Advertisement

- Australia

- /

- Trade Distributors

- /

- ASX:BMH

Here's Why We're Watching Baumart Holdings' (ASX:BMH) Cash Burn Situation

Just because a business does not make any money, does not mean that the stock will go down. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should Baumart Holdings (ASX:BMH) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business' cash, relative to its cash burn.

See our latest analysis for Baumart Holdings

How Long Is Baumart Holdings' Cash Runway?

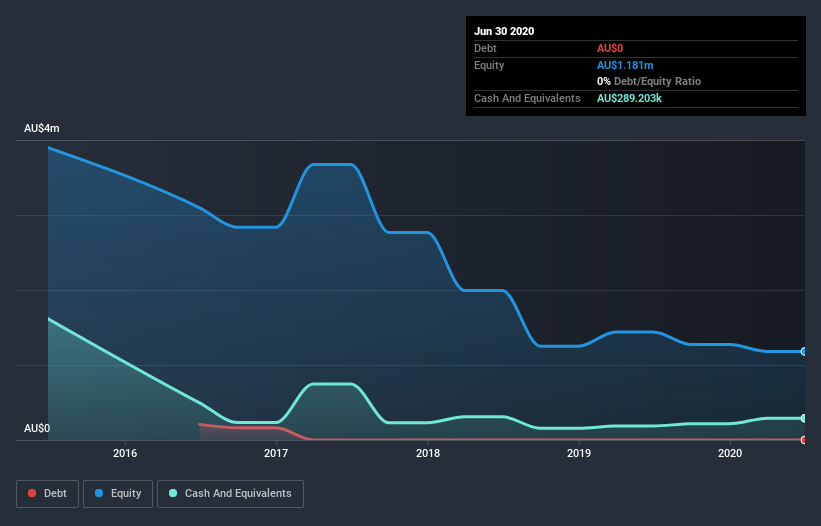

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at June 2020, Baumart Holdings had cash of AU$289k and no debt. In the last year, its cash burn was AU$270k. Therefore, from June 2020 it had roughly 13 months of cash runway. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. You can see how its cash balance has changed over time in the image below.

How Well Is Baumart Holdings Growing?

Notably, Baumart Holdings actually ramped up its cash burn very hard and fast in the last year, by 161%, signifying heavy investment in the business. On top of that, the fact that operating revenue was basically flat over the same period compounds the concern. In light of the above-mentioned, we're pretty wary of the trajectory the company seems to be on. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how Baumart Holdings is building its business over time.

How Easily Can Baumart Holdings Raise Cash?

Baumart Holdings revenue is declining and its cash burn is increasing, so many may be considering its need to raise more cash in the future. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Baumart Holdings' cash burn of AU$270k is about 1.0% of its AU$26m market capitalisation. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

So, Should We Worry About Baumart Holdings' Cash Burn?

Even though its increasing cash burn makes us a little nervous, we are compelled to mention that we thought Baumart Holdings' cash burn relative to its market cap was relatively promising. Even though we don't think it has a problem with its cash burn, the analysis we've done in this article does suggest that shareholders should give some careful thought to the potential cost of raising more money in the future. An in-depth examination of risks revealed 2 warning signs for Baumart Holdings that readers should think about before committing capital to this stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you decide to trade Baumart Holdings, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Baumart Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:BMH

Baumart Holdings

Baumart Holdings Limited, together with its subsidiaries, procures and supplies building products and materials for the residential and commercial property construction markets in Australia.

Moderate with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

CSL is undervalued in High Tax Scenario

Fair Value AU$263.33|10.2% undervalued

RA

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor