- United States

- /

- Trade Distributors

- /

- NasdaqGS:FAST

Should You Be Tempted To Sell Fastenal Company (NASDAQ:FAST) Because Of Its P/E Ratio?

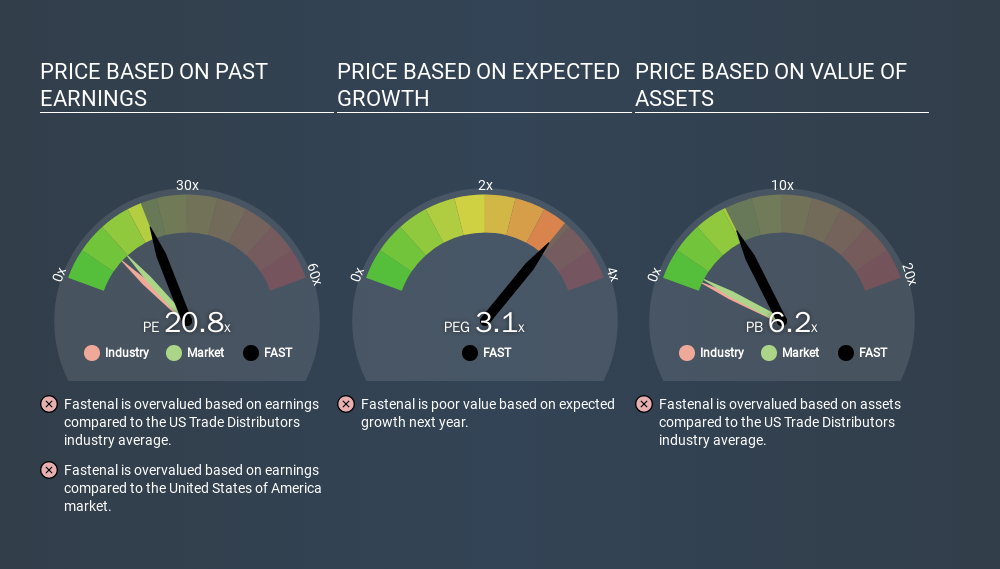

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll look at Fastenal Company's (NASDAQ:FAST) P/E ratio and reflect on what it tells us about the company's share price. Based on the last twelve months, Fastenal's P/E ratio is 20.83. In other words, at today's prices, investors are paying $20.83 for every $1 in prior year profit.

See our latest analysis for Fastenal

How Do You Calculate Fastenal's P/E Ratio?

The formula for P/E is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Fastenal:

P/E of 20.83 = $28.740 ÷ $1.380 (Based on the trailing twelve months to December 2019.)

(Note: the above calculation results may not be precise due to rounding.)

Is A High P/E Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each $1 of company earnings. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Does Fastenal's P/E Ratio Compare To Its Peers?

We can get an indication of market expectations by looking at the P/E ratio. The image below shows that Fastenal has a higher P/E than the average (9.7) P/E for companies in the trade distributors industry.

That means that the market expects Fastenal will outperform other companies in its industry. Clearly the market expects growth, but it isn't guaranteed. So investors should delve deeper. I like to check if company insiders have been buying or selling.

How Growth Rates Impact P/E Ratios

Probably the most important factor in determining what P/E a company trades on is the earnings growth. Earnings growth means that in the future the 'E' will be higher. And in that case, the P/E ratio itself will drop rather quickly. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Fastenal's earnings per share grew by 5.3% in the last twelve months. And earnings per share have improved by 11% annually, over the last five years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. Thus, the metric does not reflect cash or debt held by the company. In theory, a company can lower its future P/E ratio by using cash or debt to invest in growth.

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

How Does Fastenal's Debt Impact Its P/E Ratio?

Net debt totals just 1.0% of Fastenal's market cap. The market might award it a higher P/E ratio if it had net cash, but its unlikely this low level of net borrowing is having a big impact on the P/E multiple.

The Verdict On Fastenal's P/E Ratio

Fastenal trades on a P/E ratio of 20.8, which is above its market average of 11.8. Given the debt is only modest, and earnings are already moving in the right direction, it's not surprising that the market expects continued improvement.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course you might be able to find a better stock than Fastenal. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:FAST

Fastenal

Engages in the wholesale distribution of industrial and construction supplies in the United States, Canada, Mexico, and internationally.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)