- Australia

- /

- Specialty Stores

- /

- ASX:NCK

Nick Scali (ASX:NCK) Is Paying Out A Larger Dividend Than Last Year

Nick Scali Limited (ASX:NCK) has announced that it will be increasing its dividend on the 25th of October to AU$0.25. Based on the announced payment, the dividend yield for the company will be 5.6%, which is fairly typical for the industry.

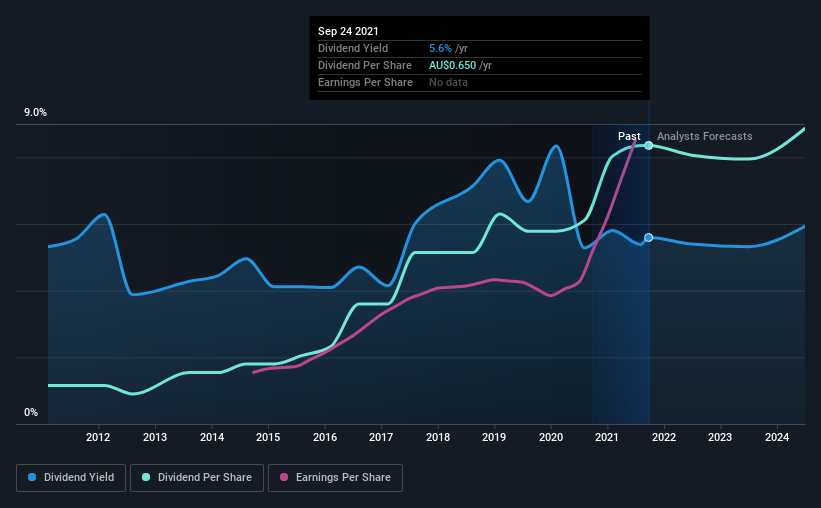

See our latest analysis for Nick Scali

Nick Scali Doesn't Earn Enough To Cover Its Payments

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Prior to this announcement, Nick Scali's dividend was comfortably covered by both cash flow and earnings. This means that a large portion of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to fall by 22.8% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 98%, which could put the dividend in jeopardy if the company's earnings don't improve.

Dividend Volatility

The company's dividend history has been marked by instability, with at least 1 cut in the last 10 years. The first annual payment during the last 10 years was AU$0.09 in 2011, and the most recent fiscal year payment was AU$0.65. This means that it has been growing its distributions at 22% per annum over that time. Nick Scali has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Nick Scali has seen EPS rising for the last five years, at 26% per annum. Nick Scali is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

We Really Like Nick Scali's Dividend

Overall, a dividend increase is always good, and we think that Nick Scali is a strong income stock thanks to its track record and growing earnings. The earnings easily cover the company's distributions, and the company is generating plenty of cash. However, it is worth noting that the earnings are expected to fall over the next year, which may not change the long term outlook, but could affect the dividend payment in the next 12 months. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Just as an example, we've come across 2 warning signs for Nick Scali you should be aware of, and 1 of them can't be ignored. If you are a dividend investor, you might also want to look at our curated list of high performing dividend stock.

If you decide to trade Nick Scali, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Nick Scali might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:NCK

Nick Scali

Engages in the sourcing and retailing of household furniture and related accessories in Australia, New Zealand, and the United Kingdom.

Excellent balance sheet with reasonable growth potential and pays a dividend.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)