With EPS Growth And More, Westpac Banking (ASX:WBC) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Westpac Banking (ASX:WBC). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

Check out our latest analysis for Westpac Banking

How Quickly Is Westpac Banking Increasing Earnings Per Share?

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. That means EPS growth is considered a real positive by most successful long-term investors. Westpac Banking managed to grow EPS by 10% per year, over three years. That's a pretty good rate, if the company can sustain it.

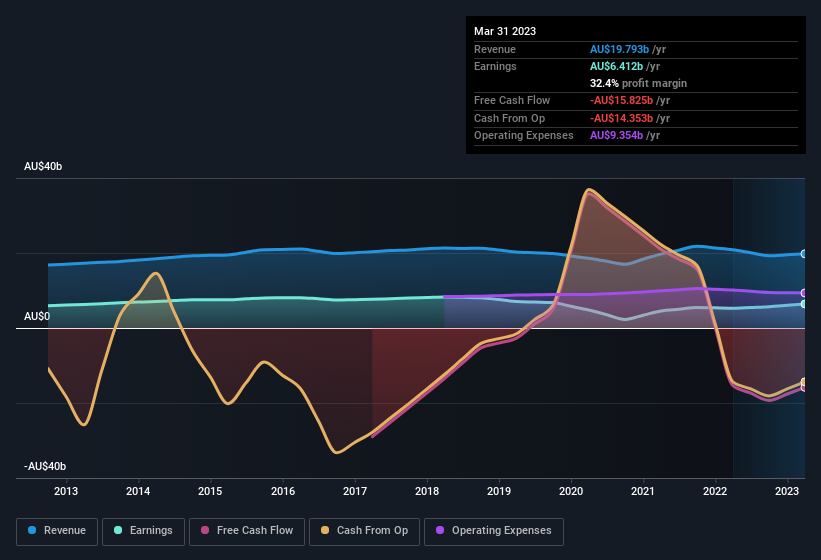

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. It's noted that Westpac Banking's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. Despite consistency in EBIT margins year on year, Westpac Banking has actually recorded a dip in revenue. This does not bode too well for short term growth prospects and so understanding the reasons for these results is of great importance.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Westpac Banking's future EPS 100% free.

Are Westpac Banking Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

With strong conviction, Westpac Banking insiders have stood united by refusing to sell shares over the last year. But more importantly, Independent Non-Executive Director Nora Scheinkestel spent AU$99k acquiring shares, doing so at an average price of AU$22.26. Purchases like this clue us in to the to the faith management has in the business' future.

On top of the insider buying, it's good to see that Westpac Banking insiders have a valuable investment in the business. As a matter of fact, their holding is valued at AU$21m. That shows significant buy-in, and may indicate conviction in the business strategy. While their ownership only accounts for 0.03%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because on our analysis the CEO, Peter King, is paid less than the median for similar sized companies. Our analysis has discovered that the median total compensation for the CEOs of companies like Westpac Banking, with market caps over AU$12b, is about AU$5.7m.

Westpac Banking offered total compensation worth AU$5.0m to its CEO in the year to September 2022. That is actually below the median for CEO's of similarly sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of a culture of integrity, in a broader sense.

Is Westpac Banking Worth Keeping An Eye On?

As previously touched on, Westpac Banking is a growing business, which is encouraging. Better yet, insiders are significant shareholders, and have been buying more shares. That should do plenty in prompting budding investors to undertake a bit more research - or even adding the company to their watchlists. It's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Westpac Banking (at least 1 which doesn't sit too well with us) , and understanding these should be part of your investment process.

Keen growth investors love to see insider buying. Thankfully, Westpac Banking isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Westpac Banking might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:WBC

Westpac Banking

Provides banking and other financial services in Australia, New Zealand, the Pacific Islands, Asia, the Americas, and Europe.

Excellent balance sheet with proven track record.

Similar Companies

Market Insights

Community Narratives