Advertisement

Telix Pharmaceuticals (ASX:TLX) Boosts Growth with Cardinal Health Alliance and New FDA Submissions

Simply Wall St

Reviewed by Simply Wall St

Telix Pharmaceuticals (ASX:TLX) is experiencing significant growth and strategic advancements, yet faces notable market and operational challenges. Recent developments include a substantial 65% revenue increase and ambitious future projections, contrasted with high valuation concerns and reimbursement hurdles. In the discussion that follows, we will explore Telix's core strengths, critical weaknesses, growth opportunities, and potential threats to provide a comprehensive overview of the company's current business situation.

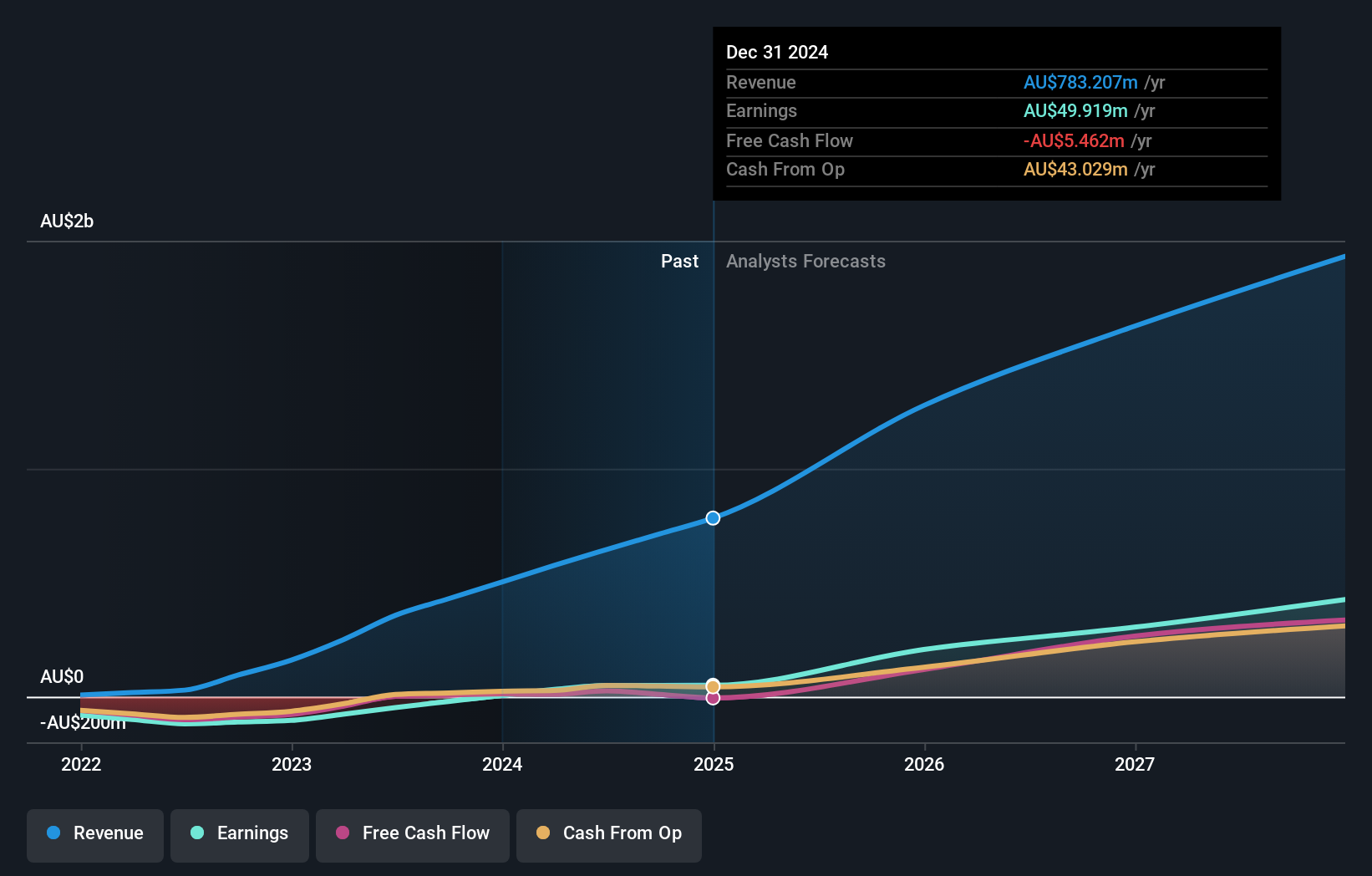

Get an in-depth perspective on Telix Pharmaceuticals's performance by reading our analysis here.

Strengths: Core Advantages Driving Sustained Success For Telix Pharmaceuticals

Telix Pharmaceuticals has demonstrated strong financial health with a 65% improvement in revenue in the first half of 2024 compared to the prior year, as noted by Darren Smith, Group Chief Financial Officer. The company raised its revenue guidance by 10% to a range of $745 million to $776 million, reflecting a 50% increase over last year's revenue. This growth is supported by strategic investments in future growth and innovation, such as the Phase III ProstACT GLOBAL study and the FDA approval for the 591 asset. The company's strong market position is further evidenced by the success of Illuccix, which continues to gain market share in the United States. Despite trading below its estimated fair value of A$44.56, Telix's current share price is less than 20% higher than the target price, indicating potential overvaluation based on its high price-to-earnings ratio of 141.2x compared to industry and peer averages.

To dive deeper into how Telix Pharmaceuticals's valuation metrics are shaping its market position, check out our detailed analysis of Telix Pharmaceuticals's Valuation.Weaknesses: Critical Issues Affecting Telix Pharmaceuticals's Performance and Areas For Growth

Telix faces significant market challenges, particularly in the U.S. reimbursement environment, as highlighted by CEO Christian Behrenbruch. The company has seen clinical utilization of its products expand, leading to an increase in the total addressable market estimates by 60% to $2.4 billion. However, operational risks remain, with substantial investments back into pipeline development, such as the $136 million reinvested from the $175 million generated by the commercial business. Additionally, Telix is considered expensive with a price-to-earnings ratio of 141.2x compared to the Global Biotechs industry average of 26.5x and the peer average of 22.1x. This overvaluation could pose a challenge in attracting new investors despite the company's profitability.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Telix Pharmaceuticals is well-positioned to leverage growth opportunities through global expansion and strategic initiatives. The company plans to launch three new imaging agents in the U.S., which is expected to sustain market share growth and expand the addressable market. Regulatory changes also present opportunities, with positive feedback on the ZIRCON data for European submission. The company's strategic alliances, such as the agreement with Cardinal Health for the distribution of Zircaix, further enhance its market position. Additionally, the submission of a New Drug Application for TLX101-CDx to the FDA, granted Orphan Drug and Fast Track designation, underscores Telix's commitment to addressing unmet medical needs and capitalizing on emerging opportunities in precision oncology.

To gain deeper insights into Telix Pharmaceuticals's historical performance, explore our detailed analysis of past performance.Threats: Key Risks and Challenges That Could Impact Telix Pharmaceuticals's Success

Telix faces several threats, including competition and supply chain issues, particularly around copper-64, which Christian Behrenbruch believes are underappreciated by the market. Economic factors also pose risks, with the majority of Pluvicto therapies selected with an Illuccix scan, indicating dependency on specific products. Regulatory issues remain a concern, as highlighted by the delta in capital raise expectations between the F1 and the convertible bond. Furthermore, shareholders have experienced dilution, with total shares outstanding growing by 4.6% over the past year. These external factors could potentially impact Telix's growth and market share, necessitating strategic management to navigate these challenges effectively.

Conclusion

Telix Pharmaceuticals has shown significant financial growth and strategic advancements, such as a 65% revenue increase and successful product launches like Illuccix. However, the company faces challenges, including high operational costs and a price-to-earnings ratio of 141.2x, which is considerably higher than the industry average of 26.5x and peer average of 22.1x. This high ratio, combined with a share price that is less than 20% higher than the target price, suggests that the stock might be expensive relative to its earnings. While Telix has strong growth prospects through global expansion and regulatory approvals, it must effectively manage competitive pressures, supply chain issues, and shareholder dilution to sustain its market position and future performance.

Key Takeaways

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Telix Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ASX:TLX

Telix Pharmaceuticals

A commercial-stage biopharmaceutical company, focuses on the development and commercialization of therapeutic and diagnostic radiopharmaceuticals for cancer and rare diseases in Australia, Belgium, Japan, Switzerland, and the United States.

High growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor