- Australia

- /

- Food and Staples Retail

- /

- ASX:WOW

How Disappointing FY25 Results and a Higher Yield at Woolworths (ASX:WOW) Has Changed Its Investment Story

Reviewed by Sasha Jovanovic

- Woolworths Group recently reported disappointing FY 2025 results, leading to a significant decline in its share price and market sentiment.

- An important insight is the company's dividend yield has risen above its 5-year average, highlighting the impact of shifting investor expectations or share price movement.

- We'll explore how management's plans to restore profit growth and address margin pressures could alter Woolworths Group's investment outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Woolworths Group Investment Narrative Recap

To be a Woolworths Group shareholder, you need confidence in its ability to defend market share and restore margins through operational improvements, strong execution, and ongoing cost discipline, especially after the recent sharp selloff. Although the disappointing FY25 results triggered the share price drop, the main short term catalyst remains management’s plans to deliver profit growth in FY26, while the biggest near-term risk is that continued margin pressure and competitive intensity could limit the bounce back, this risk has clearly come into sharper focus after recent events.

Among recent announcements, Woolworths revealed a fully franked ordinary dividend of A$0.45 per share for the last half-year, despite net profit margins and earnings receiving a boost from one-off items. The higher dividend yield, now above its five-year average, reflects either the drop in share price or changes in payout, not a conclusive signal of improved future profitability, yet it is a relevant metric as investors weigh the sustainability of ongoing capital returns against margin recovery as a near-term catalyst.

But with Woolworths’ high debt levels now even more important after its latest profit shortfall, investors should be aware that...

Read the full narrative on Woolworths Group (it's free!)

Woolworths Group's projections indicate A$77.0 billion in revenue and A$1.9 billion in earnings by 2028. This outlook is based on annual revenue growth of 3.7% and an earnings increase of A$937 million from the current A$963.0 million.

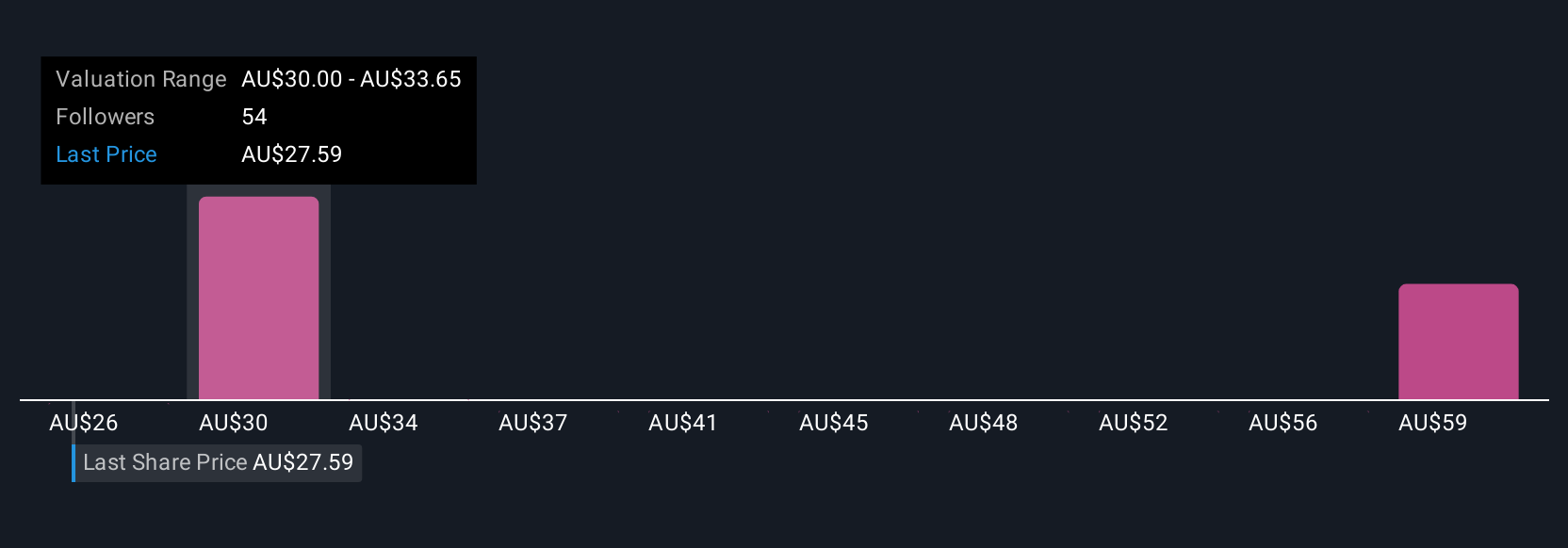

Uncover how Woolworths Group's forecasts yield a A$30.51 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members produced nine fair value estimates for Woolworths Group, ranging widely from A$26.35 to A$61.76 per share. Given ongoing concerns about margin pressure from fierce competition and elevated costs, perspectives on the company’s forward performance differ substantially, explore more alternative viewpoints to inform your decision.

Explore 9 other fair value estimates on Woolworths Group - why the stock might be worth over 2x more than the current price!

Build Your Own Woolworths Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Woolworths Group research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Woolworths Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Woolworths Group's overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Rare earth metals are the new gold rush. Find out which 35 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Woolworths Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:WOW

Moderate growth potential with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)