Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:ARR

American Rare Earths (ASX:ARR) shareholder returns have been fantastic, earning 518% in 1 year

For many, the main point of investing in the stock market is to achieve spectacular returns. When you find (and hold) a big winner, you can markedly improve your finances. For example, the American Rare Earths Limited (ASX:ARR) share price rocketed moonwards 518% in just one year. It's also good to see the share price up 166% over the last quarter. The company reported its financial results recently; you can catch up on the latest numbers by reading our company report. And shareholders have also done well over the long term, with an increase of 357% in the last three years. Anyone who held for that rewarding ride would probably be keen to talk about it.

Since it's been a strong week for American Rare Earths shareholders, let's have a look at trend of the longer term fundamentals.

See our latest analysis for American Rare Earths

With just AU$2,291,137 worth of revenue in twelve months, we don't think the market considers American Rare Earths to have proven its business plan. So it seems that the investors focused more on what could be, than paying attention to the current revenues (or lack thereof). For example, investors may be hoping that American Rare Earths finds some valuable resources, before it runs out of money.

Companies that lack both meaningful revenue and profits are usually considered high risk. There is usually a significant chance that they will need more money for business development, putting them at the mercy of capital markets to raise equity. So the share price itself impacts the value of the shares (as it determines the cost of capital). While some such companies go on to make revenue, profits, and generate value, others get hyped up by hopeful naifs before eventually going bankrupt. American Rare Earths has already given some investors a taste of the sweet gains that high risk investing can generate, if your timing is right.

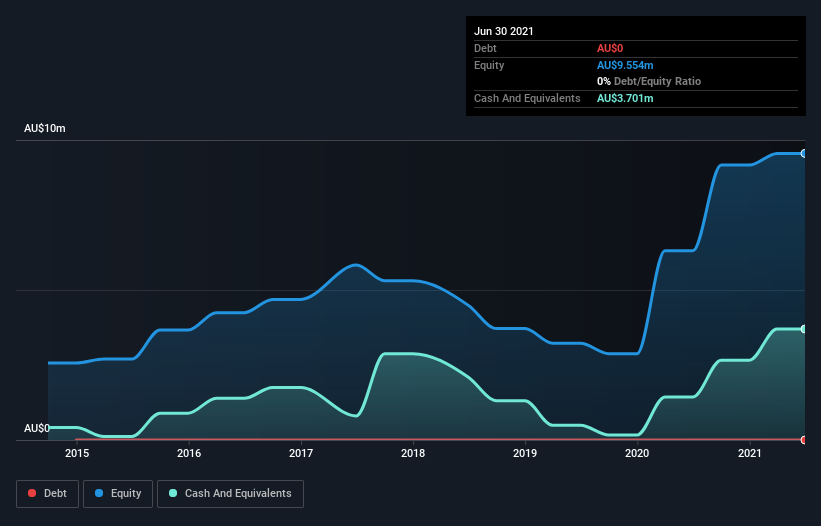

When it last reported its balance sheet in June 2021, American Rare Earths had cash in excess of all liabilities of AU$3.3m. That's not too bad but management may have to think about raising capital or taking on debt, unless the company is close to breaking even. Given the share price has increased by a solid 42% in the last year , it's fair to say investors remain excited about the future, despite the potential need for cash. The image below shows how American Rare Earths' balance sheet has changed over time; if you want to see the precise values, simply click on the image.

Of course, the truth is that it is hard to value companies without much revenue or profit. However you can take a look at whether insiders have been buying up shares. It's usually a positive if they have, as it may indicate they see value in the stock. You can click here to see if there are insiders buying.

A Different Perspective

We're pleased to report that American Rare Earths shareholders have received a total shareholder return of 518% over one year. That's better than the annualised return of 26% over half a decade, implying that the company is doing better recently. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand American Rare Earths better, we need to consider many other factors. Even so, be aware that American Rare Earths is showing 5 warning signs in our investment analysis , and 1 of those can't be ignored...

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:ARR

American Rare Earths

Engages in the exploration and development of mineral resources in Australia and the United States.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor