Advertisement

- Sweden

- /

- Trade Distributors

- /

- OM:BERG B

What Is Bergman & Beving's (STO:BERG B) P/E Ratio After Its Share Price Tanked?

Unfortunately for some shareholders, the Bergman & Beving (STO:BERG B) share price has dived 33% in the last thirty days. That drop has capped off a tough year for shareholders, with the share price down 54% in that time.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

View our latest analysis for Bergman & Beving

How Does Bergman & Beving's P/E Ratio Compare To Its Peers?

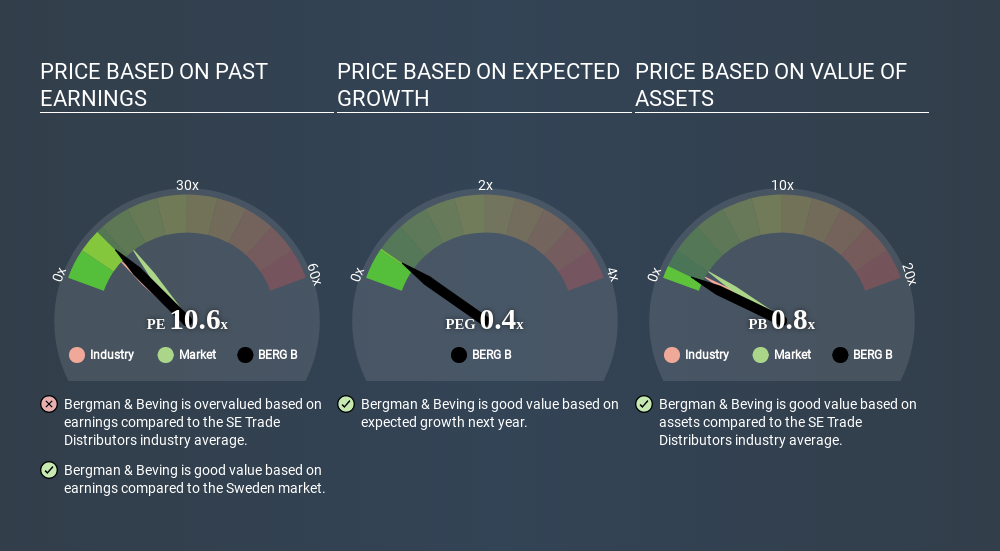

Bergman & Beving has a P/E ratio of 10.64. As you can see below Bergman & Beving has a P/E ratio that is fairly close for the average for the trade distributors industry, which is 10.0.

That indicates that the market expects Bergman & Beving will perform roughly in line with other companies in its industry. So if Bergman & Beving actually outperforms its peers going forward, that should be a positive for the share price. Checking factors such as director buying and selling. could help you form your own view on if that will happen.

How Growth Rates Impact P/E Ratios

If earnings fall then in the future the 'E' will be lower. Therefore, even if you pay a low multiple of earnings now, that multiple will become higher in the future. So while a stock may look cheap based on past earnings, it could be expensive based on future earnings.

Bergman & Beving saw earnings per share decrease by 27% last year. And EPS is down 16% a year, over the last 5 years. This growth rate might warrant a below average P/E ratio.

Remember: P/E Ratios Don't Consider The Balance Sheet

Don't forget that the P/E ratio considers market capitalization. In other words, it does not consider any debt or cash that the company may have on the balance sheet. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

Is Debt Impacting Bergman & Beving's P/E?

Bergman & Beving's net debt equates to 44% of its market capitalization. While it's worth keeping this in mind, it isn't a worry.

The Verdict On Bergman & Beving's P/E Ratio

Bergman & Beving trades on a P/E ratio of 10.6, which is below the SE market average of 14.3. With only modest debt, it's likely the lack of EPS growth at least partially explains the pessimism implied by the P/E ratio. What can be absolutely certain is that the market has become significantly less optimistic about Bergman & Beving over the last month, with the P/E ratio falling from 15.9 back then to 10.6 today. For those who prefer to invest with the flow of momentum, that might be a bad sign, but for a contrarian, it may signal opportunity.

When the market is wrong about a stock, it gives savvy investors an opportunity. If it is underestimating a company, investors can make money by buying and holding the shares until the market corrects itself. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

You might be able to find a better buy than Bergman & Beving. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OM:BERG B

Bergman & Beving

Provides solutions for the manufacturing and construction sectors in Sweden, Norway, Finland, and internationally.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor