- Australia

- /

- Hospitality

- /

- ASX:TAH

3 Undervalued ASX Small Caps With Notable Insider Action

Reviewed by Simply Wall St

The Australian market has recently faced headwinds, with the ASX 200 closing down 0.83% amid weak banking sector performances and economic uncertainties such as the Whyalla steelworks administration and slow wage growth. Despite these challenges, small-cap stocks on the ASX present intriguing opportunities, particularly when notable insider actions suggest potential value amidst broader market volatility.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Infomedia | 35.1x | 3.9x | 30.15% | ★★★★★★ |

| Abacus Storage King | 7.8x | 7.0x | 21.48% | ★★★★★☆ |

| nib holdings | 15.3x | 0.8x | 46.02% | ★★★★☆☆ |

| Autosports Group | 6.0x | 0.1x | 4.82% | ★★★★☆☆ |

| Abacus Group | NA | 5.6x | 24.34% | ★★★★☆☆ |

| Healius | NA | 0.6x | 0.77% | ★★★★☆☆ |

| SHAPE Australia | 16.6x | 0.3x | 17.02% | ★★★☆☆☆ |

| Collins Foods | 19.3x | 0.6x | -3.50% | ★★★☆☆☆ |

| Cromwell Property Group | NA | 5.2x | 17.65% | ★★★☆☆☆ |

| Tabcorp Holdings | NA | 0.6x | -13.21% | ★★★☆☆☆ |

We'll examine a selection from our screener results.

Amotiv (ASX:AOV)

Simply Wall St Value Rating: ★★★★★★

Overview: Amotiv specializes in manufacturing and supplying automotive components, with a focus on powertrain, undercar systems, lighting, electrical products, and 4WD accessories; it has a market cap of A$1.75 billion.

Operations: Amotiv generates revenue primarily from Powertrain & Undercar, Lighting Power & Electrical, and 4WD Accessories & Trailering segments. The company's gross profit margin has shown variability, reaching up to 57.13% but more recently around 44.92%. Operating expenses are driven by sales and marketing, R&D, and general administrative costs.

PE: 17.1x

Amotiv, a smaller Australian company, recently appointed Ms. Raelene Murphy as an independent Non-Executive Director and Chair of the Audit Committee, effective March 2025. This strategic move aims to bolster corporate governance and risk management. Despite a drop in net income to A$33 million for H1 2024 from A$50.2 million the previous year, sales increased slightly to A$503.7 million. The company announced a fully franked interim dividend of A$0.185 per share for 2025, reflecting shareholder commitment amidst insider confidence through share purchases earlier this year suggests potential growth prospects with earnings projected to rise by 14.64% annually.

- Dive into the specifics of Amotiv here with our thorough valuation report.

Examine Amotiv's past performance report to understand how it has performed in the past.

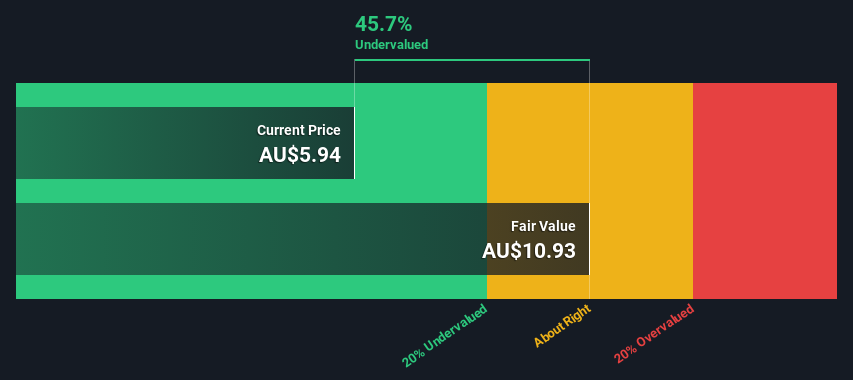

nib holdings (ASX:NHF)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nib holdings is a health and medical insurance provider operating primarily in Australia and New Zealand, with a market capitalization of A$3.33 billion.

Operations: The company's revenue is primarily derived from Australian Residents Health Insurance, contributing A$2.65 billion, and New Zealand Insurance with A$373.1 million. International (Inbound) Health Insurance adds A$203.5 million to the revenue stream, while NIB Travel and Nib Thrive contribute A$96.8 million and A$51.3 million respectively. The gross profit margin has shown variability, reaching 22.73% in December 2023 before decreasing to 13.57% by June 2024.

PE: 15.3x

Nib Holdings, a key player in the Australian health insurance sector, is attracting attention due to its perceived undervaluation. The company forecasts annual earnings growth of 6.25%, suggesting potential for future expansion. However, reliance on external borrowing introduces higher risk compared to firms with customer deposits. Insider confidence was demonstrated with recent share purchases by executives, indicating belief in the company's prospects. Additionally, Edward Close's appointment as director in December 2024 could bring fresh strategic insights.

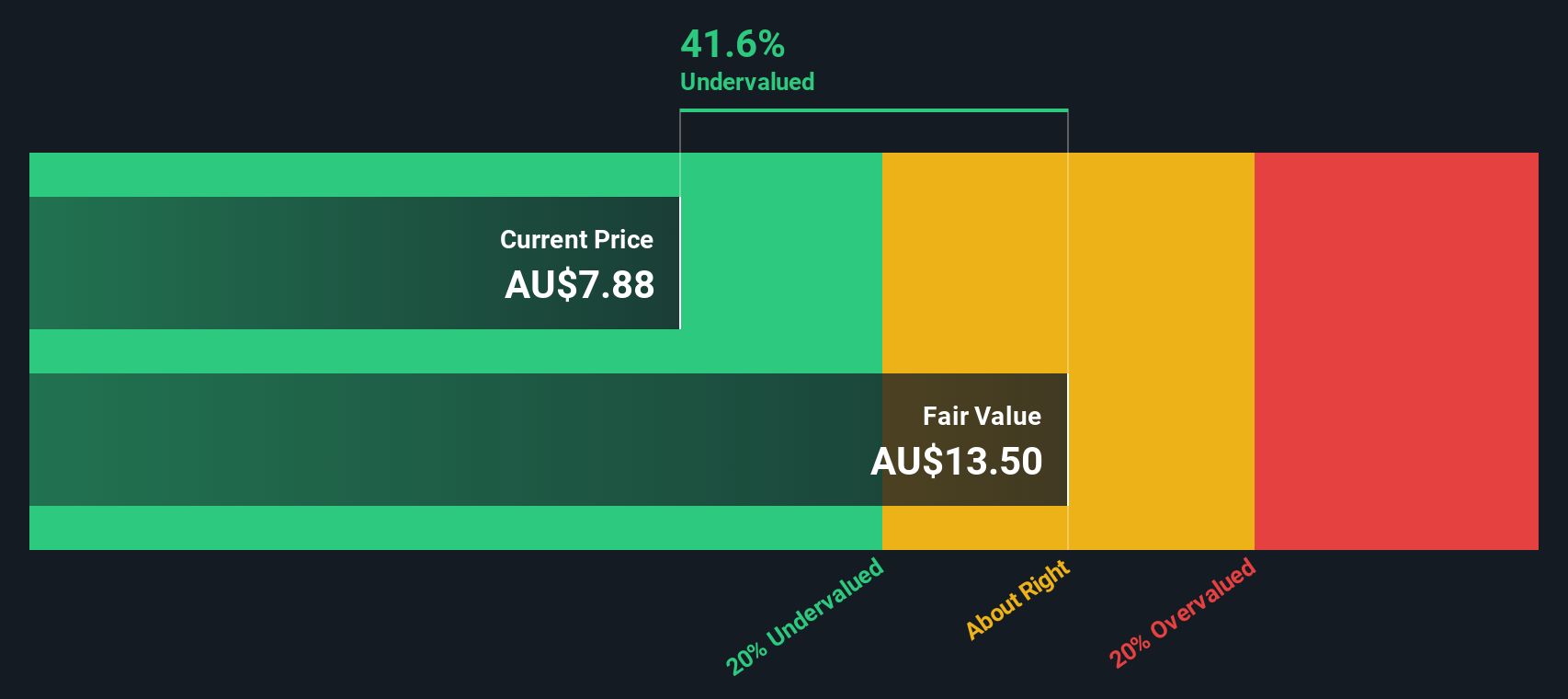

Tabcorp Holdings (ASX:TAH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Tabcorp Holdings is an Australian company primarily engaged in providing wagering and media services, with a smaller segment focused on gaming services, and has a market capitalization of approximately A$4.57 billion.

Operations: The primary revenue streams are Wagering and Media, generating A$2.16 billion, and Gaming Services at A$176.1 million. The gross profit margin consistently stands at 100%, indicating no direct costs of goods sold impacting gross profit figures across the periods provided. Operating expenses include significant allocations to sales and marketing, with recent figures around A$1.21 billion, along with general and administrative expenses approximately at A$459.4 million in the latest period analyzed.

PE: -1.1x

Tabcorp Holdings, a key player in Australia's wagering sector, has been making strategic leadership changes to bolster its growth. Recent appointments include Michael Fitzsimons as Chief Wagering Officer and Gillon McLachlan as Director. Insider confidence is evident with Adam Rytenskild purchasing 200,000 shares for A$136,000 in early February 2025. Despite having less than a year of cash runway and relying on higher-risk funding sources, earnings are projected to grow by over 113% annually.

- Click here to discover the nuances of Tabcorp Holdings with our detailed analytical valuation report.

Understand Tabcorp Holdings' track record by examining our Past report.

Seize The Opportunity

- Unlock our comprehensive list of 18 Undervalued ASX Small Caps With Insider Buying by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tabcorp Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TAH

Tabcorp Holdings

Provides gambling and entertainment services in Australia.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Community Narratives