- Canada

- /

- Oil and Gas

- /

- TSX:ERF

Why You Might Be Interested In Enerplus Corporation (TSE:ERF) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Enerplus Corporation (TSE:ERF) is about to go ex-dividend in just 4 days. This means that investors who purchase shares on or after the 29th of January will not receive the dividend, which will be paid on the 14th of February.

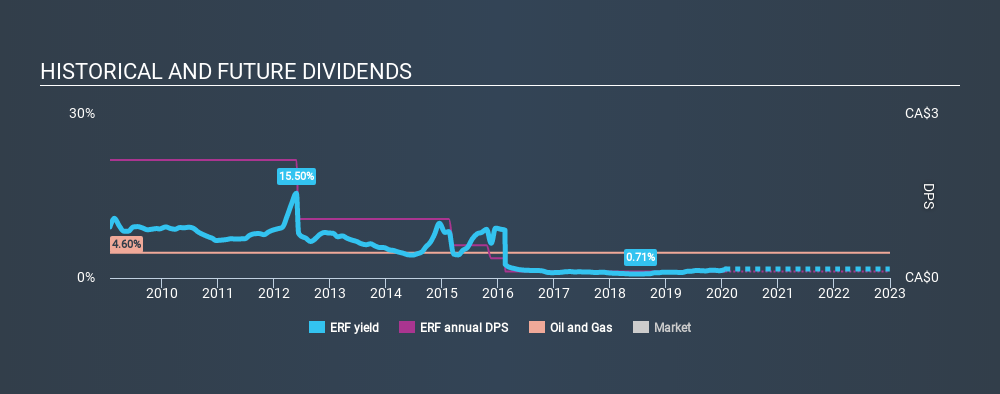

Enerplus's next dividend payment will be CA$0.01 per share, and in the last 12 months, the company paid a total of CA$0.12 per share. Based on the last year's worth of payments, Enerplus stock has a trailing yield of around 1.6% on the current share price of CA$7.3. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Enerplus

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Enerplus paid out just 6.8% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 58% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. It's encouraging to see Enerplus has grown its earnings rapidly, up 49% a year for the past five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Enerplus's dividend payments per share have declined at 25% per year on average over the past ten years, which is uninspiring. It's unusual to see earnings per share increasing at the same time as dividends per share have been in decline. We'd hope it's because the company is reinvesting heavily in its business, but it could also suggest business is lumpy.

Final Takeaway

Should investors buy Enerplus for the upcoming dividend? Earnings per share have grown at a nice rate in recent times and over the last year, Enerplus paid out less than half its earnings and a bit over half its free cash flow. There's a lot to like about Enerplus, and we would prioritise taking a closer look at it.

Curious what other investors think of Enerplus? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:ERF

Enerplus

Explores and develops crude oil and natural gas in the United States.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion