Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:TFPM

TSX Value Picks Including Allied Gold And 2 More Stocks Trading Below Estimated Worth

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates an environment of improving labour productivity and contained unit labour costs, investors are keeping a close eye on potential value opportunities. With corporate earnings growth showing resilience and inflation remaining relatively stable, identifying undervalued stocks becomes crucial for those looking to capitalize on these favorable economic conditions. In this context, Allied Gold and two other stocks stand out as promising candidates trading below their estimated worth.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| West Fraser Timber (TSX:WFG) | CA$99.54 | CA$173.99 | 42.8% |

| Vitalhub (TSX:VHI) | CA$13.51 | CA$24.09 | 43.9% |

| TerraVest Industries (TSX:TVK) | CA$165.41 | CA$309.20 | 46.5% |

| Savaria (TSX:SIS) | CA$21.22 | CA$42.21 | 49.7% |

| K92 Mining (TSX:KNT) | CA$14.84 | CA$28.18 | 47.3% |

| Groupe Dynamite (TSX:GRGD) | CA$39.64 | CA$70.89 | 44.1% |

| goeasy (TSX:GSY) | CA$210.01 | CA$382.54 | 45.1% |

| Blackline Safety (TSX:BLN) | CA$6.22 | CA$10.16 | 38.8% |

| Avino Silver & Gold Mines (TSX:ASM) | CA$5.38 | CA$9.87 | 45.5% |

| Allied Gold (TSX:AAUC) | CA$16.39 | CA$28.92 | 43.3% |

Let's take a closer look at a couple of our picks from the screened companies.

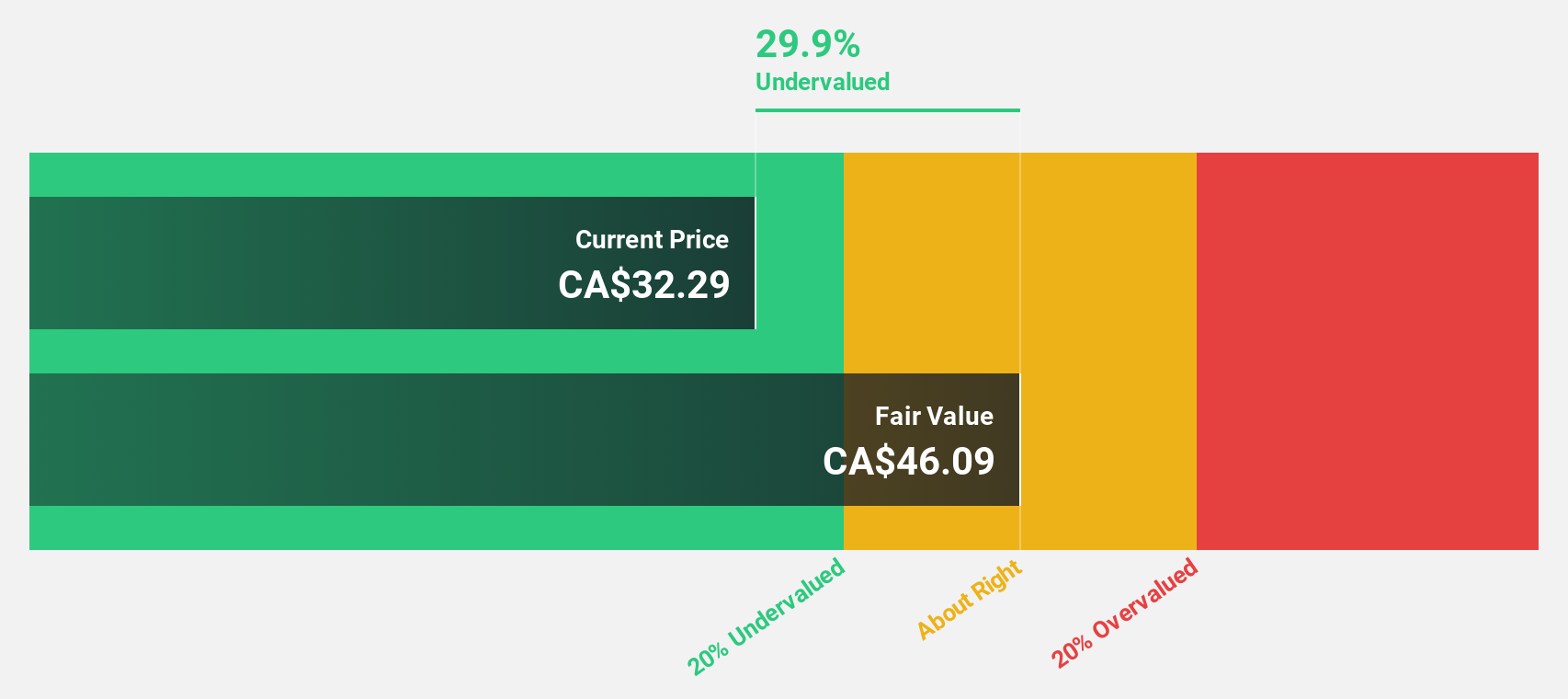

Allied Gold (TSX:AAUC)

Overview: Allied Gold Corporation, along with its subsidiaries, is engaged in the exploration and production of mineral deposits in Africa and has a market cap of CA$1.84 billion.

Operations: The company's revenue segments include the Agbaou Mine generating $213.19 million, the Bonikro Mine contributing $247.48 million, and the Sadiola Mine accounting for $497.42 million.

Estimated Discount To Fair Value: 43.3%

Allied Gold appears undervalued, trading at CA$16.39, significantly below its estimated fair value of CA$28.92. Despite a net loss of US$25.41 million in Q2 2025, the company reported sales growth to US$251.98 million from US$195.61 million a year ago and forecasts robust annual revenue growth of 22.4%. While shareholders faced substantial dilution recently, Allied Gold is expected to become profitable within three years, outpacing average market growth rates in Canada.

- Our comprehensive growth report raises the possibility that Allied Gold is poised for substantial financial growth.

- Get an in-depth perspective on Allied Gold's balance sheet by reading our health report here.

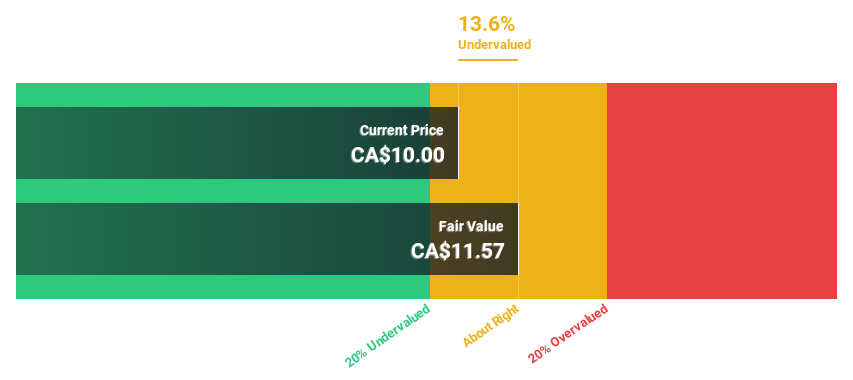

Cineplex (TSX:CGX)

Overview: Cineplex Inc., along with its subsidiaries, operates as an entertainment and media company in Canada and internationally, with a market cap of CA$655.34 million.

Operations: The company's revenue is derived from three main segments: Media (CA$141.23 million), Location-Based Entertainment (CA$132.24 million), and Film Entertainment and Content (CA$1.03 billion).

Estimated Discount To Fair Value: 11.8%

Cineplex's recent earnings report shows improved financials with Q2 2025 revenue rising to C$361.82 million from C$277.34 million a year ago, while net loss narrowed significantly. Trading at C$10.73, Cineplex is undervalued compared to its estimated fair value of C$12.17 and offers good relative value against peers. Revenue growth is forecasted at 7.3% annually, outpacing the Canadian market average of 4%, with profitability expected within three years despite negative equity concerns.

- Our expertly prepared growth report on Cineplex implies its future financial outlook may be stronger than recent results.

- Click here and access our complete balance sheet health report to understand the dynamics of Cineplex.

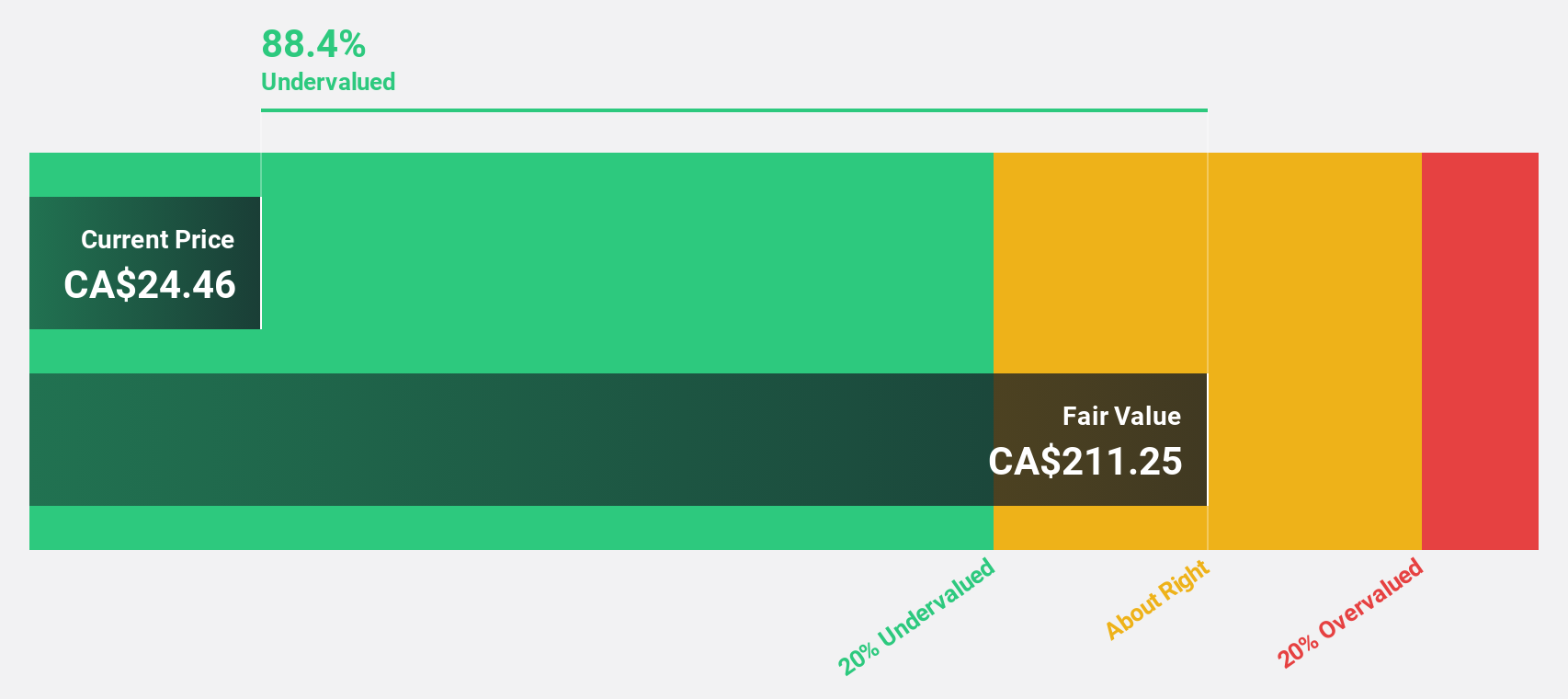

Triple Flag Precious Metals (TSX:TFPM)

Overview: Triple Flag Precious Metals Corp. is a precious metals streaming and royalty company that acquires and manages mineral interests across various countries, with a market cap of CA$7.65 billion.

Operations: The company's revenue primarily comes from its Metals & Mining segment, specifically Gold & Other Precious Metals, totaling $324.21 million.

Estimated Discount To Fair Value: 23.9%

Triple Flag Precious Metals is trading at CA$36.84, significantly below its fair value of CA$48.38, highlighting its undervaluation based on cash flows. The company reported a strong turnaround with Q2 2025 earnings of US$55.74 million compared to a loss last year and expects annual earnings growth of over 20%, surpassing the Canadian market's average growth rate. Despite recent insider selling, the company's profitability and revenue growth projections remain robust.

- Our growth report here indicates Triple Flag Precious Metals may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Triple Flag Precious Metals.

Summing It All Up

- Explore the 24 names from our Undervalued TSX Stocks Based On Cash Flows screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Triple Flag Precious Metals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TFPM

Triple Flag Precious Metals

A precious metals streaming and royalty company, engages in acquiring and managing precious metals, streams, royalties, and other mineral interests in Australia, Canada, Colombia, Cote d’Ivoire, Honduras, Mexico, Mongolia, Peru, South Africa, and the United States.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.6% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|14.9% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.2% undervalued

AG

Community Contributor