Advertisement

- Australia

- /

- Medical Equipment

- /

- ASX:PNV

PolyNovo Limited's (ASX:PNV) 25% Jump Shows Its Popularity With Investors

Those holding PolyNovo Limited (ASX:PNV) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 35% over that time.

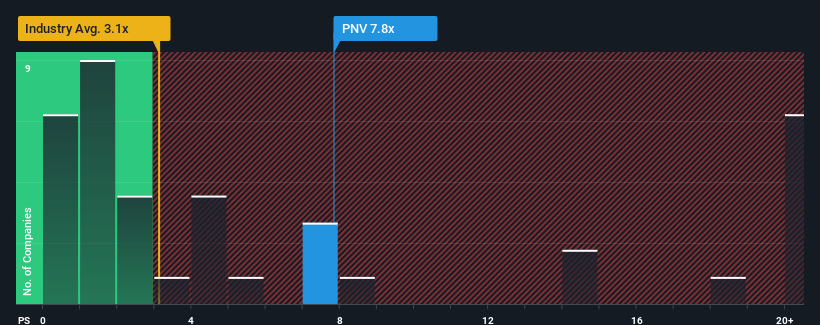

After such a large jump in price, you could be forgiven for thinking PolyNovo is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 7.8x, considering almost half the companies in Australia's Medical Equipment industry have P/S ratios below 3.1x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Our free stock report includes 1 warning sign investors should be aware of before investing in PolyNovo. Read for free now.Check out our latest analysis for PolyNovo

How Has PolyNovo Performed Recently?

PolyNovo certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think PolyNovo's future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For PolyNovo?

In order to justify its P/S ratio, PolyNovo would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered an exceptional 38% gain to the company's top line. Pleasingly, revenue has also lifted 233% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 19% each year during the coming three years according to the nine analysts following the company. That's shaping up to be materially higher than the 11% per annum growth forecast for the broader industry.

In light of this, it's understandable that PolyNovo's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From PolyNovo's P/S?

PolyNovo's P/S has grown nicely over the last month thanks to a handy boost in the share price. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that PolyNovo maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Medical Equipment industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for PolyNovo that you should be aware of.

If you're unsure about the strength of PolyNovo's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PNV

PolyNovo

Designs, manufactures, and sells biodegradable medical devices in the United States, Australia, New Zealand, and internationally.

High growth potential with proven track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor