Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Bapcor Limited (ASX:BAP) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Bapcor

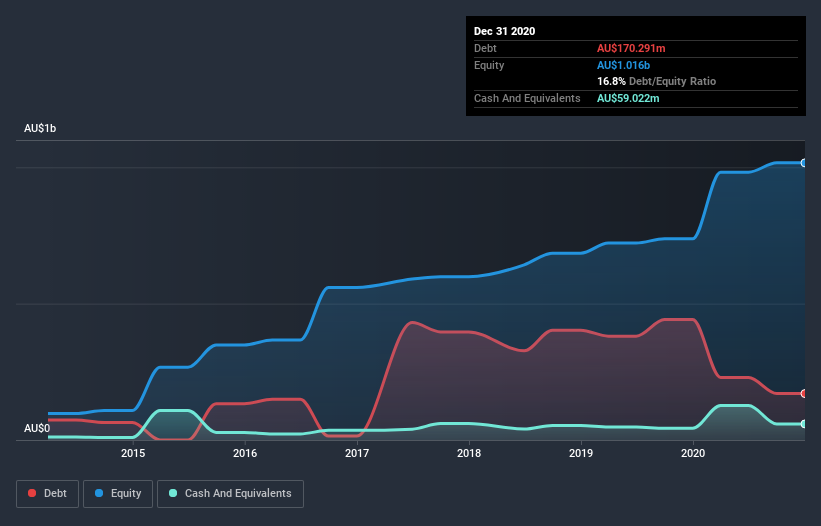

How Much Debt Does Bapcor Carry?

As you can see below, Bapcor had AU$170.3m of debt at December 2020, down from AU$441.4m a year prior. However, it does have AU$59.0m in cash offsetting this, leading to net debt of about AU$111.3m.

A Look At Bapcor's Liabilities

Zooming in on the latest balance sheet data, we can see that Bapcor had liabilities of AU$360.3m due within 12 months and liabilities of AU$312.6m due beyond that. Offsetting this, it had AU$59.0m in cash and AU$147.4m in receivables that were due within 12 months. So its liabilities total AU$466.4m more than the combination of its cash and short-term receivables.

Of course, Bapcor has a market capitalization of AU$2.51b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

With net debt sitting at just 0.58 times EBITDA, Bapcor is arguably pretty conservatively geared. And it boasts interest cover of 10.0 times, which is more than adequate. Also good is that Bapcor grew its EBIT at 13% over the last year, further increasing its ability to manage debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Bapcor can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. During the last three years, Bapcor produced sturdy free cash flow equating to 64% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Bapcor's net debt to EBITDA suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And that's just the beginning of the good news since its interest cover is also very heartening. Taking all this data into account, it seems to us that Bapcor takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Bapcor you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Bapcor, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bapcor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:BAP

Bapcor

Engages in the sale and distribution of vehicle parts, accessories, automotive equipment, and services and solutions in Australia, New Zealand, and Thailand.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor