- Australia

- /

- Metals and Mining

- /

- ASX:CAI

Further weakness as Calidus Resources (ASX:CAI) drops 14% this week, taking three-year losses to 67%

If you are building a properly diversified stock portfolio, the chances are some of your picks will perform badly. But the long term shareholders of Calidus Resources Limited (ASX:CAI) have had an unfortunate run in the last three years. So they might be feeling emotional about the 67% share price collapse, in that time. The more recent news is of little comfort, with the share price down 33% in a year. Even worse, it's down 32% in about a month, which isn't fun at all.

With the stock having lost 14% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

View our latest analysis for Calidus Resources

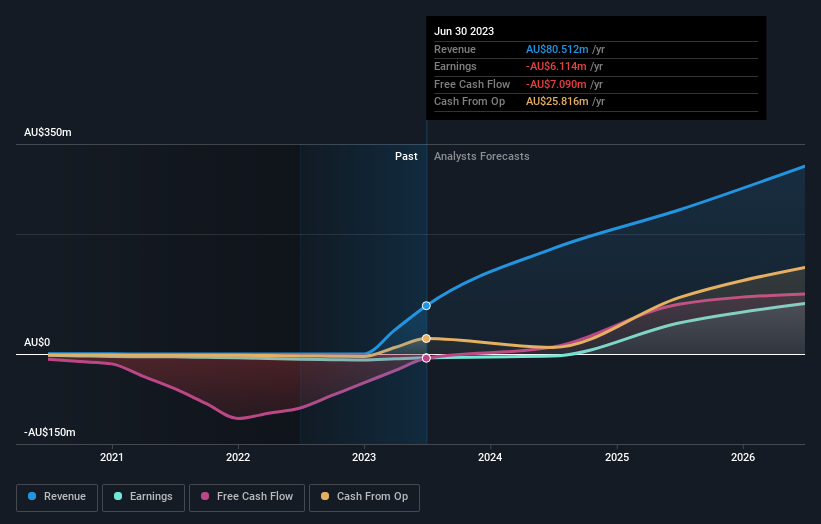

Calidus Resources isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last three years, Calidus Resources saw its revenue grow by 159% per year, compound. That's well above most other pre-profit companies. In contrast, the share price is down 19% compound, over three years - disappointing by most standards. This could mean hype has come out of the stock because the losses are concerning investors. When we see revenue growth, paired with a falling share price, we can't help wonder if there is an opportunity for those who are willing to dig deeper.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

A Different Perspective

Investors in Calidus Resources had a tough year, with a total loss of 33%, against a market gain of about 7.5%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 8% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Calidus Resources better, we need to consider many other factors. Case in point: We've spotted 2 warning signs for Calidus Resources you should be aware of.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CAI

Calidus Resources

Engages in the exploration and exploitation of gold minerals in Australia.

Slight and slightly overvalued.

Similar Companies

Market Insights

Community Narratives