Advertisement

The ASX200 is set to open more than one percent higher, reflecting a positive sentiment despite mixed performances on Wall Street, where investors are navigating company earnings and ongoing trade uncertainties. In such a fluctuating market landscape, identifying stocks with strong fundamentals becomes crucial for investors seeking stability and growth. Penny stocks, often representing smaller or newer companies, can offer surprising value when backed by solid financial foundations, making them an intriguing area to explore for potential opportunities.

Top 10 Penny Stocks In Australia

| Name | Share Price | Market Cap | Rewards & Risks |

| Lindsay Australia (ASX:LAU) | A$0.705 | A$223.61M | ✅ 4 ⚠️ 2 View Analysis > |

| CTI Logistics (ASX:CLX) | A$1.83 | A$147.4M | ✅ 4 ⚠️ 2 View Analysis > |

| Accent Group (ASX:AX1) | A$1.95 | A$1.17B | ✅ 4 ⚠️ 2 View Analysis > |

| EZZ Life Science Holdings (ASX:EZZ) | A$1.60 | A$75.48M | ✅ 4 ⚠️ 2 View Analysis > |

| IVE Group (ASX:IGL) | A$2.68 | A$413.21M | ✅ 4 ⚠️ 2 View Analysis > |

| GTN (ASX:GTN) | A$0.615 | A$117.51M | ✅ 3 ⚠️ 2 View Analysis > |

| GR Engineering Services (ASX:GNG) | A$2.76 | A$461.9M | ✅ 2 ⚠️ 1 View Analysis > |

| Bisalloy Steel Group (ASX:BIS) | A$3.30 | A$156.59M | ✅ 3 ⚠️ 1 View Analysis > |

| Regal Partners (ASX:RPL) | A$2.20 | A$739.56M | ✅ 4 ⚠️ 4 View Analysis > |

| Navigator Global Investments (ASX:NGI) | A$1.745 | A$855.19M | ✅ 5 ⚠️ 3 View Analysis > |

Click here to see the full list of 997 stocks from our ASX Penny Stocks screener.

Here's a peek at a few of the choices from the screener.

Optiscan Imaging (ASX:OIL)

Simply Wall St Financial Health Rating: ★★★★★☆

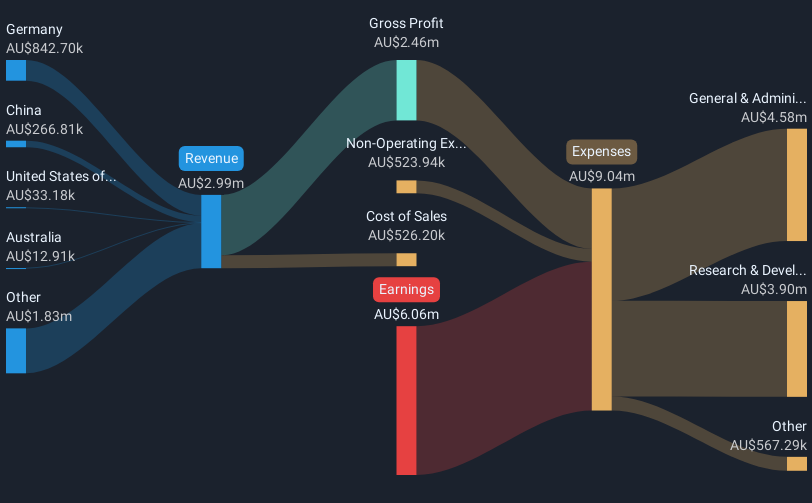

Overview: Optiscan Imaging Limited develops, manufactures, and commercializes endomicroscopic digital imaging technology for medical and pre-clinical applications across Australia, Germany, China, and the United States with a market cap of A$108.59 million.

Operations: Optiscan Imaging generates revenue of A$4.96 million from its Confocal Microscopes segment.

Market Cap: A$108.59M

Optiscan Imaging, with a market cap of A$108.59 million, remains unprofitable despite generating A$4.96 million in revenue from its Confocal Microscopes segment. The company has seen earnings decline by 25.2% annually over the past five years and maintains a negative return on equity of -42.98%. Recent executive changes aim to enhance strategic execution and product development, including appointing Darius Ooi as CFO and Belinda Williamson as Chief Commercial Officer to strengthen sales efforts. Optiscan's cash runway exceeds one year, but its share price remains highly volatile compared to most Australian stocks.

- Click here to discover the nuances of Optiscan Imaging with our detailed analytical financial health report.

- Gain insights into Optiscan Imaging's historical outcomes by reviewing our past performance report.

Southern Cross Media Group (ASX:SXL)

Simply Wall St Financial Health Rating: ★★★★☆☆

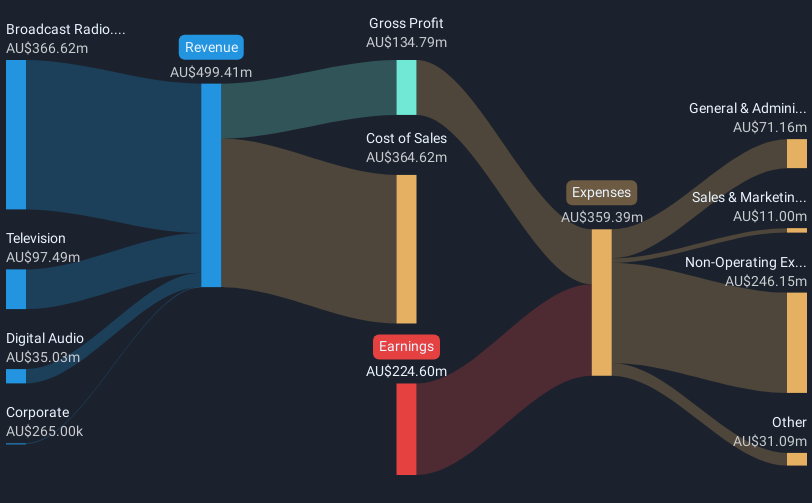

Overview: Southern Cross Media Group Limited, with a market cap of A$179.92 million, creates audio content for distribution across broadcast and digital networks in Australia.

Operations: The company's revenue is primarily derived from its Broadcast Radio segment, generating A$370.70 million, complemented by Digital Audio revenue of A$41.57 million.

Market Cap: A$179.92M

Southern Cross Media Group, with a market cap of A$179.92 million, faces challenges as it remains unprofitable despite generating significant revenue from its Broadcast Radio and Digital Audio segments. The company has a sufficient cash runway for over three years even if free cash flow shrinks annually by 26.4%. Trading at 22.3% below estimated fair value, it offers potential relative value but struggles with high net debt to equity at 45%. Recent investor activism may distract from operational focus, though plans to resume dividends in FY25 reflect improved financial discipline and leverage management below 1.5x forecasted by June 2025.

- Navigate through the intricacies of Southern Cross Media Group with our comprehensive balance sheet health report here.

- Assess Southern Cross Media Group's future earnings estimates with our detailed growth reports.

Vmoto (ASX:VMT)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Vmoto Limited develops, manufactures, markets, and distributes electric two-wheel vehicles globally with a market cap of A$38.11 million.

Operations: The company generates revenue of A$57.19 million from its electric two-wheel vehicles manufacture and distribution industry.

Market Cap: A$38.11M

Vmoto Limited, with a market cap of A$38.11 million, is navigating challenges as it remains unprofitable despite generating revenue of A$57.19 million from its electric two-wheel vehicles globally. The company faces declining sales, with a 16% drop in units sold in Q1 2025 compared to the previous year. While short-term assets exceed liabilities and cash surpasses total debt, the company's high share price volatility and negative return on equity highlight financial instability. Recent shareholder activism has not resulted in board changes, indicating potential governance concerns amid operational hurdles.

- Get an in-depth perspective on Vmoto's performance by reading our balance sheet health report here.

- Explore historical data to track Vmoto's performance over time in our past results report.

Taking Advantage

- Dive into all 997 of the ASX Penny Stocks we have identified here.

- Curious About Other Options? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:VMT

Vmoto

Engages in the development, manufacture, marketing, and distribution of electric two-wheel vehicles worldwide.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor