Advertisement

- Hong Kong

- /

- Communications

- /

- SEHK:1720

We Wouldn't Rely On Putian Communication Group's (HKG:1720) Statutory Earnings As A Guide

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. Today we'll focus on whether this year's statutory profits are a good guide to understanding Putian Communication Group (HKG:1720).

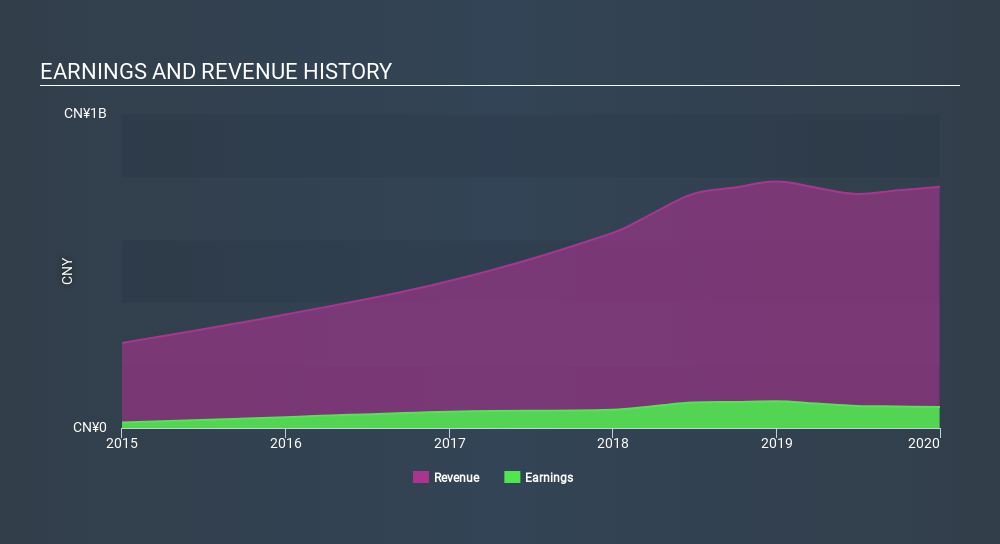

It's good to see that over the last twelve months Putian Communication Group made a profit of CN¥66.8m on revenue of CN¥768.3m. Happily, it has grown both its profit and revenue over the last three years (but not in the last year), as you can see in the chart below.

View our latest analysis for Putian Communication Group

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. So today we'll look at what Putian Communication Group's cashflow tells us about the quality of its earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Putian Communication Group.

Zooming In On Putian Communication Group's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Putian Communication Group has an accrual ratio of 0.34 for the year to December 2019. Unfortunately, that means its free cash flow was a lot less than its statutory profit, which makes us doubt the utility of profit as a guide. In the last twelve months it actually had negative free cash flow, with an outflow of CN¥95m despite its profit of CN¥66.8m, mentioned above. We also note that Putian Communication Group's free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of CN¥95m.

Our Take On Putian Communication Group's Profit Performance

As we have made quite clear, we're a bit worried that Putian Communication Group didn't back up the last year's profit with free cashflow. For this reason, we think that Putian Communication Group's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. Sadly, its EPS was down over the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Case in point: We've spotted 3 warning signs for Putian Communication Group you should be mindful of and 2 of them can't be ignored.

This note has only looked at a single factor that sheds light on the nature of Putian Communication Group's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About SEHK:1720

Putian Communication Group

An investment holding company, manufactures and produces data and communications cables and structured cabling system product under the Hanphy brand name in the People's Republic of China, Hong Kong, and internationally.

Proven track record with slight risk.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.551.6% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.4% overvalued

26 followersusers have followed this narrative

3 commentsusers have commented on this narrative

26 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8823.8% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

SO

sorkdhkddlek on Intuitive Machines ·

Strategic Expansion Meets Valuation Reality at $23

Fair Value:US$2311.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SO

sorkdhkddlek on American Electric Power Company ·

AEP: Capturing the Scarcity Value of the American Power Grid

Fair Value:US$11319.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PA

Pad on Williamson Tea Kenya ·

Long Term Hold

Fair Value:KSh17521.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.231.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1385 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0

SI

Simply Wall St User on Black Diamond Group ·

I'm guessing but is ATCO the only other Canadian competitor? And who in the US?

0

|0