Advertisement

- United Kingdom

- /

- Commercial Services

- /

- LSE:RTO

What Did Rentokil Initial's (LON:RTO) CEO Take Home Last Year?

Andy Ransom has been the CEO of Rentokil Initial plc (LON:RTO) since 2013, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also assess whether Rentokil Initial pays its CEO appropriately, considering recent earnings growth and total shareholder returns.

View our latest analysis for Rentokil Initial

How Does Total Compensation For Andy Ransom Compare With Other Companies In The Industry?

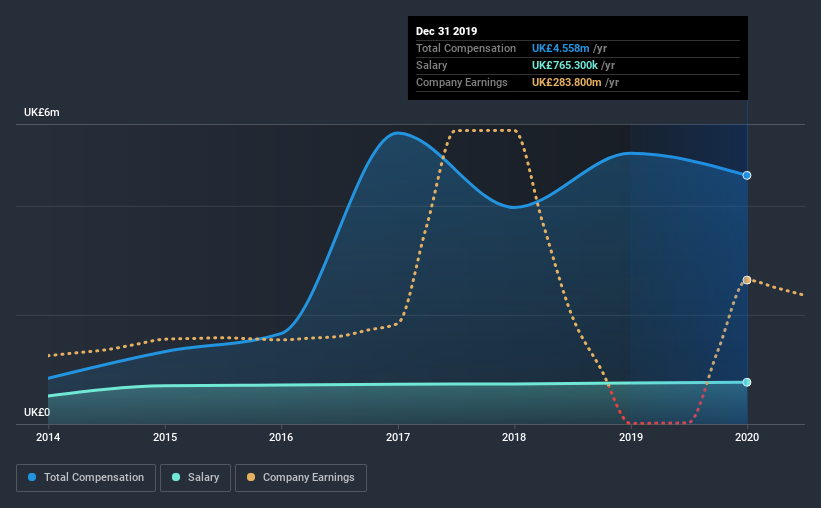

At the time of writing, our data shows that Rentokil Initial plc has a market capitalization of UK£10.0b, and reported total annual CEO compensation of UK£4.6m for the year to December 2019. Notably, that's a decrease of 8.1% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at UK£765k.

On comparing similar companies in the industry with market capitalizations above UK£6.1b, we found that the median total CEO compensation was UK£4.1m. This suggests that Rentokil Initial remunerates its CEO largely in line with the industry average. What's more, Andy Ransom holds UK£8.4m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | UK£765k | UK£750k | 17% |

| Other | UK£3.8m | UK£4.2m | 83% |

| Total Compensation | UK£4.6m | UK£5.0m | 100% |

On an industry level, roughly 56% of total compensation represents salary and 44% is other remuneration. It's interesting to note that Rentokil Initial allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Rentokil Initial plc's Growth

Over the last three years, Rentokil Initial plc has shrunk its earnings per share by 29% per year. Its revenue is up 4.3% over the last year.

Few shareholders would be pleased to read that EPS have declined. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Rentokil Initial plc Been A Good Investment?

We think that the total shareholder return of 87%, over three years, would leave most Rentokil Initial plc shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

As previously discussed, Andy is compensated close to the median for companies of its size, and which belong to the same industry. This doesn't look good when you see that EPS growth over the last three years has been negative. On the flip side, shareholder returns have been strong over the same time, which is certainly a positive sign. We wouldn't say CEO compensation is too high, but shareholders might think performance needs to be improved before paying any more.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We've identified 2 warning signs for Rentokil Initial that investors should be aware of in a dynamic business environment.

Switching gears from Rentokil Initial, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Rentokil Initial, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:RTO

Rentokil Initial

Provides route-based services in North America, Europe, the United Kingdom, Asia, the Middle East, North Africa, Turkey, and Pacific.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5297.0% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3076.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative