- Australia

- /

- Metals and Mining

- /

- ASX:BSL

There Is A Reason BlueScope Steel Limited's (ASX:BSL) Price Is Undemanding

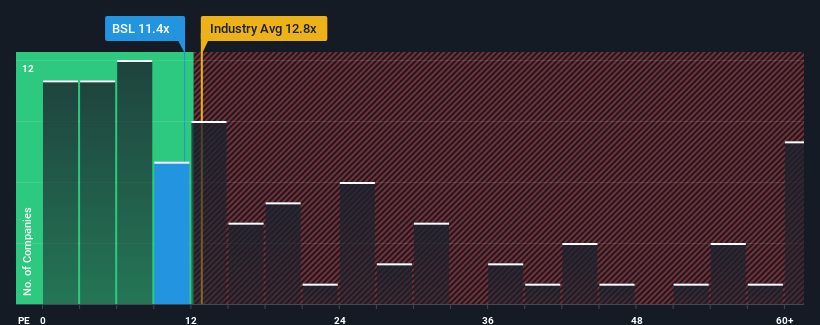

When close to half the companies in Australia have price-to-earnings ratios (or "P/E's") above 20x, you may consider BlueScope Steel Limited (ASX:BSL) as an attractive investment with its 11.4x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

While the market has experienced earnings growth lately, BlueScope Steel's earnings have gone into reverse gear, which is not great. The P/E is probably low because investors think this poor earnings performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for BlueScope Steel

How Is BlueScope Steel's Growth Trending?

In order to justify its P/E ratio, BlueScope Steel would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a frustrating 17% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 22% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 3.4% per year during the coming three years according to the twelve analysts following the company. With the market predicted to deliver 18% growth per annum, the company is positioned for a weaker earnings result.

In light of this, it's understandable that BlueScope Steel's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that BlueScope Steel maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with BlueScope Steel, and understanding should be part of your investment process.

If you're unsure about the strength of BlueScope Steel's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if BlueScope Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:BSL

BlueScope Steel

Engages in the production and marketing of metal coated and painted steel building products in Australia, New Zealand, Asia, North America, and internationally.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives