- Australia

- /

- Metals and Mining

- /

- ASX:FMG

Fortescue (ASX:FMG) Reports USD 5.7B Net Profit, Declares AUD 0.89 Dividend Amid Strong Financial Health

Fortescue(ASX:FMG) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a notable 31.2% increase in dividend payouts and innovative product launches, juxtaposed against a 16.7% drop in Q2 net sales and inflationary pressures. In the discussion that follows, we will delve into Fortescue's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

Delve into the full analysis report here for a deeper understanding of Fortescue

Strengths: Core Advantages Driving Sustained Success For Fortescue

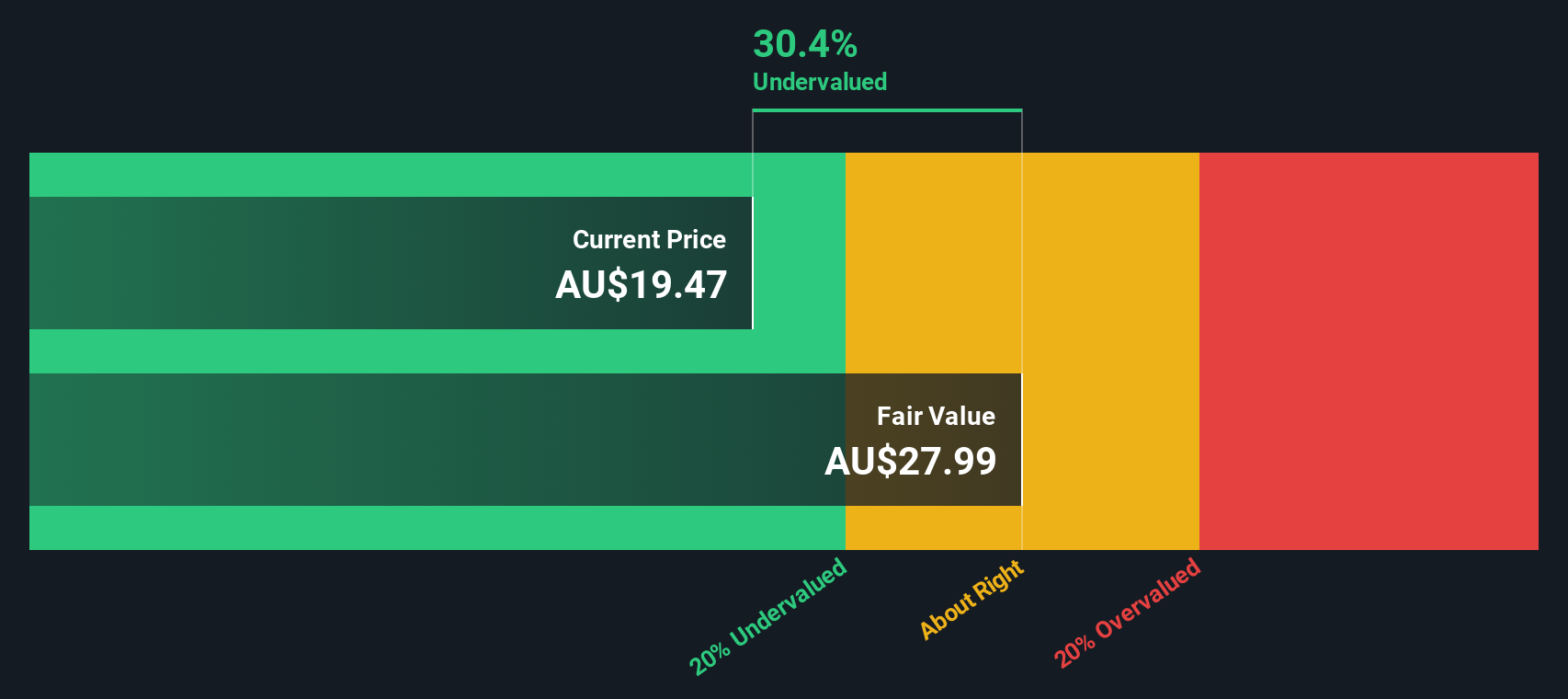

Fortescue has demonstrated robust financial health, achieving full-year shipments of 191.6 million tonnes while maintaining an industry-leading cost position with a Hematite C1 of AUD 18.24 per tonne, as highlighted by Chief Operating Officer Dino Otranto. This operational efficiency has contributed to the third-highest earnings and second-highest free cash flow in the company's history. Net profit after tax reached USD 5.7 billion, reflecting strong profitability, as noted by CFO Apple Paget. Additionally, the Board declared a final dividend of AUD 0.89 per share, representing distributions to shareholders of AUD 6.1 billion, further underscoring financial stability. Fortescue's Price-To-Earnings Ratio of 6.4x, below the peer average of 9.6x and industry average of 15.2x, indicates it is undervalued compared to its peers and the market, enhancing its market positioning.

Weaknesses: Critical Issues Affecting Fortescue's Performance and Areas For Growth

Despite its strengths, Fortescue faces several critical issues. The company has experienced challenges with the Raw Water Pipeline, as mentioned by Dino Otranto. Additionally, the increase in depreciation and amortization expenses, due to higher sustaining CapEx and the commissioning of new assets, presents financial challenges. CFO Apple Paget noted that the higher income tax expense reflects both higher statutory earnings before tax and a higher effective tax rate. Furthermore, Fortescue's management team is relatively inexperienced, with an average tenure of just one year. This could impact strategic decision-making and long-term planning. To gain insights into how these weaknesses could impact Fortescue's financial stability, explore our section on Fortescue's Past Performance.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Fortescue has several strategic opportunities to enhance its market position. The company is focusing on developing a new, green industry in Australia, with significant growth potential in Green Metals. Dino Otranto highlighted the aim to produce over 1,500 tonnes per annum of higher than 95% green metal, with first production anticipated next year. Additionally, Fortescue has an exciting exploration pipeline with programs underway in Argentina, Peru, and Brazil, which could diversify its revenue streams. CEO Richard Hutchinson emphasized the company's steadfast targets to be achieved by 2030, which could further strengthen its competitive advantage. Learn more about how these opportunities could impact Fortescue's future growth by reviewing our analysis of Fortescue's Future Performance.

Threats: Key Risks and Challenges That Could Impact Fortescue's Success

Fortescue faces several external threats that could impact its growth and market share. The global green hydrogen market is still developing, and the cost of power in many countries remains high, as noted by Richard Hutchinson. This could affect the company's green initiatives and profitability. Additionally, the ongoing decarbonization process and fluctuating power costs present long-term challenges. Competitive pressures are also evident, with peers investing significantly in blending opportunities, which Fortescue has decided against, as mentioned by Dino Otranto. The market transformation and reliance on the robustness of the Chinese market add further uncertainty to Fortescue's future performance.

Conclusion

Fortescue's strong financial health, marked by significant shipments and cost efficiency, has resulted in impressive profitability and substantial shareholder returns. However, challenges such as infrastructure issues, rising expenses, and a relatively inexperienced management team could impact strategic decision-making. The company's focus on green metals and exploration in South America presents promising growth opportunities, though external threats like high power costs and market competition remain. Trading at a Price-To-Earnings Ratio of 6.4x, below the peer and industry averages, Fortescue appears attractively priced, suggesting potential for future appreciation if it successfully navigates these challenges and capitalizes on growth initiatives.

Already own FMG? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About ASX:FMG

Fortescue

Engages in the exploration, development, production, processing, and sale of iron ore in Australia, China, and internationally.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives