Advertisement

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

So, the natural question for Urbanise.com (ASX:UBN) shareholders is whether they should be concerned by its rate of cash burn. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Urbanise.com

When Might Urbanise.com Run Out Of Money?

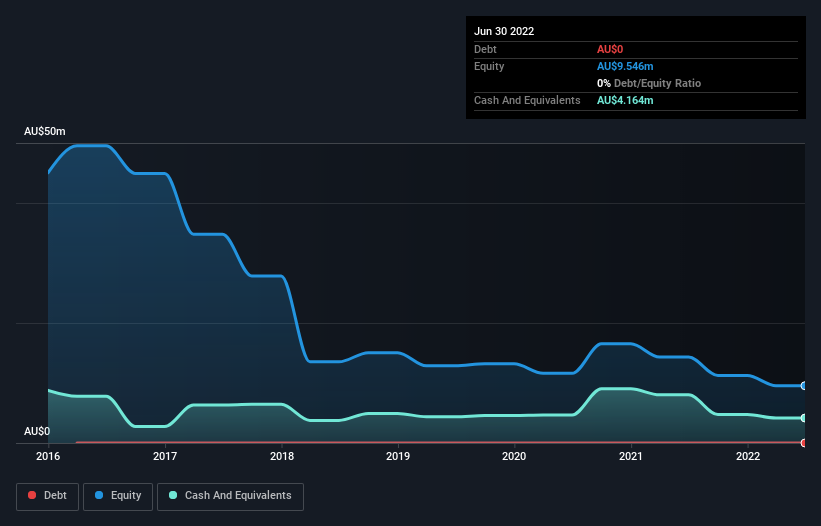

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Urbanise.com last reported its balance sheet in June 2022, it had zero debt and cash worth AU$4.2m. In the last year, its cash burn was AU$3.8m. Therefore, from June 2022 it had roughly 13 months of cash runway. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Urbanise.com Growing?

At first glance it's a bit worrying to see that Urbanise.com actually boosted its cash burn by 18%, year on year. At least the revenue was up 10% during the period, even if it wasn't up by much. In light of the data above, we're fairly sanguine about the business growth trajectory. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic earnings and revenue shows how Urbanise.com is building its business over time.

How Easily Can Urbanise.com Raise Cash?

Even though it seems like Urbanise.com is developing its business nicely, we still like to consider how easily it could raise more money to accelerate growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Urbanise.com has a market capitalisation of AU$43m and burnt through AU$3.8m last year, which is 8.9% of the company's market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

Is Urbanise.com's Cash Burn A Worry?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Urbanise.com's cash burn relative to its market cap was relatively promising. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. Taking a deeper dive, we've spotted 3 warning signs for Urbanise.com you should be aware of, and 2 of them are significant.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:UBN

Urbanise.com

Designs and develops cloud-based software platforms in the Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative