Had insiders known MOQ Limited (ASX:MOQ) would hit AU$23m they might have invested more last year

Last week, MOQ Limited (ASX:MOQ) insiders, who had purchased shares in the previous 12 months were rewarded handsomely. The shares increased by 25% last week, resulting in a AU$4.7m increase in the company's market worth. In other words, the original AU$180k purchase is now worth AU$225k.

Although we don't think shareholders should simply follow insider transactions, we would consider it foolish to ignore insider transactions altogether.

Check out our latest analysis for MOQ

The Last 12 Months Of Insider Transactions At MOQ

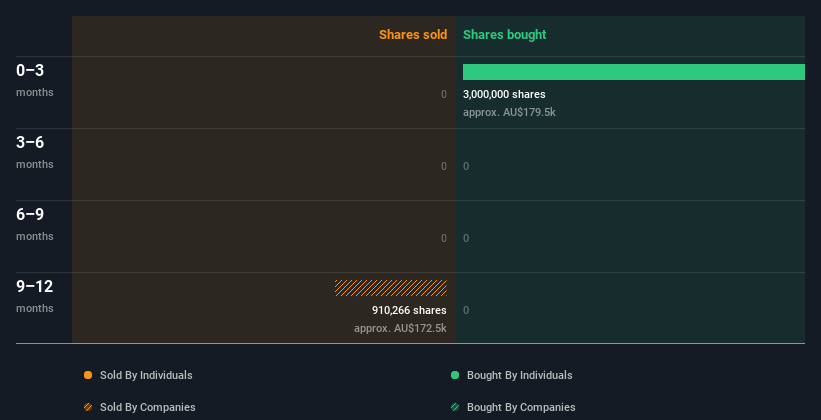

Notably, that recent purchase by David Stevens is the biggest insider purchase of MOQ shares that we've seen in the last year. Even though the purchase was made at a significantly lower price than the recent price (AU$0.075), we still think insider buying is a positive. Because it occurred at a lower valuation, it doesn't tell us much about whether insiders might find today's price attractive.

You can see a visual depiction of insider transactions (by companies and individuals) over the last 12 months, below. If you want to know exactly who sold, for how much, and when, simply click on the graph below!

MOQ is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Insider Ownership of MOQ

I like to look at how many shares insiders own in a company, to help inform my view of how aligned they are with insiders. I reckon it's a good sign if insiders own a significant number of shares in the company. It's great to see that MOQ insiders own 44% of the company, worth about AU$10m. This kind of significant ownership by insiders does generally increase the chance that the company is run in the interest of all shareholders.

What Might The Insider Transactions At MOQ Tell Us?

It's certainly positive to see the recent insider purchase. And an analysis of the transactions over the last year also gives us confidence. However, we note that the company didn't make a profit over the last twelve months, which makes us cautious. Once you factor in the high insider ownership, it certainly seems like insiders are positive about MOQ. One for the watchlist, at least! While we like knowing what's going on with the insider's ownership and transactions, we make sure to also consider what risks are facing a stock before making any investment decision. At Simply Wall St, we've found that MOQ has 5 warning signs (4 make us uncomfortable!) that deserve your attention before going any further with your analysis.

But note: MOQ may not be the best stock to buy. So take a peek at this free list of interesting companies with high ROE and low debt.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions, but not derivative transactions.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:MOQ

MOQ

MOQ Limited develops, builds, and acquires cloud focused technology businesses in Australia.

Mediocre balance sheet and slightly overvalued.

Market Insights

Community Narratives