Advertisement

European Growth Companies With High Insider Ownership March 2025

Simply Wall St

Reviewed by Simply Wall St

As European markets continue to show resilience, with the STOXX Europe 600 Index achieving its longest streak of weekly gains since August 2012, investors are increasingly drawn to growth companies with substantial insider ownership. In this context, stocks that combine robust growth potential and significant insider stakes can offer a compelling proposition for those looking to navigate the current economic landscape marked by mixed inflation signals and geopolitical uncertainties.

Top 10 Growth Companies With High Insider Ownership In Europe

| Name | Insider Ownership | Earnings Growth |

| TF Bank (OM:TFBANK) | 15.6% | 20% |

| Elicera Therapeutics (OM:ELIC) | 27.8% | 97.2% |

| Vow (OB:VOW) | 12.9% | 120.9% |

| Pharma Mar (BME:PHM) | 11.9% | 40.1% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| Bergen Carbon Solutions (OB:BCS) | 12% | 50.8% |

| Ortoma (OM:ORT B) | 27.7% | 73.4% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 89.9% |

| MedinCell (ENXTPA:MEDCL) | 13.9% | 114.3% |

| Circus (XTRA:CA1) | 26% | 51.4% |

Here's a peek at a few of the choices from the screener.

Promotora de Informaciones (BME:PRS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Promotora de Informaciones, S.A., along with its subsidiaries, operates in the media sector both in Spain and internationally, with a market cap of €418.23 million.

Operations: The company generates revenue through its Media segment, which accounts for €443.36 million, and its Education segment, contributing €467.02 million.

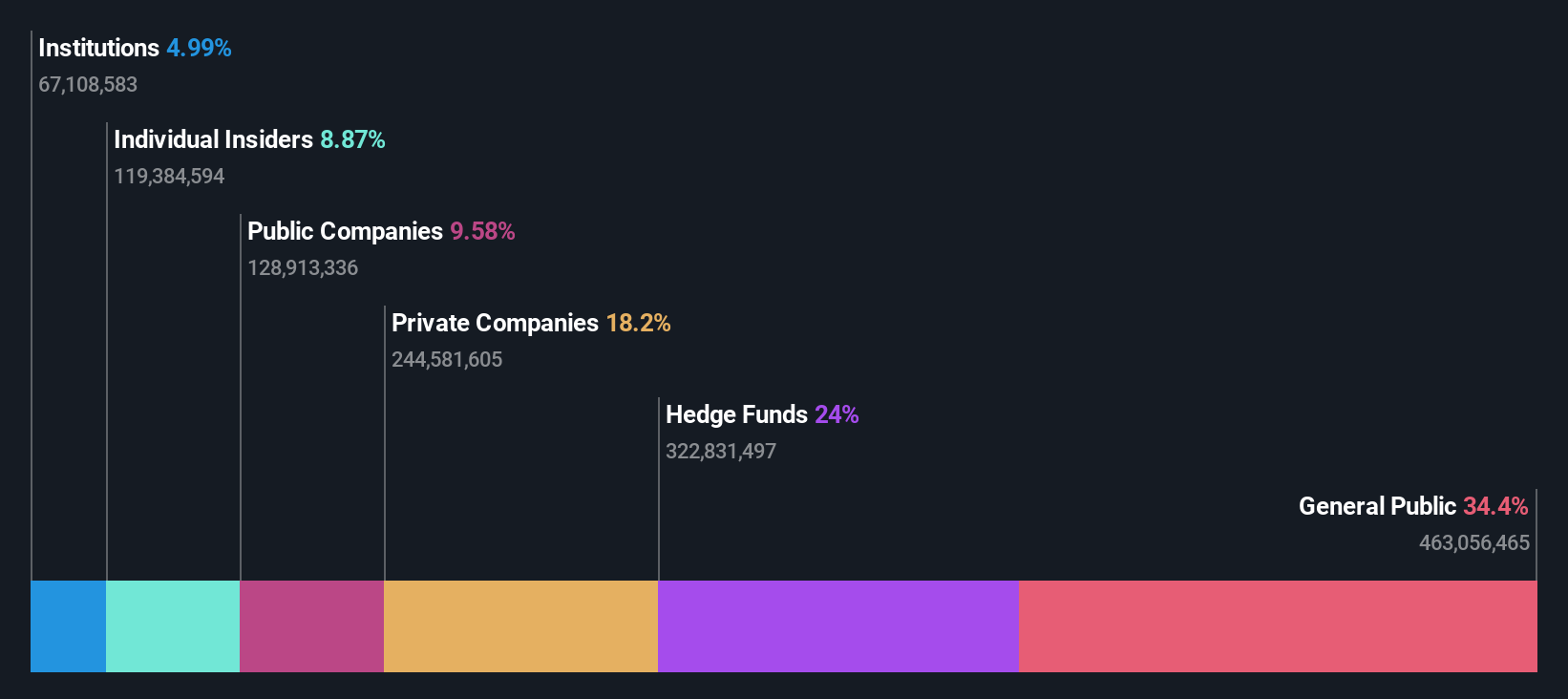

Insider Ownership: 13.3%

Earnings Growth Forecast: 132.9% p.a.

Promotora de Informaciones, S.A. demonstrates potential as a growth company with high insider ownership in Europe. Despite recent volatility and negative shareholders' equity, the firm's earnings have shown significant improvement, with a notable increase in net income for Q4 2024 to €25.7 million from €4.2 million the previous year. While revenue forecasts suggest growth faster than the Spanish market at 7.4% annually, profitability is expected within three years, outpacing average market expectations.

- Take a closer look at Promotora de Informaciones' potential here in our earnings growth report.

- Our expertly prepared valuation report Promotora de Informaciones implies its share price may be lower than expected.

Lime Technologies (OM:LIME)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Lime Technologies AB (publ) offers SaaS-based CRM solutions in the Nordic region, with a market cap of approximately SEK4.86 billion.

Operations: The company's revenue is primarily derived from selling and implementing CRM software systems, amounting to SEK685.75 million.

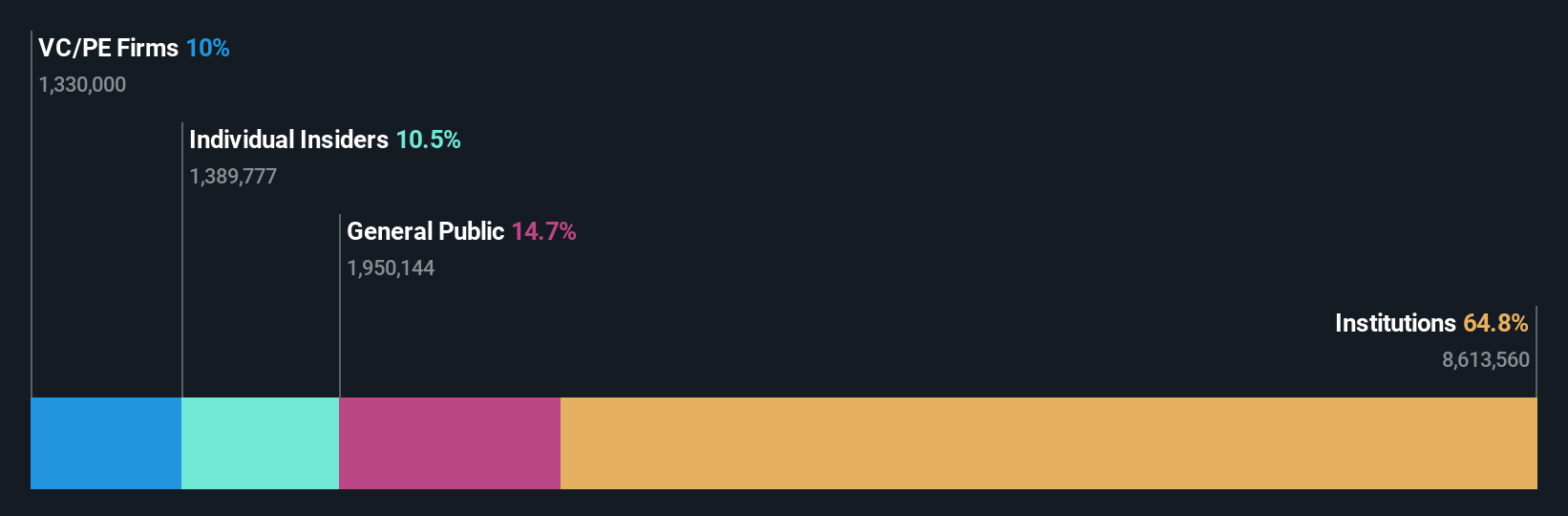

Insider Ownership: 10.7%

Earnings Growth Forecast: 24% p.a.

Lime Technologies shows potential for growth with high insider ownership in Europe. The company reported Q4 2024 sales of SEK 183.92 million, up from SEK 154.66 million the previous year, and net income of SEK 24.13 million. Earnings are forecast to grow significantly at 24% annually, surpassing the Swedish market average of 9.4%. Despite a high debt level, Lime trades at a discount to its estimated fair value and maintains strong profitability with an EBITA margin target of at least 25%.

- Delve into the full analysis future growth report here for a deeper understanding of Lime Technologies.

- Our expertly prepared valuation report Lime Technologies implies its share price may be too high.

Semperit Holding (WBAG:SEM)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Semperit Aktiengesellschaft Holding is a company that develops, produces, and sells rubber products for the medical and industrial sectors globally, with a market cap of €288.44 million.

Operations: The company's revenue segments consist of €34.32 million from Surgical Operations, €380.82 million from Semperit Engineered Applications, and €288.16 million from Semperit Industrial Applications.

Insider Ownership: 10.1%

Earnings Growth Forecast: 34.7% p.a.

Semperit Holding's earnings are expected to grow significantly at 34.7% annually, outpacing the Austrian market average of 9.3%. However, its Return on Equity is forecasted to be low at 5.9% in three years. The company trades at a substantial discount of 44.6% below its estimated fair value, but profit margins have decreased from last year and the dividend yield of 3.57% is not well covered by free cash flows.

- Dive into the specifics of Semperit Holding here with our thorough growth forecast report.

- The valuation report we've compiled suggests that Semperit Holding's current price could be inflated.

Summing It All Up

- Reveal the 222 hidden gems among our Fast Growing European Companies With High Insider Ownership screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:LIME

Lime Technologies

Provides software as a service (SaaS) based customer relationship management (CRM) solutions in the Nordic region.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor