Wayne Arthur is the CEO of Skyfii Limited (ASX:SKF), and in this article, we analyze the executive's compensation package with respect to the overall performance of the company. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Skyfii.

See our latest analysis for Skyfii

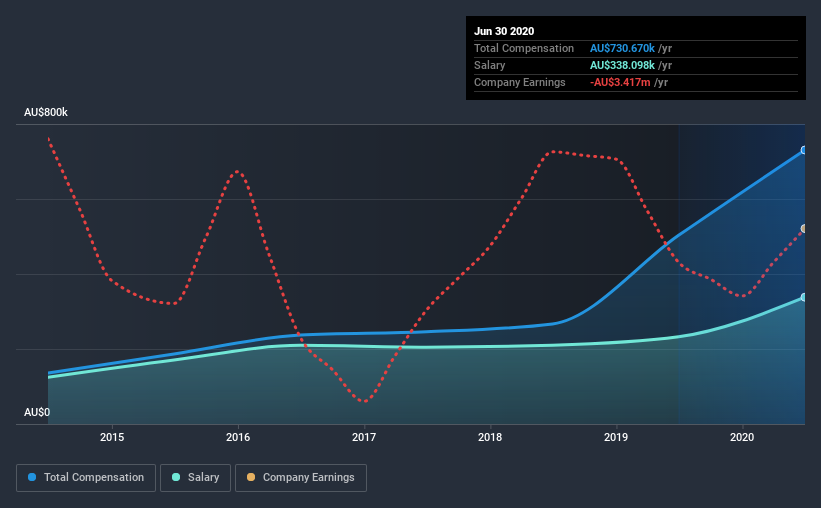

How Does Total Compensation For Wayne Arthur Compare With Other Companies In The Industry?

Our data indicates that Skyfii Limited has a market capitalization of AU$70m, and total annual CEO compensation was reported as AU$731k for the year to June 2020. That's a notable increase of 45% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$338k.

In comparison with other companies in the industry with market capitalizations under AU$263m, the reported median total CEO compensation was AU$334k. Hence, we can conclude that Wayne Arthur is remunerated higher than the industry median. Moreover, Wayne Arthur also holds AU$2.3m worth of Skyfii stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$338k | AU$233k | 46% |

| Other | AU$393k | AU$271k | 54% |

| Total Compensation | AU$731k | AU$503k | 100% |

On an industry level, roughly 59% of total compensation represents salary and 41% is other remuneration. Skyfii pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Skyfii Limited's Growth Numbers

Skyfii Limited has seen its earnings per share (EPS) increase by 14% a year over the past three years. Its revenue is up 44% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Skyfii Limited Been A Good Investment?

Most shareholders would probably be pleased with Skyfii Limited for providing a total return of 74% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

As we noted earlier, Skyfii pays its CEO higher than the norm for similar-sized companies belonging to the same industry. But EPS growth and shareholder returns have been top-notch for the past three years. Considering such exceptional results for the company, we'd venture to say CEO compensation is fair. Given the strong history of shareholder returns, the shareholders are probably very happy with Wayne's performance.

CEO compensation can have a massive impact on performance, but it's just one element. That's why we did some digging and identified 2 warning signs for Skyfii that you should be aware of before investing.

Important note: Skyfii is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

When trading Skyfii or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Beonic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:BEO

Beonic

Provides data analytics services in the Asia Pacific, the Americas, Europe, the Middle East, and Africa.

Mediocre balance sheet with low risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)