Advertisement

- Australia

- /

- Medical Equipment

- /

- ASX:CYC

Rainbows and Unicorns: The Cyclopharm Limited (ASX:CYC) Analyst Just Became A Lot More Optimistic

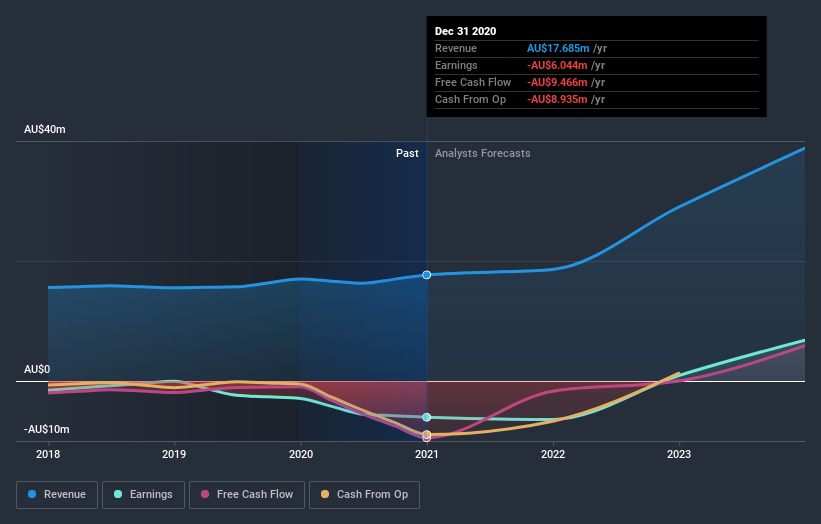

Shareholders in Cyclopharm Limited (ASX:CYC) may be thrilled to learn that the covering analyst has just delivered a major upgrade to their near-term forecasts. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analyst modelling a real improvement in business performance.

After this upgrade, Cyclopharm's single analyst is now forecasting revenues of AU$19m in 2021. This would be a modest 5.2% improvement in sales compared to the last 12 months. Losses are expected to be contained, narrowing 11% from last year to AU$0.07. Yet prior to the latest estimates, the analyst had been forecasting revenues of AU$17m and losses of AU$0.083 per share in 2021. So there's been quite a change-up of views after the recent consensus updates, with the analyst making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

View our latest analysis for Cyclopharm

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Cyclopharm's past performance and to peers in the same industry. The period to the end of 2021 brings more of the same, according to the analyst, with revenue forecast to display 5.2% growth on an annualised basis. That is in line with its 4.9% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 15% per year. So it's pretty clear that Cyclopharm is expected to grow slower than similar companies in the same industry.

The Bottom Line

The most important thing here is that the analyst reduced their loss per share estimates for this year, reflecting increased optimism around Cyclopharm's prospects. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. More bullish expectations could be a signal for investors to take a closer look at Cyclopharm.

Better yet, Cyclopharm is expected to break-even soon - within the next few years - according to analyst forecasts, which would be a momentous event for shareholders. For more information, you can click through to our free platform to learn more about these forecasts.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you decide to trade Cyclopharm, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:CYC

Cyclopharm

Cyclopharm Limited manufacture and sells medical equipment and radiopharmaceuticals in the Asia Pacific, Europe, Canada, the United States, and internationally.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative