Exploring Bell Financial Group And Two More ASX Stocks Estimated To Be Trading Below Their Value

Reviewed by Simply Wall St

Over the past year, the Australian stock market has shown robust growth, appreciating by 9.9%, while remaining stable in the last week. In this context of promising earnings forecasts with an expected annual growth of 14%, stocks like Bell Financial Group that are trading below their perceived value present intriguing opportunities for investors seeking potential gains.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| LaserBond (ASX:LBL) | A$0.715 | A$1.21 | 40.9% |

| COSOL (ASX:COS) | A$1.25 | A$2.43 | 48.7% |

| GTN (ASX:GTN) | A$0.43 | A$0.70 | 38.8% |

| Charter Hall Group (ASX:CHC) | A$12.40 | A$22.35 | 44.5% |

| ReadyTech Holdings (ASX:RDY) | A$3.21 | A$5.97 | 46.2% |

| hipages Group Holdings (ASX:HPG) | A$1.075 | A$1.95 | 44.7% |

| Regal Partners (ASX:RPL) | A$3.24 | A$6.19 | 47.7% |

| IPH (ASX:IPH) | A$6.32 | A$11.36 | 44.4% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Treasury Wine Estates (ASX:TWE) | A$12.57 | A$21.87 | 42.5% |

Underneath we present a selection of stocks filtered out by our screen

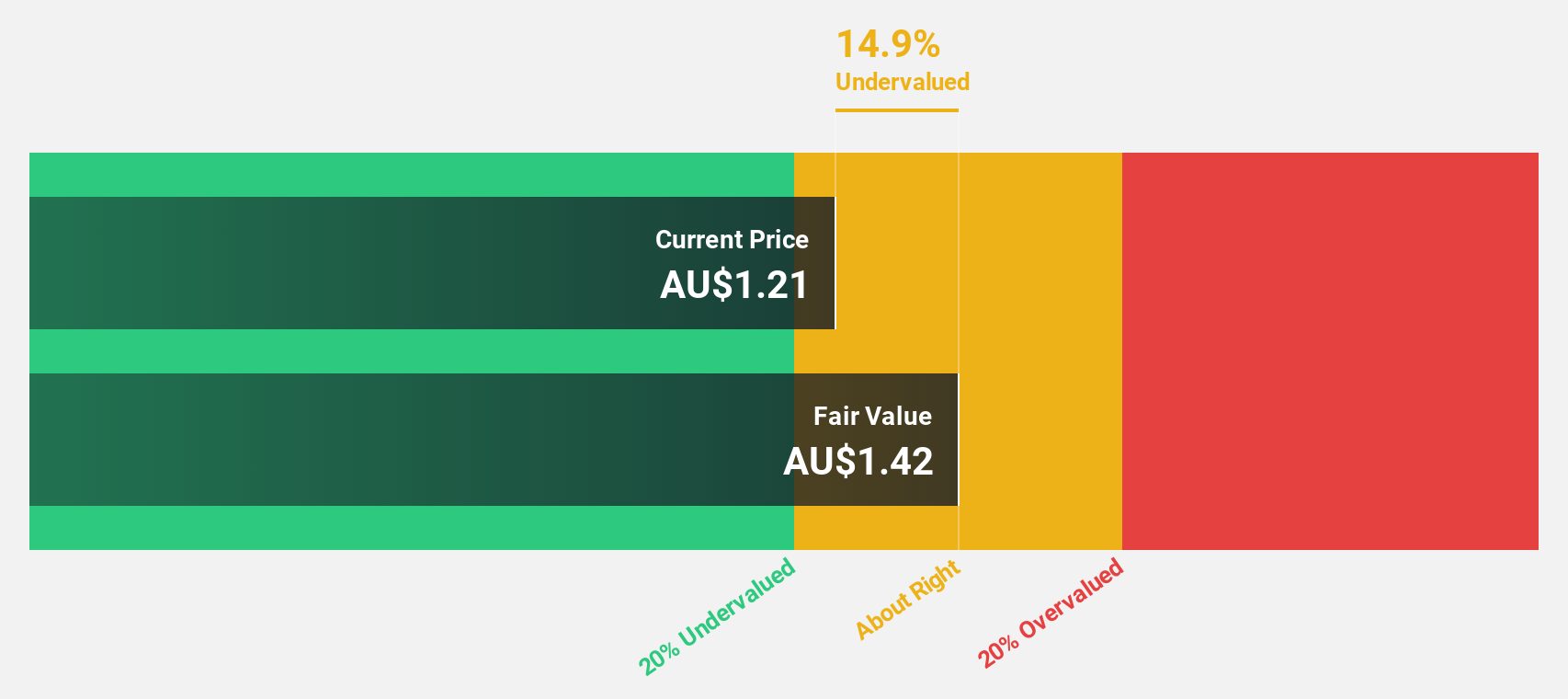

Bell Financial Group (ASX:BFG)

Overview: Bell Financial Group Limited (ASX:BFG) operates in the financial sector, offering services such as broking, online broking, corporate finance, and financial advisory to a diverse client base, with a market capitalization of approximately A$0.44 billion.

Operations: Bell Financial Group generates revenue through four primary channels: retail broking (A$103.58 million), institutional broking (A$50.36 million), financial products and services (A$48.10 million), and technology solutions for trading platforms (A$26.20 million).

Estimated Discount To Fair Value: 23.6%

Bell Financial Group, priced at A$1.36, is trading significantly below its estimated fair value of A$1.78, marking a 23.6% undervaluation based on discounted cash flow analysis. Despite a low forecasted return on equity of 16.3% in three years, the company's earnings are expected to grow by 26.95% annually, outpacing the Australian market's average growth rate of 13.7%. However, its dividend sustainability is questionable as it is not well covered by earnings or cash flows.

- Upon reviewing our latest growth report, Bell Financial Group's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Bell Financial Group.

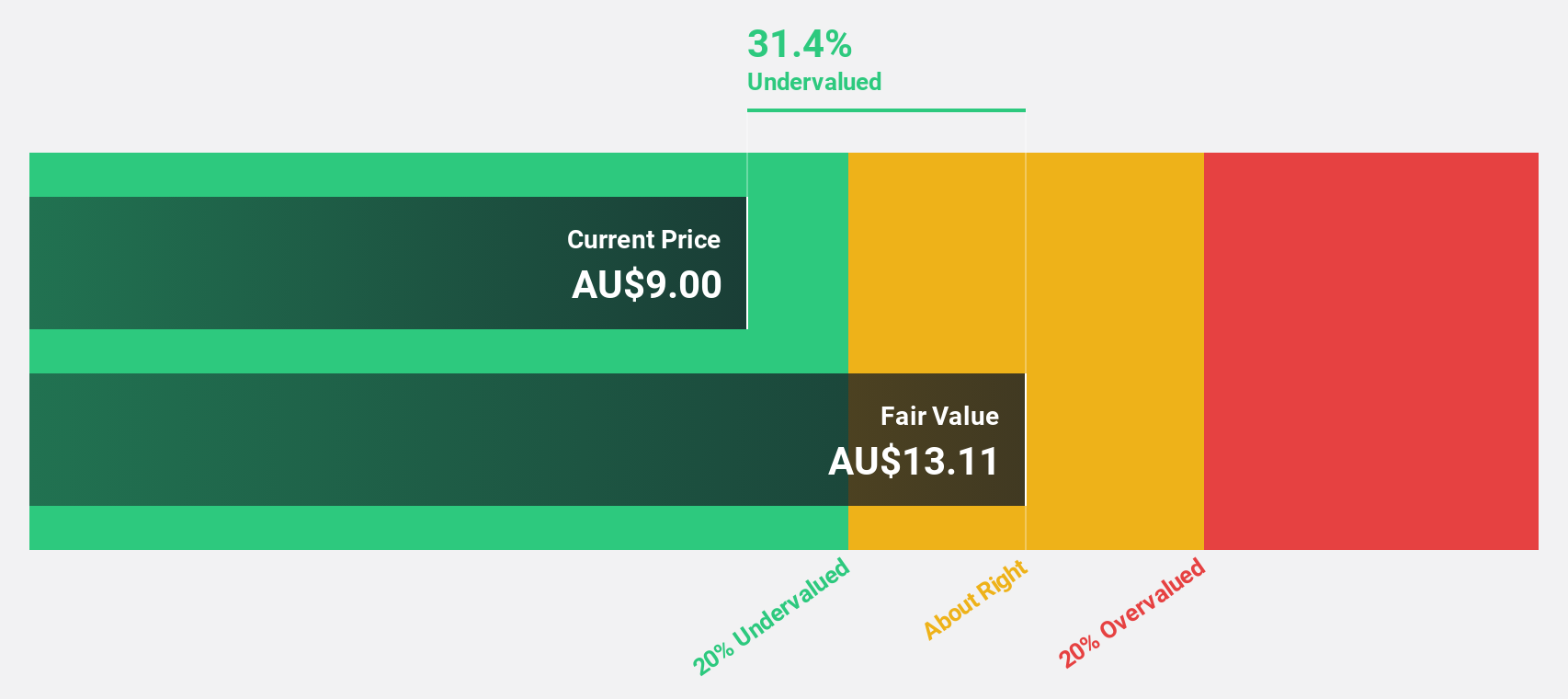

Lynas Rare Earths (ASX:LYC)

Overview: Lynas Rare Earths Limited operates in the exploration, development, mining, extraction, and processing of rare earth minerals primarily in Australia and Malaysia, with a market capitalization of approximately A$5.66 billion.

Operations: The company generates its revenue primarily from rare earth operations, which amounted to A$604.08 million.

Estimated Discount To Fair Value: 19.8%

Lynas Rare Earths, currently valued at A$6.06, appears undervalued with a potential fair value of A$7.55, reflecting a 19.8% discrepancy based on discounted cash flow analysis. Despite lower profit margins this year compared to last, the company is poised for substantial growth with earnings expected to increase by 33.22% annually and revenue projected to rise by 28.2% per year—both rates surpassing broader Australian market trends significantly.

- The analysis detailed in our Lynas Rare Earths growth report hints at robust future financial performance.

- Get an in-depth perspective on Lynas Rare Earths' balance sheet by reading our health report here.

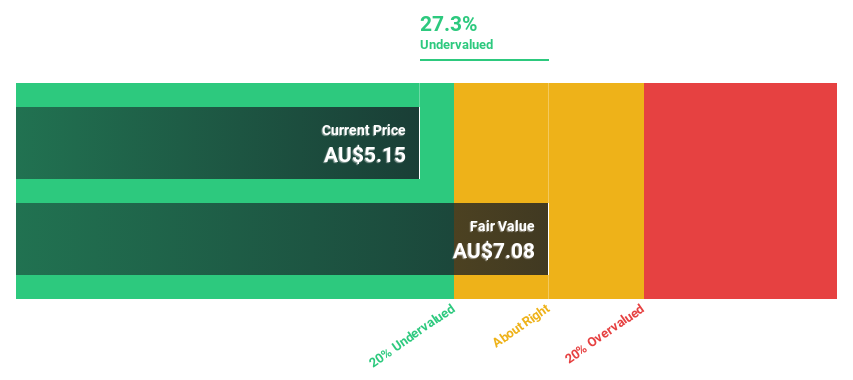

Stockland (ASX:SGP)

Overview: Stockland is a prominent developer specializing in creating connected communities, with a market capitalization of approximately A$10.80 billion.

Operations: The company generates revenue primarily through its Communities and Commercial Property segments, with figures amounting to A$1.77 billion and A$0.81 billion respectively.

Estimated Discount To Fair Value: 35.6%

Stockland, priced at A$4.53, trades below its estimated fair value of A$7.04, suggesting a significant undervaluation based on discounted cash flow analysis. Expected to outperform with a 22% annual earnings growth over the next three years—higher than the Australian market average of 13.7%. However, its profit margins have declined to 9.1% from last year's 31%, and dividends are poorly supported by cash flows, indicating potential financial stress despite forecasted revenue growth outpacing the market at 7% annually.

- Our earnings growth report unveils the potential for significant increases in Stockland's future results.

- Unlock comprehensive insights into our analysis of Stockland stock in this financial health report.

Next Steps

- Gain an insight into the universe of 47 Undervalued ASX Stocks Based On Cash Flows by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Stockland, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:SGP

Stockland

We are a leading creator and curator of connected communities with people at the heart of the places we create.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Community Narratives