Amid a backdrop of mixed economic signals from both Australia and China, the ASX200 has shown modest fluctuations. With events like the Future of Mining conference highlighting sector opportunities, investors remain keenly focused on market dynamics. In this context, growth companies with high insider ownership can offer a compelling narrative as they often suggest confidence from those closest to the company's operations and future prospects.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Hartshead Resources (ASX:HHR) | 13.9% | 86.3% |

| Cettire (ASX:CTT) | 28.7% | 30.1% |

| Gratifii (ASX:GTI) | 14.3% | 112.4% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Doctor Care Anywhere Group (ASX:DOC) | 28.4% | 96.4% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Change Financial (ASX:CCA) | 26.6% | 85.4% |

| Botanix Pharmaceuticals (ASX:BOT) | 11.4% | 120.9% |

| Liontown Resources (ASX:LTR) | 16.4% | 63.9% |

Let's take a closer look at a couple of our picks from the screened companies.

Botanix Pharmaceuticals (ASX:BOT)

Simply Wall St Growth Rating: ★★★★★★

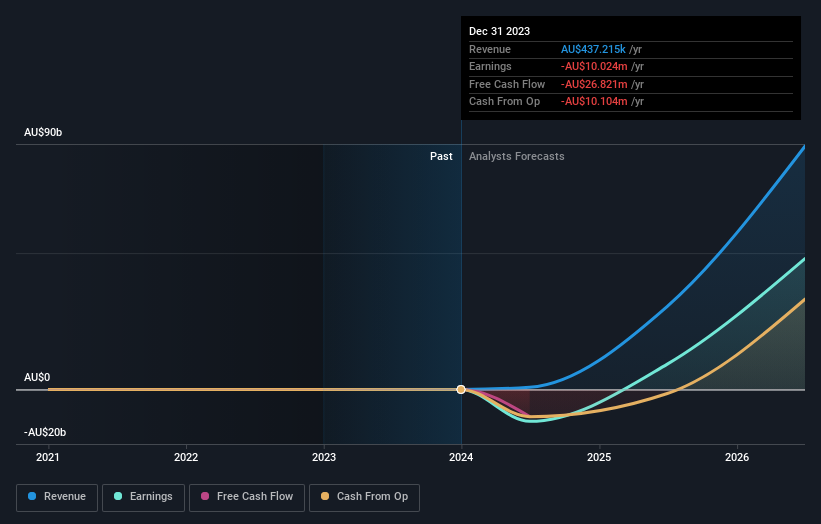

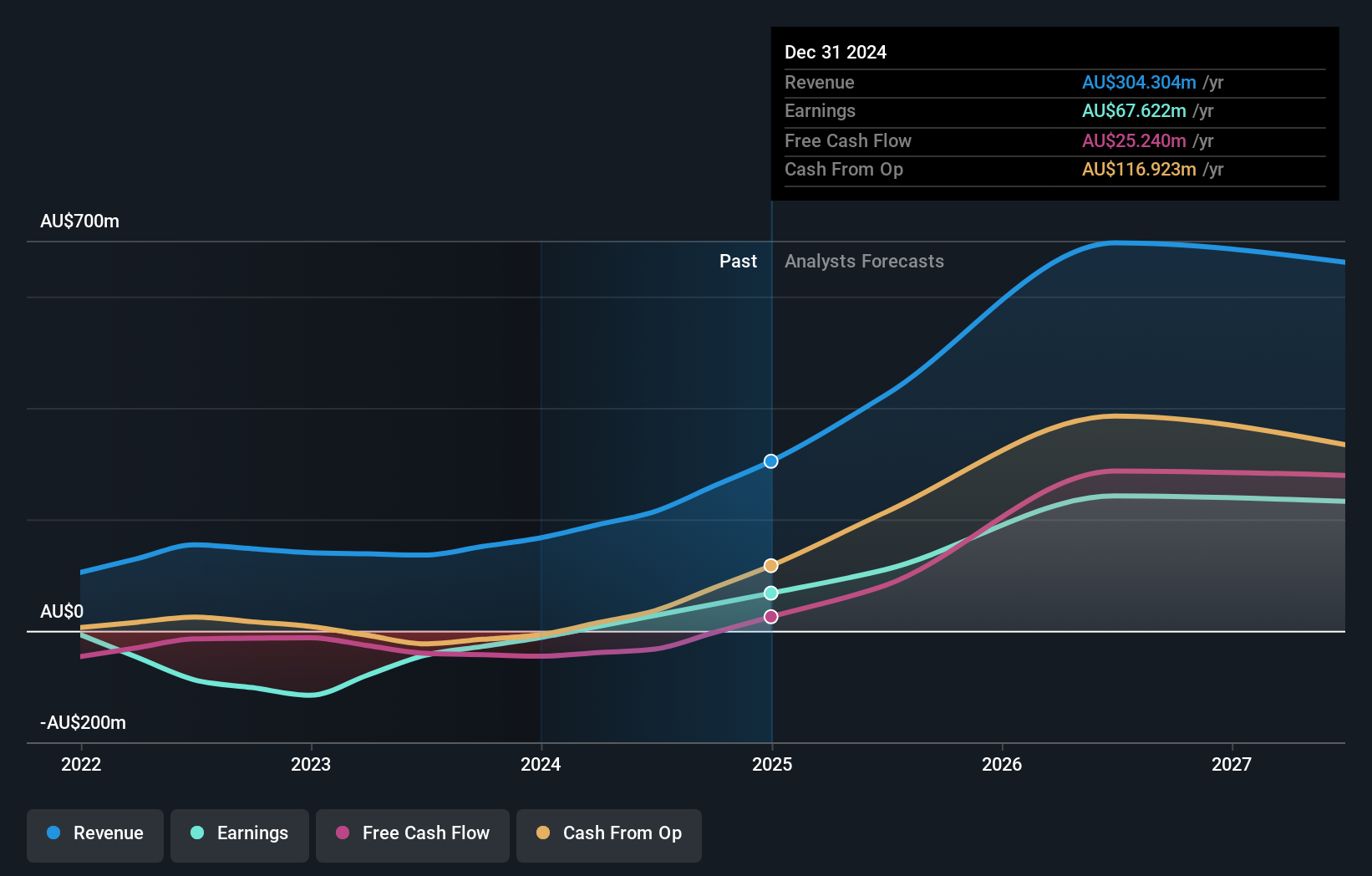

Overview: Botanix Pharmaceuticals Limited, based in Australia, focuses on the research and development of dermatology and antimicrobial products, with a market capitalization of approximately A$519.80 million.

Operations: The company generates revenue primarily from its dermatology and antimicrobial product development activities, totaling A$0.44 million.

Insider Ownership: 11.4%

Botanix Pharmaceuticals, with modest annual revenues of A$437K, is anticipated to see a sharp revenue increase at 120.4% annually, outpacing the broader Australian market's 5.4%. Despite recent shareholder dilution and limited financial reserves providing less than a year of cash runway, the company's earnings could grow substantially by 120.89% per year. Botanix is also nearing regulatory approval for SofdraÔ, as indicated in their latest update on commercial launch plans and market insights shared on May 6, 2024.

- Delve into the full analysis future growth report here for a deeper understanding of Botanix Pharmaceuticals.

- Upon reviewing our latest valuation report, Botanix Pharmaceuticals' share price might be too optimistic.

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across various regions including Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of approximately A$4.30 billion.

Operations: The company generates revenue through its leisure and corporate travel services, with segment earnings of A$1.28 billion and A$1.06 billion respectively.

Insider Ownership: 13.3%

Flight Centre Travel Group, trading 21.2% below its estimated fair value, shows promise with a forecasted revenue growth of 9.7% per year, outpacing the Australian market's average of 5.4%. Its earnings are expected to increase by 18.81% annually, also exceeding the national trend of 13.7%. Additionally, a projected Return on Equity of 21.7% in three years underscores its potential for robust financial health amidst no significant insider trading activity recently reported.

- Unlock comprehensive insights into our analysis of Flight Centre Travel Group stock in this growth report.

- Our valuation report here indicates Flight Centre Travel Group may be undervalued.

Ora Banda Mining (ASX:OBM)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ora Banda Mining Limited is an Australian company focused on the exploration, operation, and development of mineral properties, with a market capitalization of approximately A$705.51 million.

Operations: The primary revenue source for the company is gold mining, generating A$166.66 million.

Insider Ownership: 10.2%

Ora Banda Mining is anticipated to grow its revenue by 41.9% annually, significantly outstripping the Australian market's average of 5.4%. Despite shareholder dilution over the past year, the company's earnings could surge by approximately 93.57% per year. Positioned at a compelling 91.7% below its estimated fair value, Ora Banda is expected to reach profitability within three years, a rate considered above average compared to market growth, though recent insider trading data is unavailable.

- Click to explore a detailed breakdown of our findings in Ora Banda Mining's earnings growth report.

- Upon reviewing our latest valuation report, Ora Banda Mining's share price might be too pessimistic.

Turning Ideas Into Actions

- Delve into our full catalog of 90 Fast Growing ASX Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Botanix Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:BOT

Botanix Pharmaceuticals

Engages in the research and development of dermatology and antimicrobial products in Australia and the United States.

Exceptional growth potential with excellent balance sheet.