Advertisement

- Australia

- /

- Healthtech

- /

- ASX:ONE

Here's Why We're Watching Oneview Healthcare's (ASX:ONE) Cash Burn Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for Oneview Healthcare (ASX:ONE) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. We'll start by comparing its cash burn with its cash reserves in order to calculate its cash runway.

Check out our latest analysis for Oneview Healthcare

How Long Is Oneview Healthcare's Cash Runway?

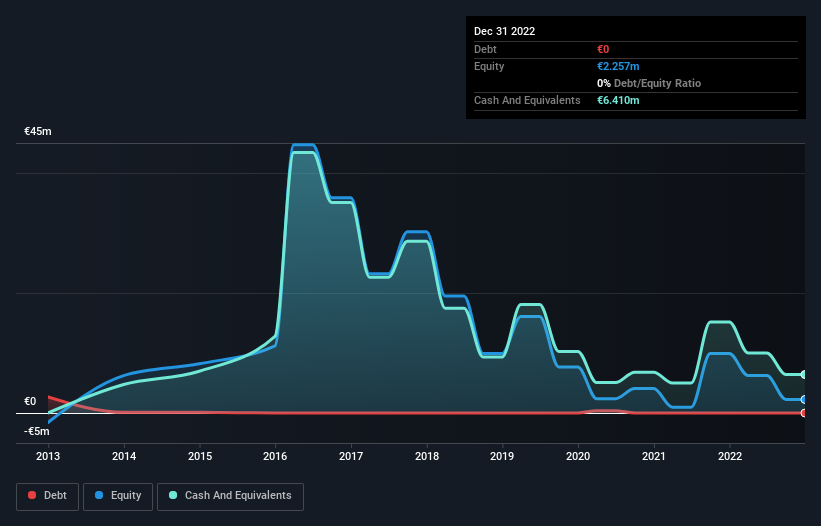

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. As at December 2022, Oneview Healthcare had cash of €6.4m and no debt. Looking at the last year, the company burnt through €9.0m. So it had a cash runway of approximately 9 months from December 2022. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Oneview Healthcare Growing?

Notably, Oneview Healthcare actually ramped up its cash burn very hard and fast in the last year, by 119%, signifying heavy investment in the business. While that's concerning on it's own, the fact that operating revenue was actually down 8.3% over the same period makes us positively tremulous. Considering both these metrics, we're a little concerned about how the company is developing. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how Oneview Healthcare is building its business over time.

Can Oneview Healthcare Raise More Cash Easily?

Since Oneview Healthcare can't yet boast improving growth metrics, the market will likely be considering how it can raise more cash if need be. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Oneview Healthcare has a market capitalisation of €83m and burnt through €9.0m last year, which is 11% of the company's market value. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

So, Should We Worry About Oneview Healthcare's Cash Burn?

On this analysis of Oneview Healthcare's cash burn, we think its cash burn relative to its market cap was reassuring, while its increasing cash burn has us a bit worried. Summing up, we think the Oneview Healthcare's cash burn is a risk, based on the factors we mentioned in this article. On another note, Oneview Healthcare has 4 warning signs (and 2 which are significant) we think you should know about.

Of course Oneview Healthcare may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ONE

Oneview Healthcare

Develops and sells software services for the healthcare sector in Ireland, the United States, Australia, Ireland, the Middle East, and Asia.

Excellent balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor