Advertisement

- Australia

- /

- Capital Markets

- /

- ASX:HMC

3 ASX Stocks Trading At Up To 46.3% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the Australian market has risen 1.1%, and over the past 12 months, it is up 11%, with earnings forecasted to grow by 13% annually. In this favorable environment, identifying undervalued stocks can present significant opportunities for investors looking to capitalize on potential growth.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Regal Partners (ASX:RPL) | A$3.39 | A$6.77 | 49.9% |

| Hansen Technologies (ASX:HSN) | A$4.21 | A$8.20 | 48.7% |

| IPH (ASX:IPH) | A$6.18 | A$11.54 | 46.4% |

| Ansell (ASX:ANN) | A$29.55 | A$56.92 | 48.1% |

| Shine Justice (ASX:SHJ) | A$0.71 | A$1.34 | 47% |

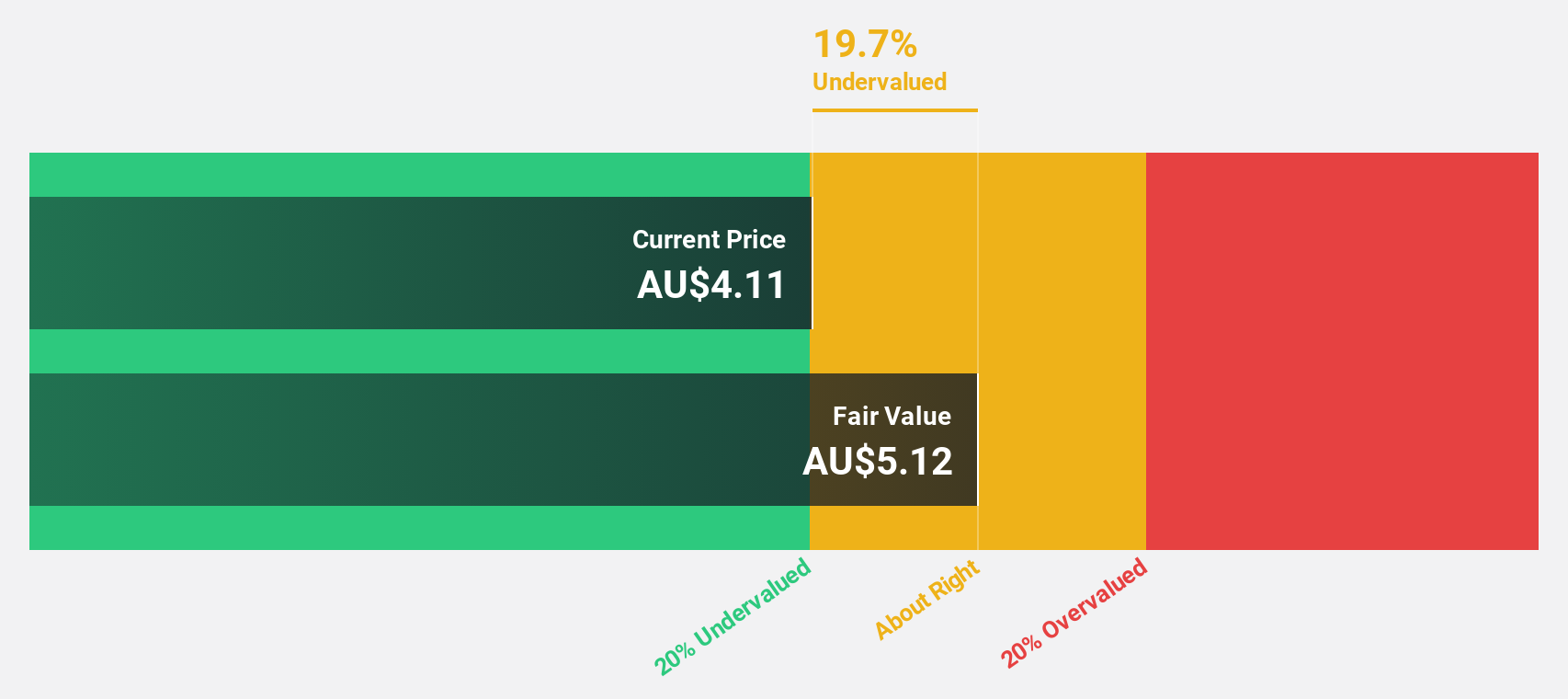

| HMC Capital (ASX:HMC) | A$8.31 | A$15.47 | 46.3% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Little Green Pharma (ASX:LGP) | A$0.091 | A$0.17 | 46.3% |

| Airtasker (ASX:ART) | A$0.265 | A$0.52 | 49.4% |

| Superloop (ASX:SLC) | A$1.71 | A$3.31 | 48.4% |

Underneath we present a selection of stocks filtered out by our screen.

HMC Capital (ASX:HMC)

Overview: HMC Capital Limited, with a market cap of A$3.14 billion, owns and manages real estate-focused funds in Australia through its subsidiaries.

Operations: HMC Capital generates revenue primarily from real estate at A$77.60 million, supplemented by private equity at A$3.50 million.

Estimated Discount To Fair Value: 46.3%

HMC Capital reported earnings of A$66 million and sales of A$81.1 million for the year ended June 30, 2024, showing solid growth from the previous year. Trading at A$8.31, it is significantly undervalued compared to its estimated fair value of A$15.47. Although shareholders faced dilution recently, HMC's revenue is forecast to grow by over 20% annually, outpacing market averages and indicating strong future cash flows despite a modest return on equity forecast of 9.5%.

- Our expertly prepared growth report on HMC Capital implies its future financial outlook may be stronger than recent results.

- Take a closer look at HMC Capital's balance sheet health here in our report.

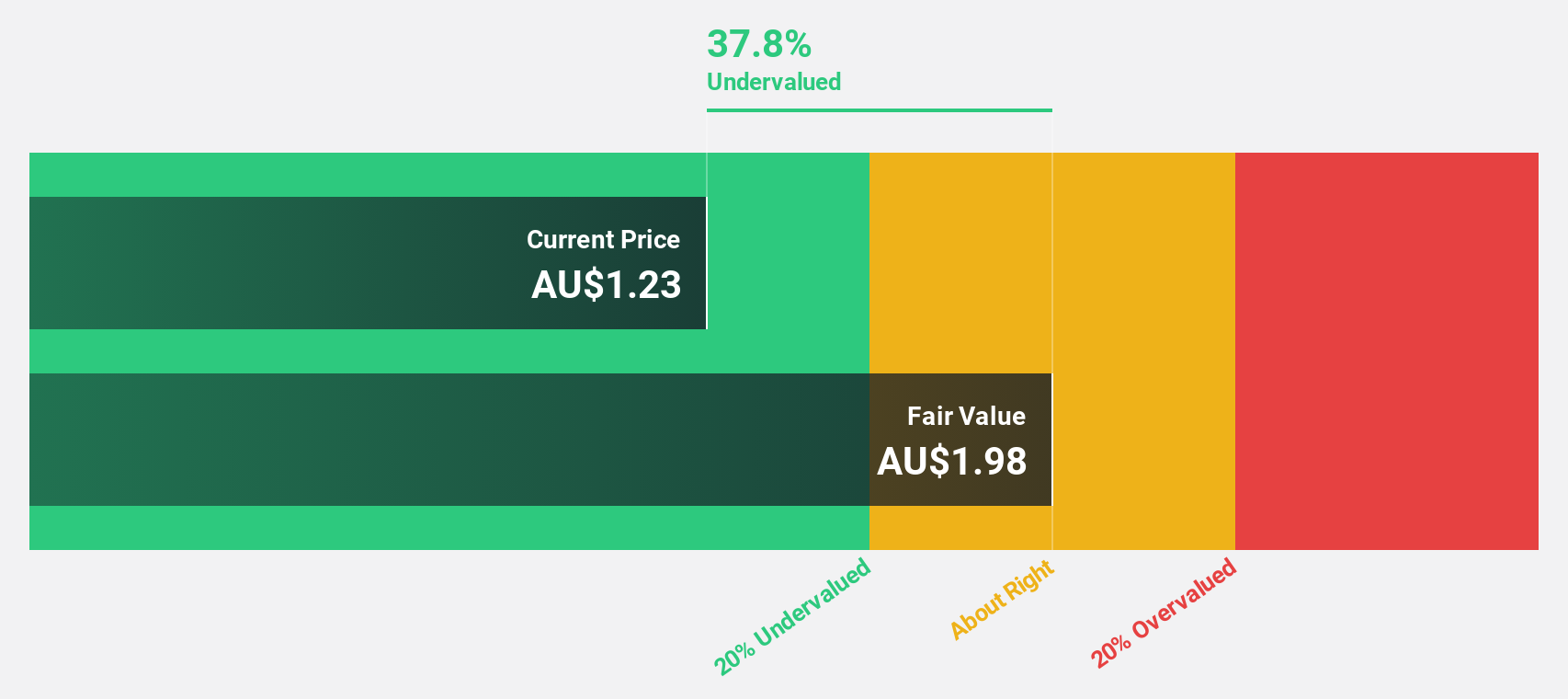

Infomedia (ASX:IFM)

Overview: Infomedia Ltd (ASX:IFM) is a technology company that develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide, with a market cap of A$657.61 million.

Operations: Revenue from publishing periodicals amounts to A$140.83 million.

Estimated Discount To Fair Value: 25.8%

Infomedia Ltd reported full-year sales of A$140.83 million, up from A$129.91 million last year, with net income rising to A$12.68 million from A$9.58 million. Trading at A$1.76, it is significantly undervalued compared to its estimated fair value of A$2.37 and shows strong cash flow potential with earnings expected to grow 28.7% annually over the next three years, outpacing the broader Australian market's growth forecast of 12.8%.

- Our growth report here indicates Infomedia may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Infomedia.

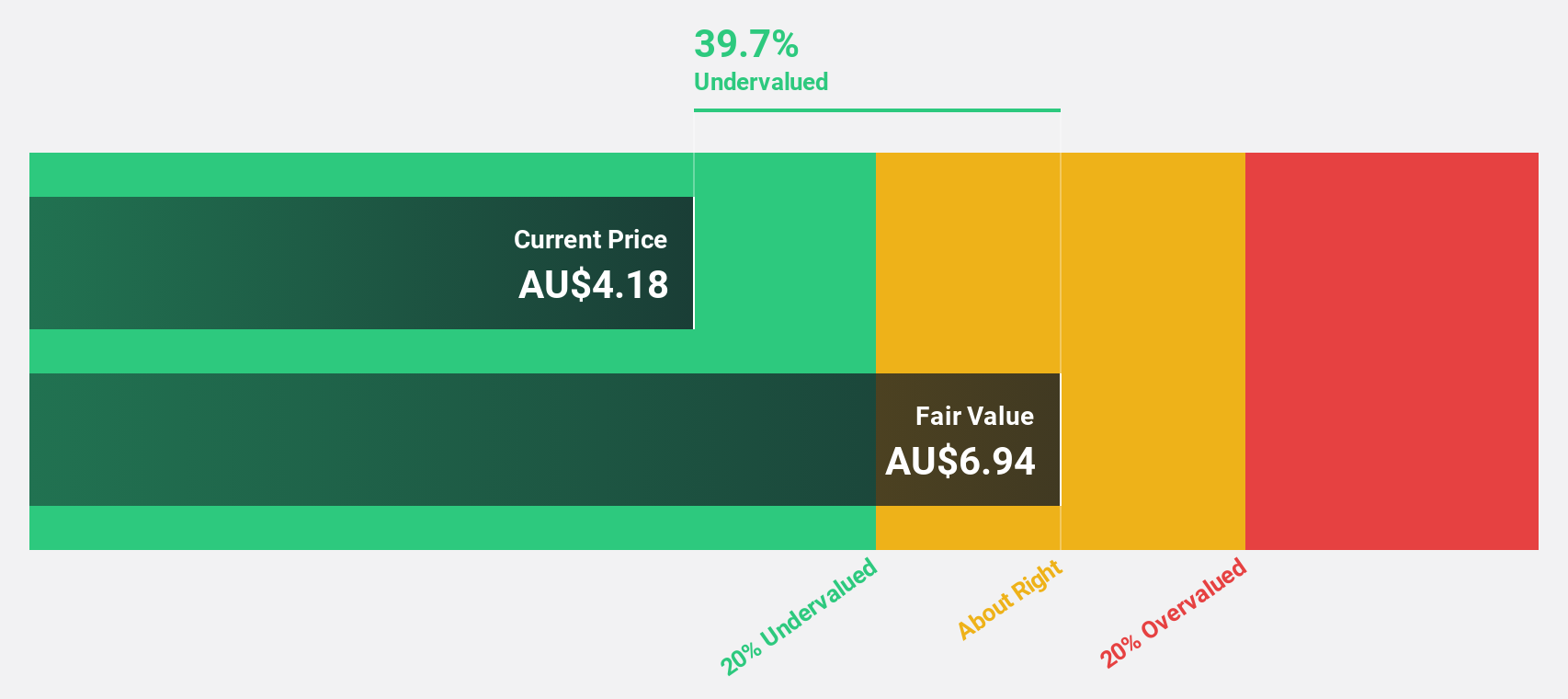

Nanosonics (ASX:NAN)

Overview: Nanosonics Limited, with a market cap of A$975.65 million, operates as an infection prevention company globally.

Operations: The company's revenue primarily comes from its Healthcare Equipment segment, generating A$170.01 million.

Estimated Discount To Fair Value: 37%

Nanosonics Limited's recent earnings report showed sales of A$170.01 million and net income of A$12.97 million, down from A$19.88 million last year. Trading at A$3.22, it is significantly undervalued compared to its estimated fair value of A$5.11 and is forecasted to grow earnings by 22.3% annually, which is faster than the Australian market average of 12.8%. However, profit margins have decreased from 12% to 7.6%.

- In light of our recent growth report, it seems possible that Nanosonics' financial performance will exceed current levels.

- Get an in-depth perspective on Nanosonics' balance sheet by reading our health report here.

Where To Now?

- Click this link to deep-dive into the 43 companies within our Undervalued ASX Stocks Based On Cash Flows screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HMC Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:HMC

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor