Advertisement

Three Australian Undiscovered Gems with Strong Financial Metrics

Simply Wall St

Reviewed by Simply Wall St

Amidst a turbulent backdrop marked by trade tensions and fluctuating indices, the Australian market is poised for a potential rebound following one of its most challenging trading days in 2025. As investors navigate these uncertain waters, identifying stocks with robust financial metrics becomes crucial for those seeking stability and potential growth opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.78% | 4.30% | ★★★★★★ |

| Schaffer | 25.47% | 6.03% | -5.20% | ★★★★★★ |

| Fiducian Group | NA | 9.97% | 7.85% | ★★★★★★ |

| Hearts and Minds Investments | NA | 47.09% | 49.82% | ★★★★★★ |

| Djerriwarrh Investments | 1.14% | 8.17% | 7.54% | ★★★★★★ |

| Red Hill Minerals | NA | 95.16% | 40.06% | ★★★★★★ |

| MFF Capital Investments | 0.69% | 28.52% | 31.31% | ★★★★★☆ |

| Lycopodium | 6.89% | 16.56% | 32.73% | ★★★★★☆ |

| Carlton Investments | 0.02% | 4.45% | 3.97% | ★★★★★☆ |

| K&S | 20.24% | 1.58% | 25.54% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

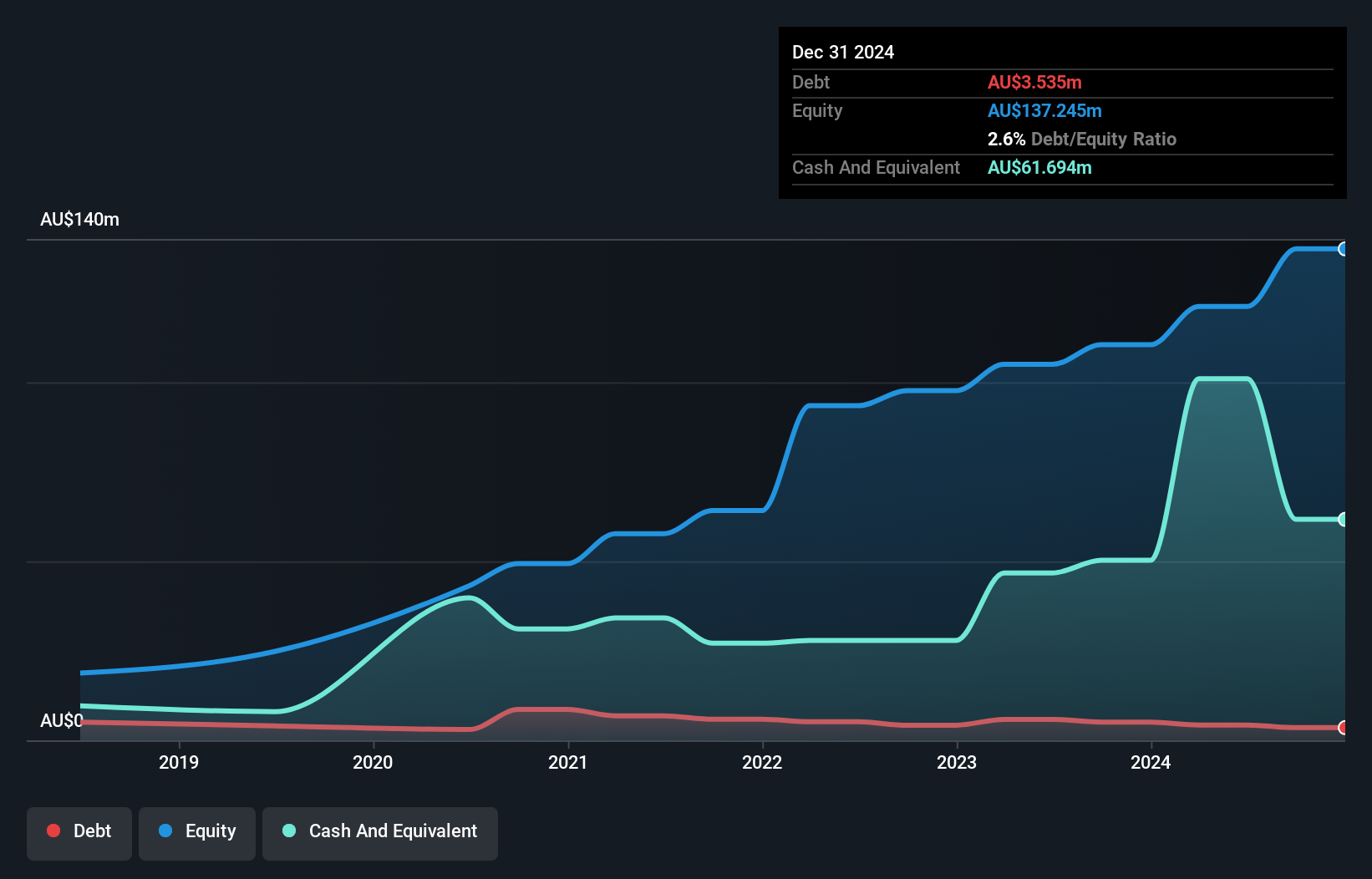

GenusPlus Group (ASX:GNP)

Simply Wall St Value Rating: ★★★★★★

Overview: GenusPlus Group Ltd specializes in the installation, construction, and maintenance of power and communication systems across Australia, with a market capitalization of approximately A$508.12 million.

Operations: GenusPlus Group Ltd generates revenue primarily from its Infrastructure segment, contributing A$372.42 million, followed by the Industrial and Communication segments with A$187.56 million and A$86.02 million, respectively. The company's net profit margin is a key financial metric to consider when evaluating its profitability trends over time.

GenusPlus Group, a dynamic player in Australia's construction sector, showcases impressive growth with earnings up 48.7% over the past year, outpacing the industry's 28.7% rise. The company's debt to equity ratio has notably improved from 10.3% to 2.6% over five years, highlighting effective financial management. Recent earnings reveal sales of A$332.87 million for H1 2025 compared to A$249.96 million previously, with net income rising to A$13.7 million from A$9.05 million last year and basic EPS improving to A$0.0769 from A$0.0509, indicating robust performance and potential for continued growth in this competitive market space.

- Dive into the specifics of GenusPlus Group here with our thorough health report.

Review our historical performance report to gain insights into GenusPlus Group's's past performance.

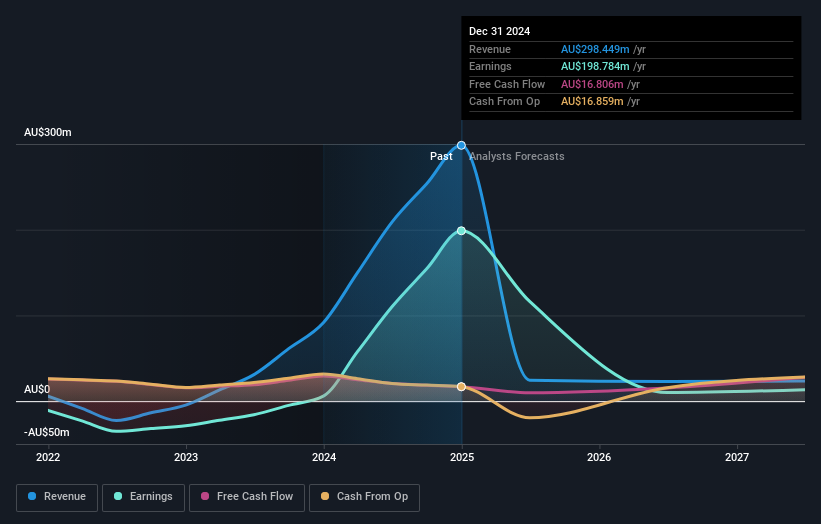

Pacific Current Group (ASX:PAC)

Simply Wall St Value Rating: ★★★★★☆

Overview: Pacific Current Group Limited operates a multi-boutique asset management business on a global scale, with a market capitalization of A$618.02 million.

Operations: Pacific Current Group generates revenue primarily through its multi-boutique asset management operations. The company's financial performance is characterized by a focus on optimizing profit margins, with particular attention to cost efficiencies.

Pacific Current Group, a small player in Australia's financial scene, recently showcased impressive earnings growth of 3270% over the past year, significantly outpacing the industry average of 23.6%. With a price-to-earnings ratio of 3.1x, it trades at an attractive value compared to the broader Australian market's 17.4x. The company's interest payments are well covered by EBIT at 39 times coverage, indicating strong financial health despite its debt-to-equity ratio rising to 8.9% over five years. While insider selling was noted recently, its high non-cash earnings and positive free cash flow suggest robust underlying performance.

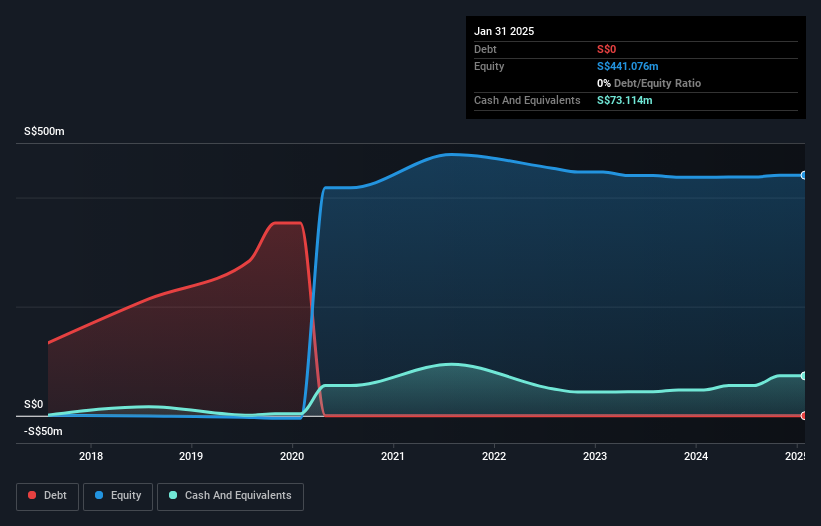

Tuas (ASX:TUA)

Simply Wall St Value Rating: ★★★★★★

Overview: Tuas Limited operates a mobile network in Singapore and has a market cap of A$2.55 billion.

Operations: Tuas Limited generates revenue primarily from its mobile operations, amounting to SGD 135.51 million.

Tuas has recently turned profitable, reporting a net income of SGD 3.02 million for the half year ended January 31, 2025, compared to a net loss of SGD 3.5 million the previous year. This telecom player is debt-free and boasts high-quality earnings, with revenue expected to grow at an impressive rate of nearly 17% annually. Free cash flow has improved significantly over time, reaching A$26.70 million as of April 2025 from negative figures in earlier years. With no interest payments to worry about and strong sales growth from SGD 54.72 million to SGD 73.16 million year-on-year, Tuas seems well-positioned for future expansion in its industry segment.

- Click to explore a detailed breakdown of our findings in Tuas' health report.

Gain insights into Tuas' past trends and performance with our Past report.

Turning Ideas Into Actions

- Discover the full array of 51 ASX Undiscovered Gems With Strong Fundamentals right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tuas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TUA

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor