- Australia

- /

- Aerospace & Defense

- /

- ASX:EOS

Electro Optic Systems (ASX:EOS): Rethinking Valuation After Special Contract Call Spurs Investor Interest

Reviewed by Simply Wall St

Electro Optic Systems Holdings (ASX:EOS) has grabbed investor attention after hosting a special call on December 14 to outline a new contract announcement, prompting fresh questions about earnings visibility and longer term growth.

See our latest analysis for Electro Optic Systems Holdings.

The timing of this contract focused call helps explain why Electro Optic Systems Holdings has seen such explosive momentum lately, with a 7 day share price return of 56.88 percent and a 1 year total shareholder return of 572.32 percent. This suggests sentiment has flipped decisively in favour of a longer term recovery story from earlier weakness.

If this defence and space contract win has you rethinking the sector, it could be worth scanning other aerospace and defense stocks that might be quietly setting up for the next leg higher.

With EOS up more than 570 percent over the past year yet still trading below some estimates of intrinsic value, are investors looking at a rare mispriced turnaround, or is the market already banking on years of growth ahead?

Most Popular Narrative: 2.4% Undervalued

With Electro Optic Systems Holdings last closing at A$7.53 against a narrative fair value of A$7.72, the valuation case hinges on rapid operational improvement and sustained growth.

Analysts are assuming Electro Optic Systems Holdings's revenue will grow by 30.0% annually over the next 3 years.

Analysts assume that profit margins will increase from -59.1% today to 10.0% in 3 years time.

Want to see how a loss making defense contractor is being modeled into a profitable growth story with expanding margins and a premium earnings multiple? The narrative leans on aggressive revenue ramps, a sharp swing in profitability, and a valuation framework more often reserved for market favorites. Curious which specific milestones and financial jumps need to fall into place to justify that fair value? Read on to unpack the full narrative behind these bold projections.

Result: Fair Value of $7.72 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat scenario could unravel if defense spending normalizes faster than expected, or if rival contractors outmuscle EOS in counter drone and laser systems.

Find out about the key risks to this Electro Optic Systems Holdings narrative.

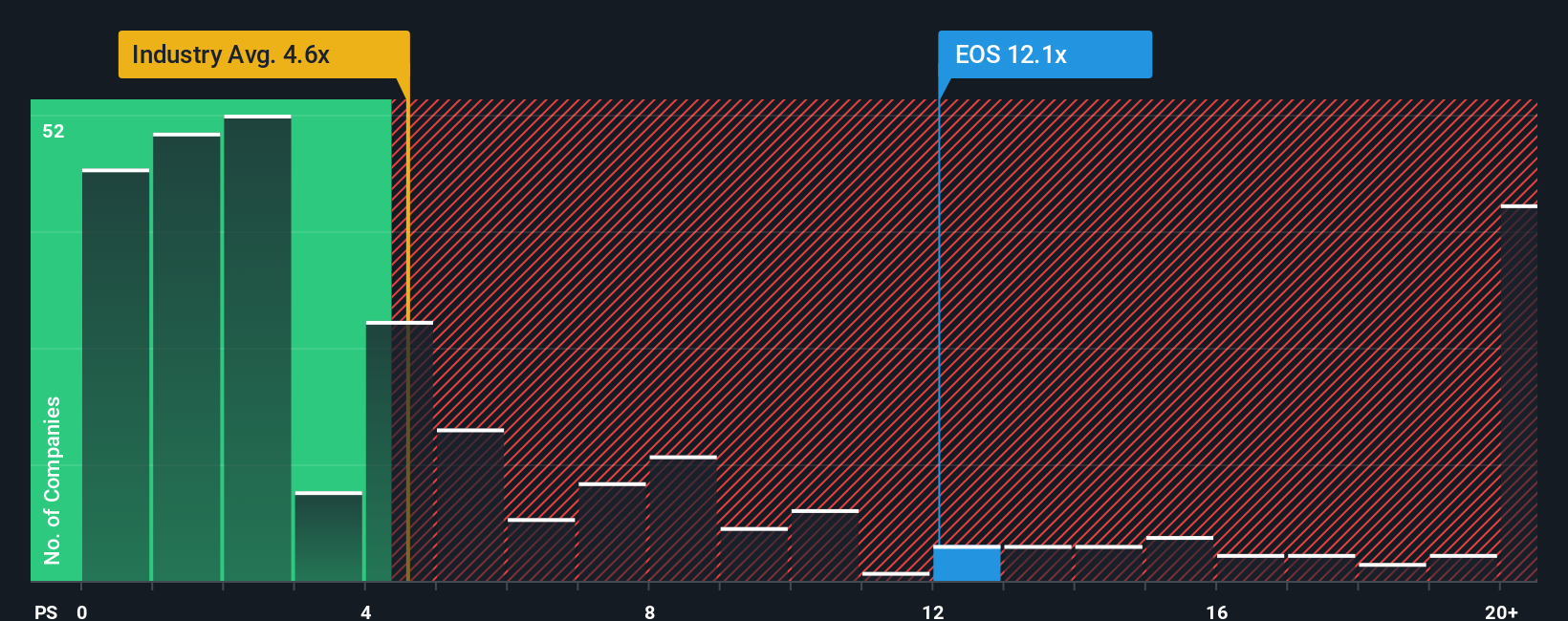

Another View: Sales Multiple Flashes Caution

While the narrative fair value suggests EOS is modestly undervalued, the price tag looks far richer when you zoom in on sales. At 12.6 times revenue, EOS trades at almost double peers on 6.5 times and above its own fair ratio of 11 times. This implies much less margin for error if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Electro Optic Systems Holdings Narrative

If this perspective does not quite match your own thinking and you would rather examine the numbers yourself, you can create a custom view in just a few minutes, Do it your way

A great starting point for your Electro Optic Systems Holdings research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for your next investing edge?

Use the Simply Wall St Screener to pinpoint stocks that match your strategy, so you are not left watching others capitalize on the next wave of winners.

- Secure reliable income potential by targeting these 12 dividend stocks with yields > 3% that can help strengthen the foundation of your long term portfolio.

- Ride the innovation surge by focusing on these 26 AI penny stocks positioned at the forefront of artificial intelligence and automation trends.

- Capitalize on market mispricing by zeroing in on these 912 undervalued stocks based on cash flows where cash flow strength is not yet fully reflected in share prices.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Electro Optic Systems Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:EOS

Electro Optic Systems Holdings

Engages in the development, manufacture, and sale of telescopes and dome enclosures, laser satellite tracking systems, and remote weapon systems.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)