- Australia

- /

- Consumer Finance

- /

- ASX:ZIP

Zip Co (ASX:ZIP) Partners With GameStop As Stock Drops 16% Over The Week

Reviewed by Simply Wall St

Last week, GameStop Corp. announced a partnership with Zip Co (ASX:ZIP) to become GameStop's primary pay-in-installments service in the U.S. Despite this development, Zip Co's share price declined 16% over the week. This movement occurred amid broader market volatility, likely influenced by anticipation of President Trump's tariff announcements, which has affected investor sentiment across various sectors. While the Dow Jones and the Nasdaq showed recoveries later in the week, Zip Co's involvement in a new strategic partnership didn't shield it from market-wide pressures, reflecting broader economic uncertainties influencing stock valuations.

Buy, Hold or Sell Zip Co? View our complete analysis and fair value estimate and you decide.

Rare earth metals are the new gold rush. Find out which 21 stocks are leading the charge.

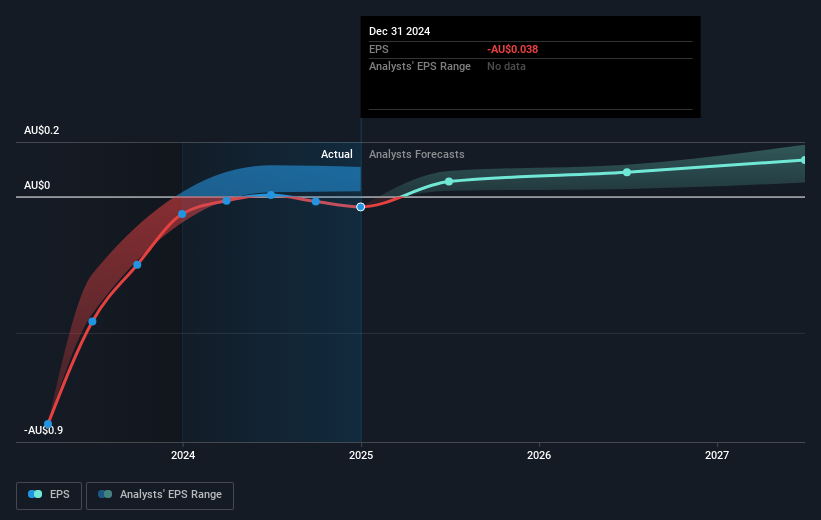

Over the past year, Zip Co's total return, including share price and dividends, was 22.69%. This performance surpassed the broader Australian market's decline of 1.7% and outpaced the Australian Consumer Finance industry that returned 1.5%. Key developments influencing this result included Zip's expansion and partnerships in the U.S., particularly following its integration with Stripe in mid-August 2024, which facilitated the use of Zip as a payment option for U.S. merchants. Additionally, Zip's earnings showed a significant turnaround with a net income of A$5.7 million for the full year, compared to a prior net loss of A$329.9 million, reflecting improved financial health and market optimism.

The company's share performance was also buoyed by capital raising initiatives, such as the successful follow-on equity offerings that secured a total of A$267.12 million in mid-2024. This capitalization supported Zip's expansion efforts, while its addition to the S&P/ASX 200 Index in July 2024 likely raised its profile among investors. However, the announcement of co-founder Larry Diamond stepping down from key roles in December 2024 introduced some uncertainty, though he remains an advisor, affirming continuity in leadership support.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Zip Co, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zip Co might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ZIP

Zip Co

Engages in the provision of digital retail finance and payments solutions to consumers, and small and medium sized merchants (SMEs) in Australia, New Zealand, Canada, and the United States.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives