Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:AZS

Here's Why We Think Azure Minerals Limited's (ASX:AZS) CEO Compensation Looks Fair for the time being

Performance at Azure Minerals Limited (ASX:AZS) has been reasonably good and CEO Tony Rovira has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 15 November 2022. We present our case of why we think CEO compensation looks fair.

Check out the opportunities and risks within the AU Metals and Mining industry.

Comparing Azure Minerals Limited's CEO Compensation With The Industry

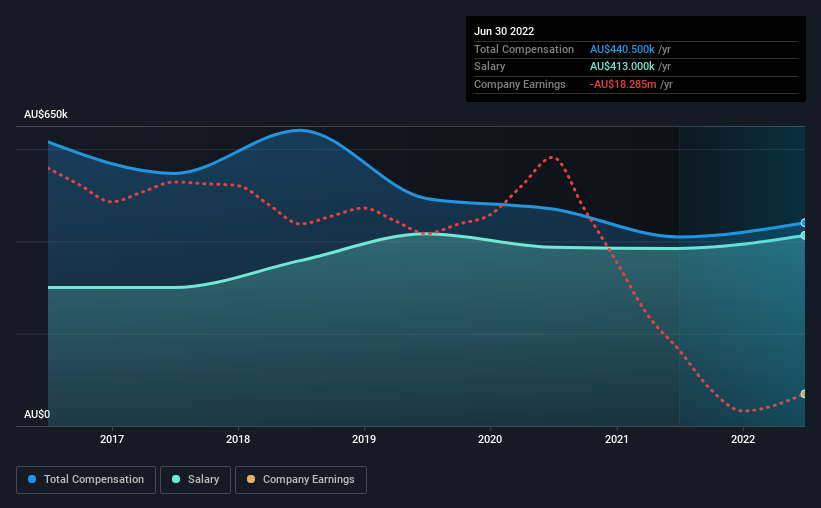

At the time of writing, our data shows that Azure Minerals Limited has a market capitalization of AU$103m, and reported total annual CEO compensation of AU$441k for the year to June 2022. That's a modest increase of 7.5% on the prior year. In particular, the salary of AU$413.0k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under AU$309m, the reported median total CEO compensation was AU$366k. This suggests that Azure Minerals remunerates its CEO largely in line with the industry average. Moreover, Tony Rovira also holds AU$707k worth of Azure Minerals stock directly under their own name.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$413k | AU$385k | 94% |

| Other | AU$28k | AU$25k | 6% |

| Total Compensation | AU$441k | AU$410k | 100% |

Talking in terms of the industry, salary represented approximately 60% of total compensation out of all the companies we analyzed, while other remuneration made up 40% of the pie. According to our research, Azure Minerals has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Azure Minerals Limited's Growth

Azure Minerals Limited's earnings per share (EPS) grew 8.4% per year over the last three years. In the last year, its revenue is down 96%.

We generally like to see a little revenue growth, but the modest EPS growth gives us some relief. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Azure Minerals Limited Been A Good Investment?

Boasting a total shareholder return of 137% over three years, Azure Minerals Limited has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. In our study, we found 6 warning signs for Azure Minerals you should be aware of, and 4 of them are potentially serious.

Important note: Azure Minerals is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:AZS

Azure Minerals

Azure Minerals Limited engages in the exploration of precious and base minerals in Australia.

Flawless balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|11.6% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor