Advertisement

ASX Stocks That May Be Priced Below Estimated Value In December 2024

Simply Wall St

Reviewed by Simply Wall St

As the ASX 200 inches up by 1% to reach 8,200, buoyed by a potential Santa Rally and strong performances in Financials and Discretionary sectors, investors are keenly observing market movements for opportunities. In such an environment where every sector has shown positive momentum, identifying stocks that may be priced below their estimated value can offer strategic entry points for those looking to capitalize on potential growth.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Data#3 (ASX:DTL) | A$6.52 | A$12.30 | 47% |

| Regal Partners (ASX:RPL) | A$3.52 | A$6.21 | 43.3% |

| Telix Pharmaceuticals (ASX:TLX) | A$24.62 | A$43.45 | 43.3% |

| Ansell (ASX:ANN) | A$33.23 | A$59.90 | 44.5% |

| Ingenia Communities Group (ASX:INA) | A$4.66 | A$9.19 | 49.3% |

| ReadyTech Holdings (ASX:RDY) | A$3.18 | A$6.26 | 49.2% |

| Charter Hall Group (ASX:CHC) | A$14.76 | A$28.66 | 48.5% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Genesis Minerals (ASX:GMD) | A$2.54 | A$4.90 | 48.2% |

| FINEOS Corporation Holdings (ASX:FCL) | A$1.955 | A$3.84 | 49% |

Let's take a closer look at a couple of our picks from the screened companies.

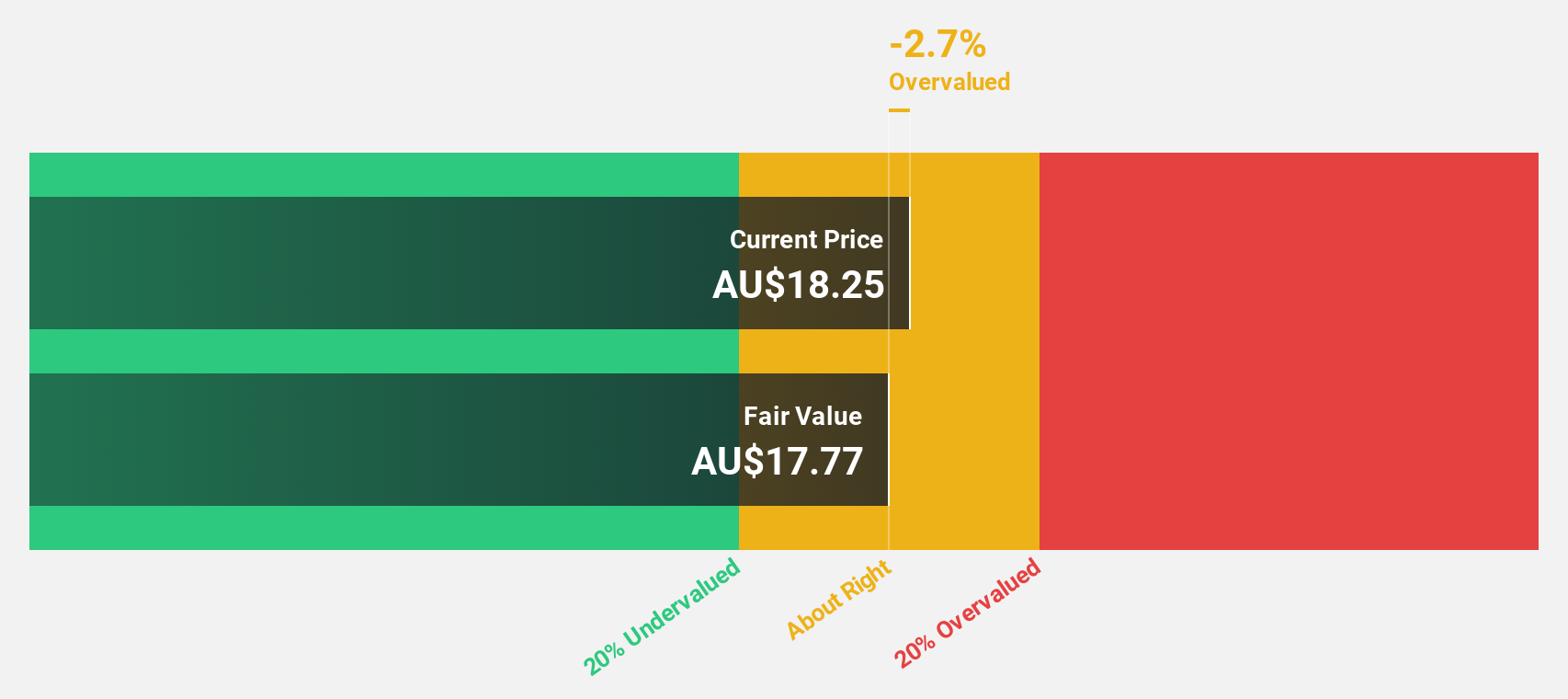

Codan (ASX:CDA)

Overview: Codan Limited develops technology solutions for a diverse range of clients including United Nations organizations, security and military groups, government departments, individuals, and small-scale miners, with a market cap of A$2.94 billion.

Operations: Codan's revenue is primarily derived from its Communications segment, which generated A$326.91 million, and its Metal Detection segment, contributing A$219.85 million.

Estimated Discount To Fair Value: 39.3%

Codan, recently added to the S&P/ASX 200 Index, is trading at A$16.3, which is 39.3% below its estimated fair value of A$26.86, highlighting its potential undervaluation based on cash flows. The company's earnings are forecast to grow by 17.4% annually, outpacing the broader Australian market's growth rate of 12.5%. Additionally, Codan's revenue is expected to increase by 10.6% per year, surpassing the market average of 5.8%.

- The analysis detailed in our Codan growth report hints at robust future financial performance.

- Click to explore a detailed breakdown of our findings in Codan's balance sheet health report.

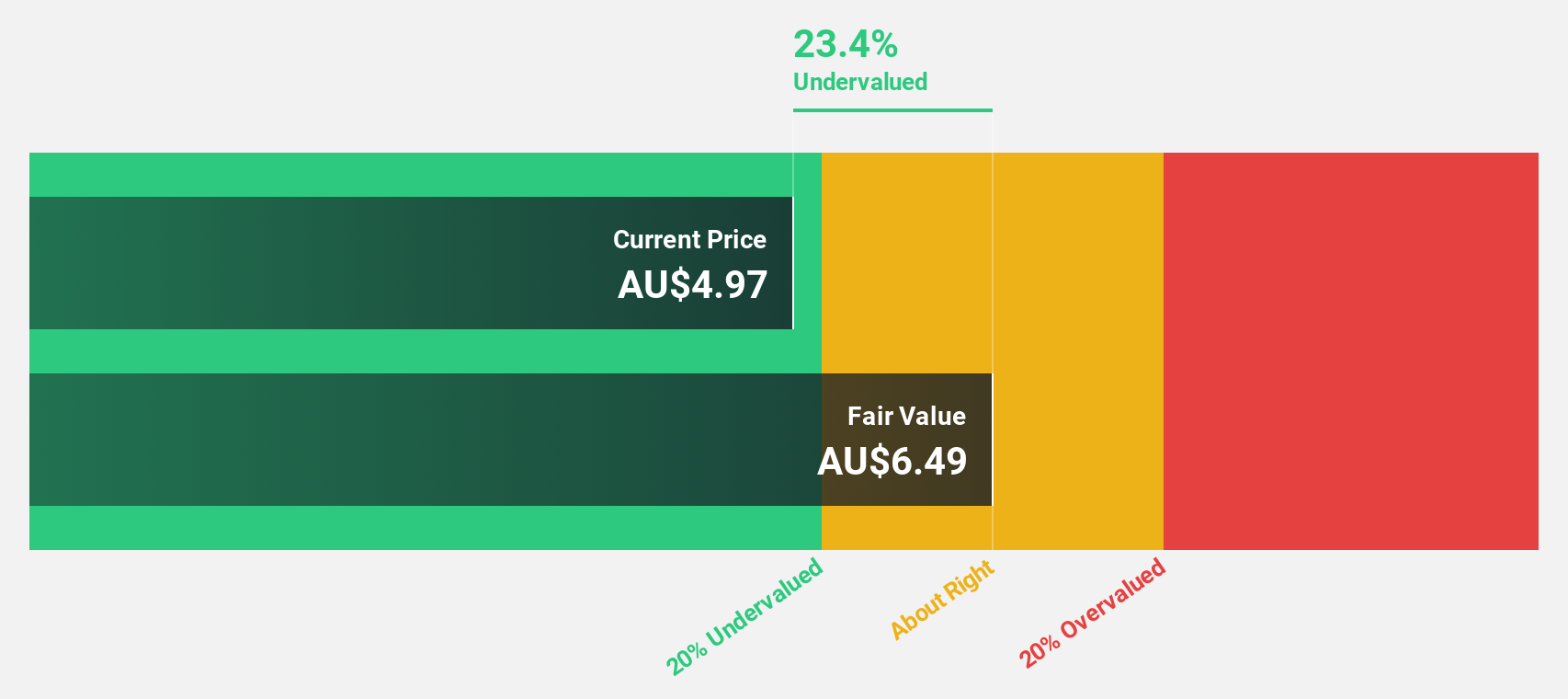

Ingenia Communities Group (ASX:INA)

Overview: Ingenia Communities Group (ASX:INA) is a prominent operator, owner, and developer of residential communities and holiday accommodations with a market cap of A$1.88 billion.

Operations: The company's revenue is primarily derived from its segments in Tourism - Ingenia Holidays (A$134.84 million), Residential - Lifestyle Development (A$205.81 million), Residential - Lifestyle Rental (A$86.50 million), and Residential - Ingenia Gardens (A$23.67 million), along with contributions from Fuel, Food & Beverage (A$19.26 million).

Estimated Discount To Fair Value: 49.3%

Ingenia Communities Group, trading at A$4.66, is significantly undervalued with an estimated fair value of A$9.19. Despite a low forecasted return on equity of 7.9%, its earnings are projected to grow substantially by 25.6% annually, surpassing the Australian market's growth rate of 12.5%. Recent M&A speculation involves Ingenia potentially acquiring Lifestyle Communities to strengthen its position, possibly funded by selling its A$1 billion holiday parks business or using shares for the transaction.

- Upon reviewing our latest growth report, Ingenia Communities Group's projected financial performance appears quite optimistic.

- Take a closer look at Ingenia Communities Group's balance sheet health here in our report.

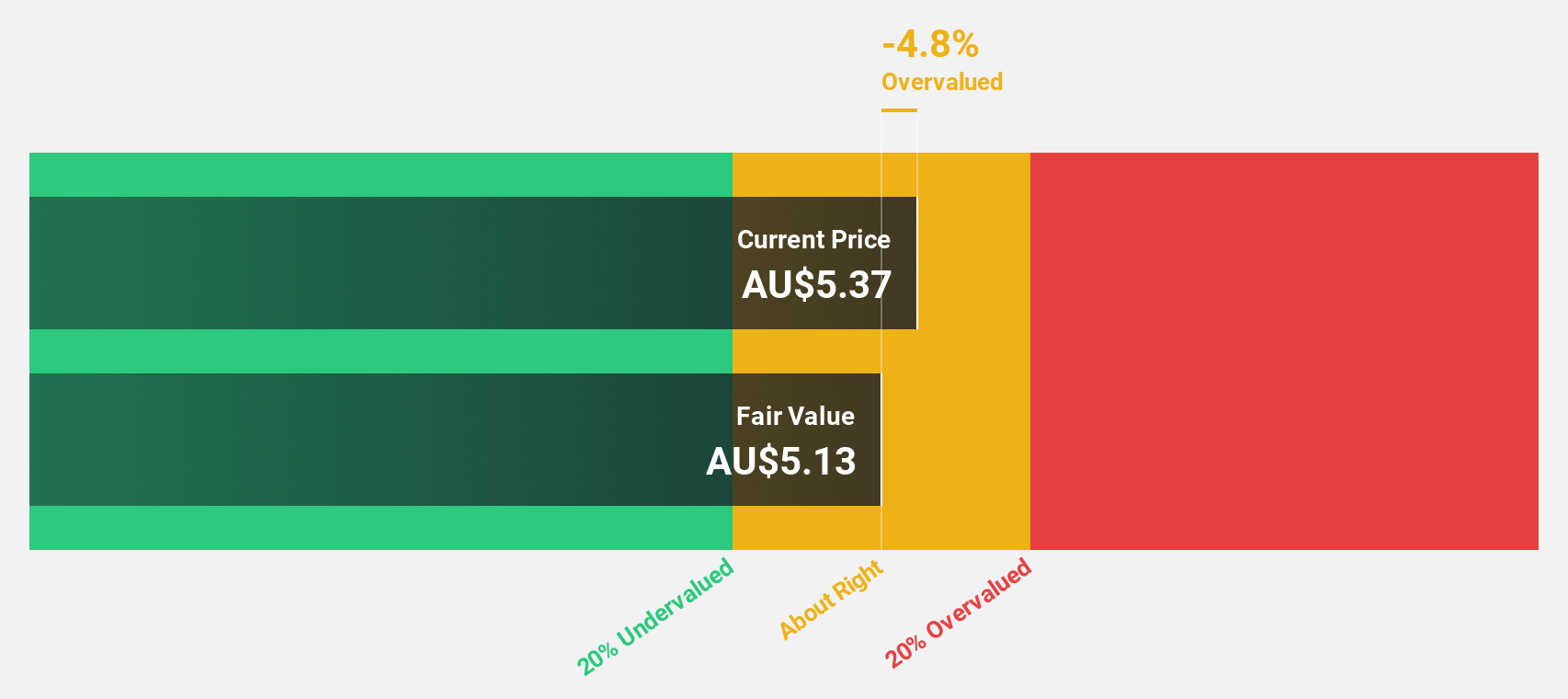

Medibank Private (ASX:MPL)

Overview: Medibank Private Limited offers private health insurance and health services in Australia, with a market cap of A$10.36 billion.

Operations: The company's revenue segments consist of Health Insurance, generating A$7.90 billion, and Medibank Health, contributing A$360.10 million.

Estimated Discount To Fair Value: 40.1%

Medibank Private, priced at A$3.81, is trading significantly below its estimated fair value of A$6.36, indicating potential undervaluation based on cash flows. Earnings are forecasted to grow robustly at 27.2% annually, outpacing the Australian market's growth rate of 12.5%, although revenue growth lags behind the market average. Despite a high future return on equity projection of 23.8%, its dividend yield of 4.36% isn't well covered by earnings, posing sustainability concerns.

- Our comprehensive growth report raises the possibility that Medibank Private is poised for substantial financial growth.

- Dive into the specifics of Medibank Private here with our thorough financial health report.

Summing It All Up

- Reveal the 37 hidden gems among our Undervalued ASX Stocks Based On Cash Flows screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:MPL

Medibank Private

Provides private health insurance and health services in Australia.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor