- Australia

- /

- Consumer Durables

- /

- ASX:BRG

Increases to Breville Group Limited's (ASX:BRG) CEO Compensation Might Cool off for now

Performance at Breville Group Limited (ASX:BRG) has been reasonably good and CEO Jim Clayton has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 09 November 2022. However, some shareholders will still be cautious of paying the CEO excessively.

Our analysis indicates that BRG is potentially overvalued!

Comparing Breville Group Limited's CEO Compensation With The Industry

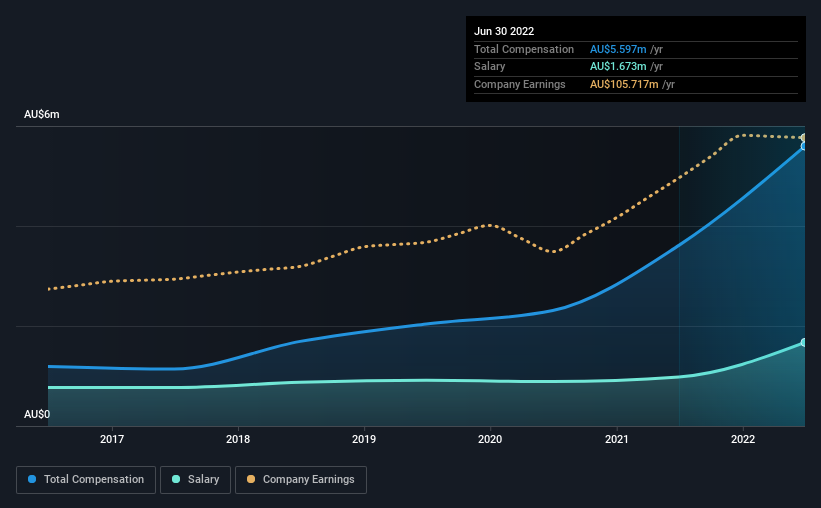

Our data indicates that Breville Group Limited has a market capitalization of AU$2.9b, and total annual CEO compensation was reported as AU$5.6m for the year to June 2022. That's a notable increase of 55% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at AU$1.7m.

On comparing similar companies from the same industry with market caps ranging from AU$1.6b to AU$5.0b, we found that the median CEO total compensation was AU$2.9m. Hence, we can conclude that Jim Clayton is remunerated higher than the industry median. Moreover, Jim Clayton also holds AU$5.6m worth of Breville Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | AU$1.7m | AU$980k | 30% |

| Other | AU$3.9m | AU$2.6m | 70% |

| Total Compensation | AU$5.6m | AU$3.6m | 100% |

On an industry level, around 56% of total compensation represents salary and 44% is other remuneration. Breville Group pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Breville Group Limited's Growth

Breville Group Limited's earnings per share (EPS) grew 13% per year over the last three years. In the last year, its revenue is up 19%.

Shareholders would be glad to know that the company has improved itself over the last few years. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Breville Group Limited Been A Good Investment?

Breville Group Limited has served shareholders reasonably well, with a total return of 32% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We did our research and identified 2 warning signs (and 1 which makes us a bit uncomfortable) in Breville Group we think you should know about.

Important note: Breville Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Breville Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:BRG

Breville Group

Designs, develops, markets, and distributes small electrical kitchen appliances in the consumer products industry in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives