- Australia

- /

- Metals and Mining

- /

- ASX:CHN

Chalice Mining (ASX:CHN) Valuation Check After Governance Fix and Gonneville Pre‑Feasibility Update

Reviewed by Simply Wall St

Chalice Mining (ASX:CHN) has just resolved a governance issue by appointing independent director Garret Dixon as chair of its Audit Committee, while investors are also watching for the upcoming discussion on the Gonneville Project pre feasibility study.

See our latest analysis for Chalice Mining.

The governance clean up and focus on the Gonneville pre feasibility study seem to be feeding into a strong rebound narrative. The latest A$2.04 share price sits alongside an 80.53 percent year to date share price return, but a still deeply negative three year total shareholder return of 66.83 percent, suggesting improving momentum from a heavily sold off base.

If you are looking beyond Chalice for other ideas in resources and infrastructure linked themes, this could be a good moment to explore fast growing stocks with high insider ownership.

With governance now tidied up and Gonneville moving toward pre feasibility, has Chalice’s sharp share price rebound left meaningful upside on the table, or is the market already pricing in the next leg of growth?

Price-to-Book of 6.1x: Is it justified?

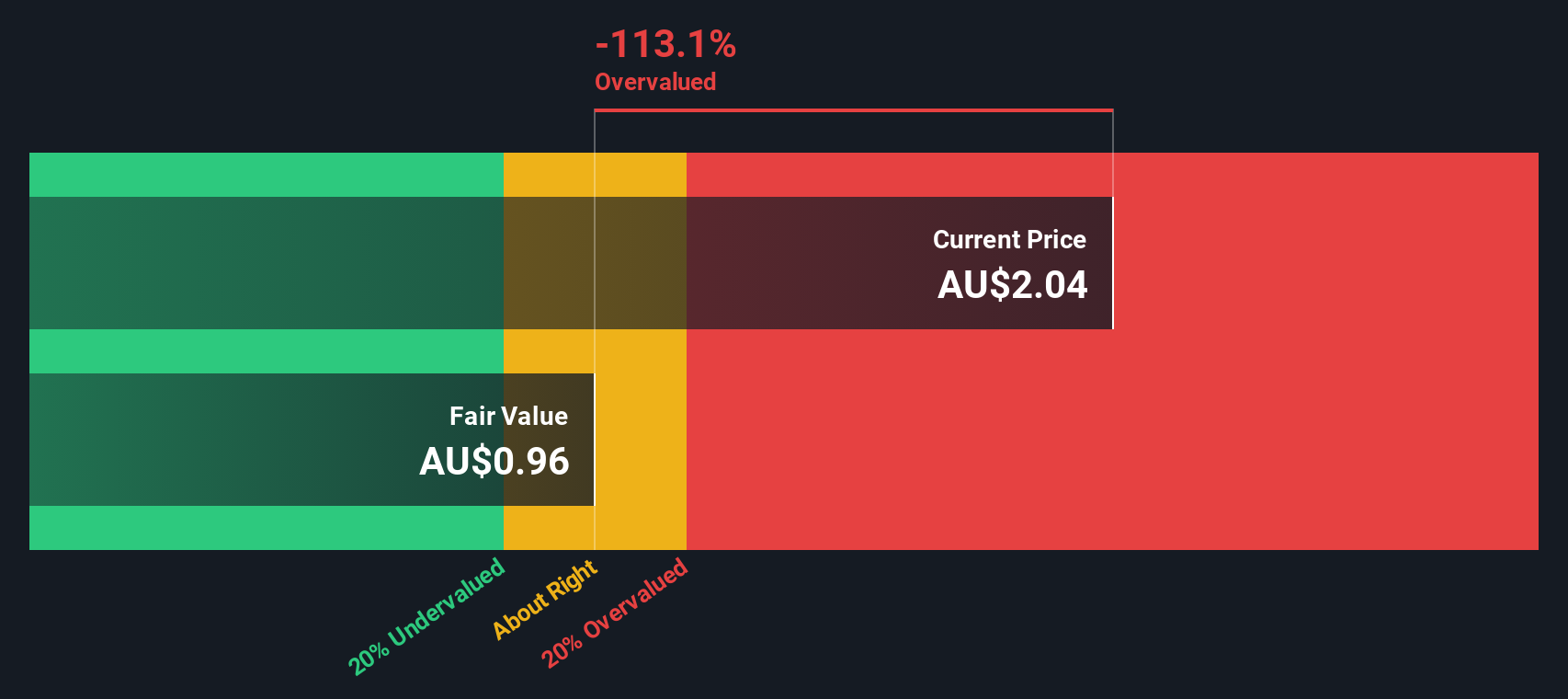

On a last close of A$2.04, Chalice Mining trades on a price-to-book ratio of 6.1 times, pointing to a rich valuation relative to assets.

The price-to-book multiple compares the company’s market value to its net assets, a common yardstick for capital intensive, asset heavy sectors like metals and mining.

For Chalice, a 6.1 times price-to-book suggests investors are paying a significant premium over the book value of its exploration assets. This effectively front loads expectations for future project success and cash flow that have yet to materialise, particularly while the company remains loss making.

That premium stands out against the broader Australian metals and mining industry average of 2.3 times price-to-book. This implies the market is assigning Chalice a much more optimistic appraisal than typical sector peers at this stage.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 6.1x (OVERVALUED)

However, risks remain, including execution uncertainty around the Gonneville pre feasibility study and the possibility that metal price weakness undermines today’s optimistic valuation.

Find out about the key risks to this Chalice Mining narrative.

Another View on Value

Our DCF model paints a starker picture than the 6.1 times price to book ratio. With Chalice trading at A$2.04 against an estimated fair value of around A$0.96, the shares screen as materially overvalued. Is sentiment running too far ahead of fundamentals, or is the model missing future upside from Gonneville?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Chalice Mining for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Chalice Mining Narrative

If our perspective does not quite match your own, or you would rather dig into the numbers yourself, you can build a custom view in just a few minutes, Do it your way.

A great starting point for your Chalice Mining research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before markets move on without you, take a moment to scan fresh opportunities our screeners surface so your watchlist keeps working as hard as you do.

- Consider fast moving small caps by reviewing these 3625 penny stocks with strong financials that pair higher risk with the potential for outsized upside.

- Position your portfolio for the next tech development cycle by zeroing in on these 24 AI penny stocks shaping automation, data intelligence, and productivity trends.

- Explore ways to strengthen your income stream by focusing on these 13 dividend stocks with yields > 3% that combine attractive yields with solid underlying businesses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CHN

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion