Advertisement

- Australia

- /

- Life Sciences

- /

- ASX:PIQ

Here's Why We Think Proteomics International Laboratories Limited's (ASX:PIQ) CEO Compensation Looks Fair for the time being

Performance at Proteomics International Laboratories Limited (ASX:PIQ) has been reasonably good and CEO Richard Lipscombe has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 24 November 2022. We present our case of why we think CEO compensation looks fair.

Check out the opportunities and risks within the AU Life Sciences industry.

How Does Total Compensation For Richard Lipscombe Compare With Other Companies In The Industry?

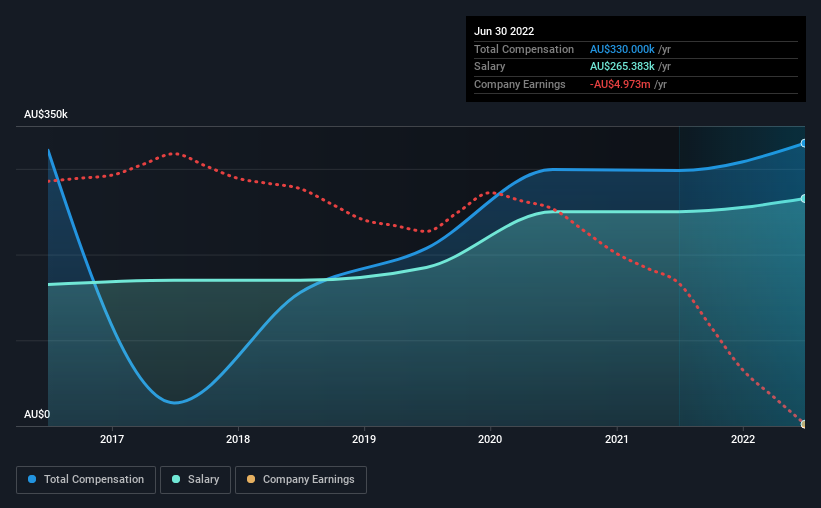

At the time of writing, our data shows that Proteomics International Laboratories Limited has a market capitalization of AU$104m, and reported total annual CEO compensation of AU$330k for the year to June 2022. Notably, that's an increase of 11% over the year before. Notably, the salary which is AU$265.4k, represents most of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations under AU$296m, the reported median total CEO compensation was AU$425k. This suggests that Proteomics International Laboratories remunerates its CEO largely in line with the industry average. Furthermore, Richard Lipscombe directly owns AU$17m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$265k | AU$250k | 80% |

| Other | AU$65k | AU$48k | 20% |

| Total Compensation | AU$330k | AU$298k | 100% |

On an industry level, around 80% of total compensation represents salary and 20% is other remuneration. There isn't a significant difference between Proteomics International Laboratories and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Proteomics International Laboratories Limited's Growth Numbers

Proteomics International Laboratories Limited has reduced its earnings per share by 30% a year over the last three years. Its revenue is up 25% over the last year.

The reduction in EPS, over three years, is arguably concerning. On the other hand, the strong revenue growth suggests the business is growing. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Proteomics International Laboratories Limited Been A Good Investment?

Most shareholders would probably be pleased with Proteomics International Laboratories Limited for providing a total return of 187% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

The overall company performance has been commendable, however there are still areas for improvement. We reckon that there are some shareholders who may be hesitant to increase CEO pay further until EPS growth starts to improve, despite the robust revenue growth.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 4 warning signs (and 1 which doesn't sit too well with us) in Proteomics International Laboratories we think you should know about.

Important note: Proteomics International Laboratories is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PIQ

Proteomics International Laboratories

Operates as a medical technology company with a focus on the area of proteomics in Australia, New Zealand, the United States, Europe, India, and Southeast Asia.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.9% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|21.8% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.6% undervalued

TR

Community Contributor