Most Shareholders Will Probably Agree With UNIQA Insurance Group AG's (VIE:UQA) CEO Compensation

Key Insights

- UNIQA Insurance Group's Annual General Meeting to take place on 3rd of June

- Total pay for CEO Andreas Brandstetter includes €748.0k salary

- Total compensation is similar to the industry average

- Over the past three years, UNIQA Insurance Group's EPS grew by 155% and over the past three years, the total shareholder return was 32%

CEO Andreas Brandstetter has done a decent job of delivering relatively good performance at UNIQA Insurance Group AG (VIE:UQA) recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 3rd of June. Here is our take on why we think the CEO compensation looks appropriate.

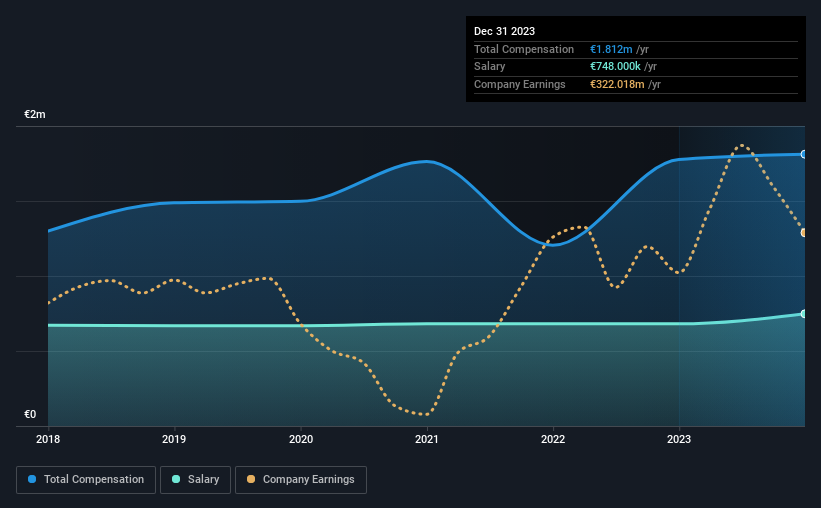

View our latest analysis for UNIQA Insurance Group

Comparing UNIQA Insurance Group AG's CEO Compensation With The Industry

According to our data, UNIQA Insurance Group AG has a market capitalization of €2.5b, and paid its CEO total annual compensation worth €1.8m over the year to December 2023. That's mostly flat as compared to the prior year's compensation. While we always look at total compensation first, our analysis shows that the salary component is less, at €748k.

For comparison, other companies in the Austria Insurance industry with market capitalizations ranging between €1.8b and €5.9b had a median total CEO compensation of €1.8m. So it looks like UNIQA Insurance Group compensates Andreas Brandstetter in line with the median for the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | €748k | €681k | 41% |

| Other | €1.1m | €1.1m | 59% |

| Total Compensation | €1.8m | €1.8m | 100% |

On an industry level, around 41% of total compensation represents salary and 59% is other remuneration. There isn't a significant difference between UNIQA Insurance Group and the broader market, in terms of salary allocation in the overall compensation package. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at UNIQA Insurance Group AG's Growth Numbers

Over the past three years, UNIQA Insurance Group AG has seen its earnings per share (EPS) grow by 155% per year. Its revenue is up 17% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has UNIQA Insurance Group AG Been A Good Investment?

UNIQA Insurance Group AG has served shareholders reasonably well, with a total return of 32% over three years. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We've identified 1 warning sign for UNIQA Insurance Group that investors should be aware of in a dynamic business environment.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WBAG:UQA

UNIQA Insurance Group

Operates as an insurance company in Austria and Central and Eastern Europe.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Clarivate Stock: When Data Becomes the Backbone of Innovation and Law

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

MicroVision will explode future revenue by 380.37% with a vision towards success

Trending Discussion