interested in Codan, you may well want to click here to check an interactive graph of its earnings per share history.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CDA

Codan

Develops technology solutions for United Nations organizations, security and military agencies, government departments, corporates, individuals consumers, and small-scale miners.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1261.0% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

FU

FundamentalFlow on Vertiv Holdings Co ·

The Short and Long Term Compounder of Liquid Cooling industry.

Fair Value:US$45037.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2036.8% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on GQG Partners ·

The Cheap Genius Problem

Fair Value:AU$2.4541.2% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

Recently Updated Narratives

RC

rcb9 on Palantir Technologies ·

The Fifty-Five Percent Margin Is A Tax Holiday, Not The Business

Fair Value:US$91.8590.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KL

Klim on PetroTal ·

PetroTal: Betting On a Production Recovery

Fair Value:CA$0.8542.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_1211213 on Robo.ai ·

Robo.ai (AIIO): A Long-Term Bullish Technical Setup

Fair Value:US$5.6447.2% undervalued

1 followerusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

294 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.0% overvalued

156 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.7% undervalued

177 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0