Advertisement

3 Undervalued Small Caps In Australia With Recent Insider Buying

Simply Wall St

Reviewed by Simply Wall St

The Australian market has shown mixed performance recently, with the ASX200 closing up 0.3% at 8,099.9 points, driven by gains in the Materials and Real Estate sectors while Financials lagged behind. In this environment of fluctuating sector performance and economic indicators, identifying undervalued small-cap stocks with recent insider buying can offer unique investment opportunities. For investors looking to navigate these dynamic conditions, focusing on companies where insiders are purchasing shares may signal confidence in their long-term prospects. Here are three such small-cap stocks in Australia that have caught our attention due to recent insider activity.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Corporate Travel Management | 19.6x | 2.3x | 8.07% | ★★★★★☆ |

| GWA Group | 15.7x | 1.5x | 44.06% | ★★★★★☆ |

| SHAPE Australia | 13.9x | 0.3x | 36.33% | ★★★★☆☆ |

| Elders | 23.8x | 0.5x | 47.16% | ★★★★☆☆ |

| Bapcor | NA | 0.8x | 48.06% | ★★★★☆☆ |

| Credit Corp Group | 20.5x | 2.7x | 41.61% | ★★★★☆☆ |

| Dicker Data | 20.4x | 0.7x | -66.82% | ★★★☆☆☆ |

| Coventry Group | 233.0x | 0.4x | -14.39% | ★★★☆☆☆ |

| BSP Financial Group | 7.8x | 2.8x | 2.06% | ★★★☆☆☆ |

| Abacus Group | NA | 6.1x | 23.55% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

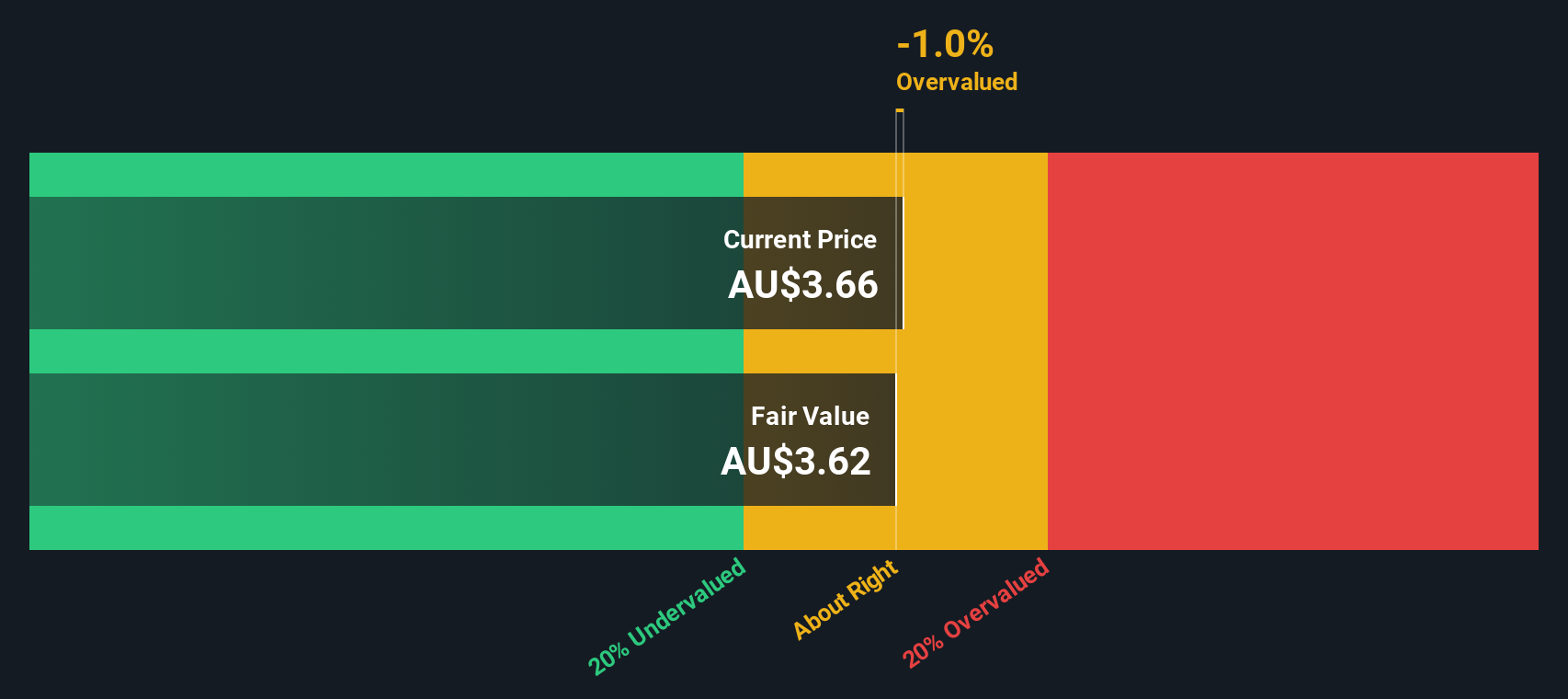

Deterra Royalties (ASX:DRR)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Deterra Royalties is a company focused on managing and acquiring royalty arrangements, with a market cap of approximately A$2.02 billion.

Operations: Deterra Royalties generates revenue primarily through royalty arrangements, with recent figures showing A$240.51 million. The company's cost of goods sold (COGS) was A$9.08 million, resulting in a gross profit margin of 96.22%. Operating expenses were A$3.98 million and non-operating expenses totaled A$72.56 million, contributing to a net income margin of 64.40%.

PE: 12.6x

Deterra Royalties, a small-cap stock in Australia, reported A$154.89 million net income for the year ending June 30, 2024, slightly up from A$152.46 million the previous year. Basic earnings per share increased to A$0.293 from A$0.2885. The company announced a dividend decrease to A$0.144 per share for the six months ending June 30, 2024, with an ex-dividend date of August 27, 2024. Insider confidence is evident with recent purchases over the past three months by key executives.

- Click to explore a detailed breakdown of our findings in Deterra Royalties' valuation report.

Assess Deterra Royalties' past performance with our detailed historical performance reports.

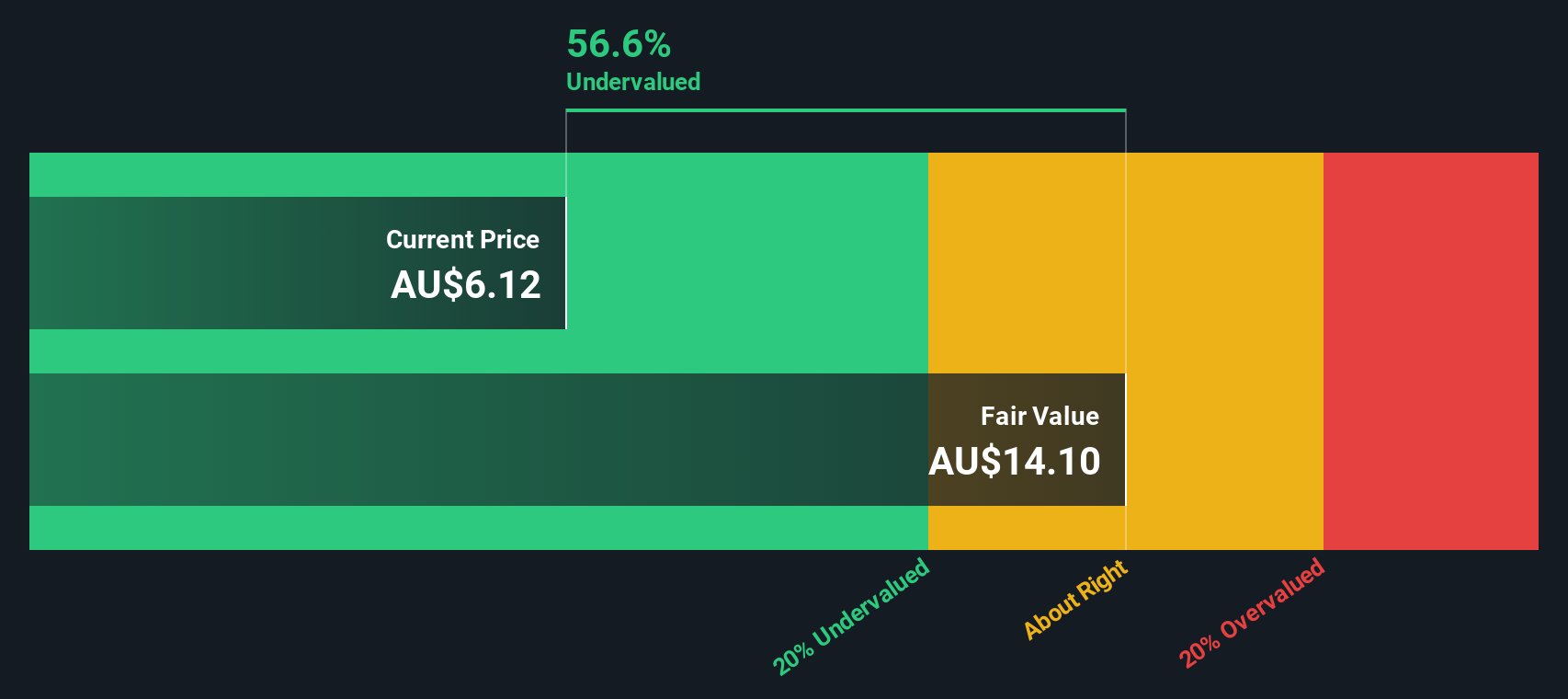

Elders (ASX:ELD)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Elders operates a diverse agribusiness network, providing products and services including branch networks, wholesale products, and feed and processing services, with a market cap of A$1.78 billion.

Operations: The company's revenue streams include A$2.54 billion from its Branch Network, A$341.19 million from Wholesale Products, and A$120.14 million from Feed and Processing Services. Over recent periods, net income margins have shown variability with a peak of 7.08% in September 2017 and a decline to 2.12% by March 2024. Operating expenses have consistently impacted profitability, with sales and marketing being the largest component within these costs.

PE: 23.8x

Elders, a small Australian agribusiness, has seen insider confidence with recent share purchases by executives in the past six months. Despite a dip in profit margins from 3.4% to 2.1%, earnings are projected to grow by 22.8% annually. The company recently appointed Glenn Davis as a non-executive director, bringing extensive board experience and legal expertise. However, Elders carries significant debt and relies entirely on external borrowing for funding, indicating higher financial risk.

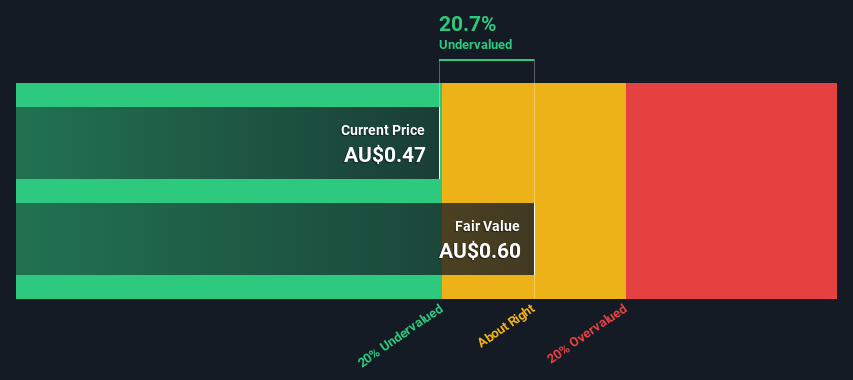

Tabcorp Holdings (ASX:TAH)

Simply Wall St Value Rating: ★★★★★☆

Overview: Tabcorp Holdings operates in the gaming services and wagering and media sectors, with a market cap of approximately A$5.40 billion.

Operations: Tabcorp Holdings generates revenue primarily from its Wagering and Media segment, which contributes A$2.16 billion, and its Gaming Services segment, which adds A$176.1 million. The company has experienced fluctuations in net income margin, with a notable decline to -0.5763% as of September 2024. Operating expenses have consistently been a significant portion of the costs, with sales and marketing expenses being particularly high at A$1.21 billion for the same period.

PE: -0.8x

Tabcorp Holdings, a notable player among Australia's smaller stocks, recently reported a net loss of A$1.36 billion for the fiscal year ending June 30, 2024, compared to a net income of A$66.5 million the previous year. Despite this downturn, insider confidence is evident with significant share purchases over the past six months. The company’s sales dipped slightly to A$2.34 billion from A$2.43 billion last year and announced a reduced dividend of A$0.003 per share payable on September 20, 2024.

Turning Ideas Into Actions

- Reveal the 25 hidden gems among our Undervalued ASX Small Caps With Insider Buying screener with a single click here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elders might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ELD

Elders

Provides agricultural products and services to rural and regional customers primarily in Australia.

Undervalued moderate.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor