Advertisement

- France

- /

- Professional Services

- /

- ENXTPA:BVI

Should We Worry About Bureau Veritas SA's (EPA:BVI) P/E Ratio?

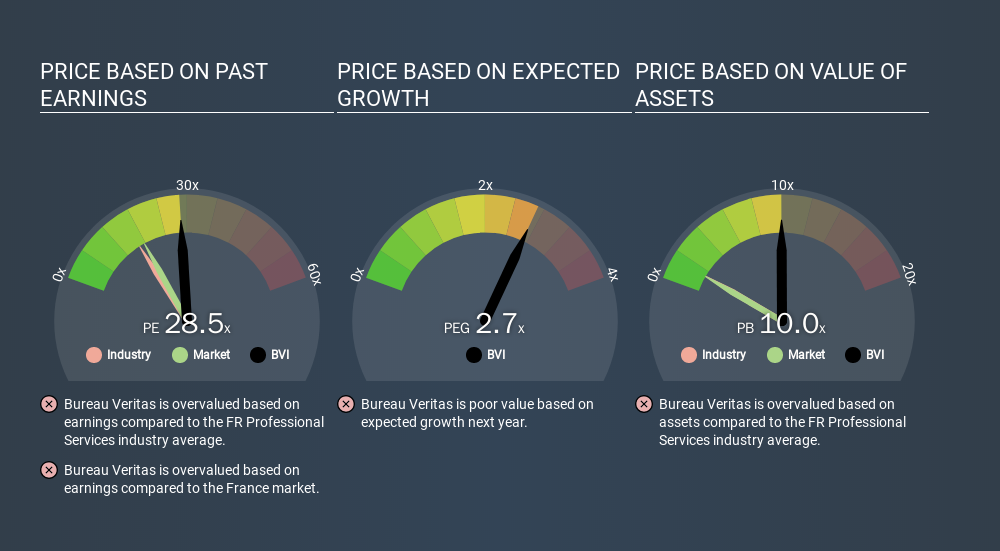

Today, we'll introduce the concept of the P/E ratio for those who are learning about investing. We'll look at Bureau Veritas SA's (EPA:BVI) P/E ratio and reflect on what it tells us about the company's share price. Looking at earnings over the last twelve months, Bureau Veritas has a P/E ratio of 28.51. That means that at current prices, buyers pay €28.51 for every €1 in trailing yearly profits.

View our latest analysis for Bureau Veritas

How Do You Calculate Bureau Veritas's P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Bureau Veritas:

P/E of 28.51 = €23.11 ÷ €0.81 (Based on the trailing twelve months to June 2019.)

Is A High Price-to-Earnings Ratio Good?

The higher the P/E ratio, the higher the price tag of a business, relative to its trailing earnings. All else being equal, it's better to pay a low price -- but as Warren Buffett said, 'It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

How Does Bureau Veritas's P/E Ratio Compare To Its Peers?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. The image below shows that Bureau Veritas has a higher P/E than the average (16.2) P/E for companies in the professional services industry.

That means that the market expects Bureau Veritas will outperform other companies in its industry. Clearly the market expects growth, but it isn't guaranteed. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. Earnings growth means that in the future the 'E' will be higher. And in that case, the P/E ratio itself will drop rather quickly. And as that P/E ratio drops, the company will look cheap, unless its share price increases.

Bureau Veritas increased earnings per share by 7.0% last year. And it has bolstered its earnings per share by 1.5% per year over the last five years.

Don't Forget: The P/E Does Not Account For Debt or Bank Deposits

It's important to note that the P/E ratio considers the market capitalization, not the enterprise value. That means it doesn't take debt or cash into account. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Spending on growth might be good or bad a few years later, but the point is that the P/E ratio does not account for the option (or lack thereof).

How Does Bureau Veritas's Debt Impact Its P/E Ratio?

Bureau Veritas has net debt worth 20% of its market capitalization. That's enough debt to impact the P/E ratio a little; so keep it in mind if you're comparing it to companies without debt.

The Verdict On Bureau Veritas's P/E Ratio

Bureau Veritas has a P/E of 28.5. That's higher than the average in its market, which is 17.8. With debt at prudent levels and improving earnings, it's fair to say the market expects steady progress in the future.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visual report on analyst forecasts could hold the key to an excellent investment decision.

Of course you might be able to find a better stock than Bureau Veritas. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ENXTPA:BVI

Bureau Veritas

Provides laboratory testing, inspection, and certification services.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Optimi Health ·

OPTH: A licensed manufacturer already selling MDMA while peers still wait on trials

Fair Value:US$1259.6% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

36 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.524.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.722.1% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on STLLR Gold ·

STLLR Gold, Eric Sprott + Agnico Backed: Massive Canadian Gold Developer at Junior Prices

Fair Value:CA$102.2298.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

PE

peter_4mgsy on Rhythm Pharmaceuticals ·

High-Growth Emerging Commercial Stage Biotech

Fair Value:US$13413.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on FreightCar America ·

ALL ABOARD THE VALUE TRAIN: WHY $RAIL MIGHT BE HEADED NORTH - FREIGHTCAR AMERICA - Long term price target of $25

Fair Value:US$2568.4% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28022.3% undervalued

288 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9120.5% overvalued

153 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0941.5% undervalued

173 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

IA

ian_oii7z on Woodside Energy Group ·

Hey James! Thank you but I am not sure if I am reading this correctly as your analysis opens with "At A$36.602 per share, Woodside Energy Group (ASX: WDS) appears reasonably valued based on its existing operations and near-term production growth." I would like to say that the last time that WDS was above $36.00 per share was in October 2023, so I am a little confused by your statement w.r.t. current prices etc . Can you please explain?

1

|0

R2

R2R on Fonterra Shareholders Fund ·

SIMPLY WALL STREET please delete this Ai slop nonsense article.

0

|0