Advertisement

Why We Think Zicom Group Limited's (ASX:ZGL) CEO Compensation Is Not Excessive At All

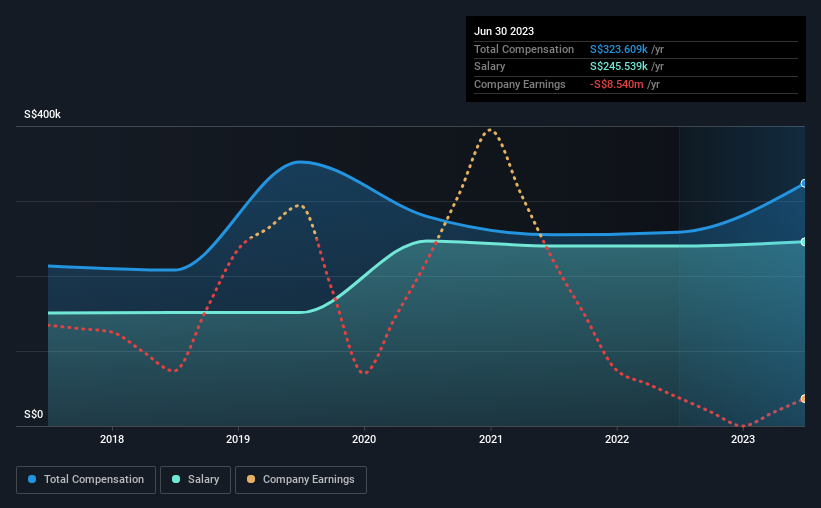

Key Insights

- Zicom Group will host its Annual General Meeting on 27th of November

- Total pay for CEO Yew Sim Kok includes S$245.5k salary

- The total compensation is 50% less than the average for the industry

- Over the past three years, Zicom Group's EPS fell by 81% and over the past three years, the total shareholder return was 4.2%

The performance at Zicom Group Limited (ASX:ZGL) has been rather lacklustre of late and shareholders may be wondering what CEO Yew Sim Kok is planning to do about this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 27th of November. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

View our latest analysis for Zicom Group

Comparing Zicom Group Limited's CEO Compensation With The Industry

According to our data, Zicom Group Limited has a market capitalization of AU$11m, and paid its CEO total annual compensation worth S$324k over the year to June 2023. That's a notable increase of 25% on last year. Notably, the salary which is S$245.5k, represents most of the total compensation being paid.

In comparison with other companies in the Australian Machinery industry with market capitalizations under AU$305m, the reported median total CEO compensation was S$643k. In other words, Zicom Group pays its CEO lower than the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | S$246k | S$240k | 76% |

| Other | S$78k | S$18k | 24% |

| Total Compensation | S$324k | S$258k | 100% |

Speaking on an industry level, nearly 53% of total compensation represents salary, while the remainder of 47% is other remuneration. It's interesting to note that Zicom Group pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Zicom Group Limited's Growth

Over the last three years, Zicom Group Limited has shrunk its earnings per share by 81% per year. In the last year, its revenue is up 1.8%.

Few shareholders would be pleased to read that EPS have declined. The fairly low revenue growth fails to impress given that the EPS is down. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Zicom Group Limited Been A Good Investment?

With a total shareholder return of 4.2% over three years, Zicom Group Limited has done okay by shareholders, but there's always room for improvement. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

To Conclude...

While it's true that shareholders have seen decent returns, it's hard to overlook the lack of earnings growth and this makes us wonder if the current returns can continue. These concerns could be addressed to the board and shareholders should revisit their investment thesis to see if it still makes sense.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 4 warning signs for Zicom Group that investors should think about before committing capital to this stock.

Switching gears from Zicom Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Zicom Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ZGL

Zicom Group

Manufactures and sells marine deck machinery, fluid regulating and metering stations, transit concrete mixers, foundation and geotechnical equipment, and precision engineered and automation equipment in Australia, the Philippines, Singapore, China, Bangladesh, and internationally.

Slight with acceptable track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor