Advertisement

- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

Results: UltraTech Cement Limited Beat Earnings Expectations And Analysts Now Have New Forecasts

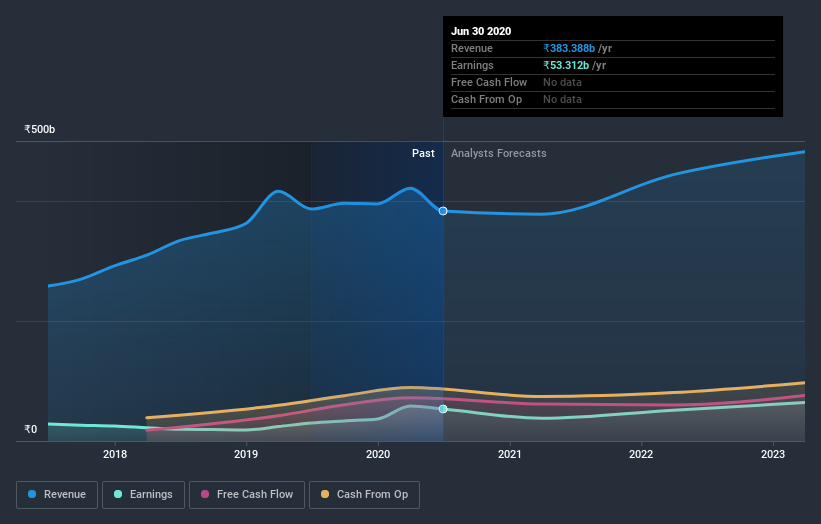

As you might know, UltraTech Cement Limited (NSE:ULTRACEMCO) just kicked off its latest first-quarter results with some very strong numbers. It was overall a positive result, with revenues beating expectations by 4.9% to hit ₹76b. UltraTech Cement also reported a statutory profit of ₹27.64, which was an impressive 57% above what the analysts had forecast. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on UltraTech Cement after the latest results.

Check out our latest analysis for UltraTech Cement

Taking into account the latest results, UltraTech Cement's 26 analysts currently expect revenues in 2021 to be ₹378.1b, approximately in line with the last 12 months. Statutory earnings per share are expected to tumble 32% to ₹126 in the same period. In the lead-up to this report, the analysts had been modelling revenues of ₹373.3b and earnings per share (EPS) of ₹100 in 2021. There was no real change to the revenue estimates, but the analysts do seem more bullish on earnings, given the sizeable expansion in earnings per share expectations following these results.

The analysts have been lifting their price targets on the back of the earnings upgrade, with the consensus price target rising 8.4% to ₹4,498. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on UltraTech Cement, with the most bullish analyst valuing it at ₹5,504 and the most bearish at ₹3,465 per share. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the UltraTech Cement's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast revenue decline of 1.4%, a significant reduction from annual growth of 13% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 9.6% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - UltraTech Cement is expected to lag the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards UltraTech Cement following these results. On the plus side, there were no major changes to revenue estimates; although forecasts imply revenues will perform worse than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for UltraTech Cement going out to 2023, and you can see them free on our platform here.

Even so, be aware that UltraTech Cement is showing 2 warning signs in our investment analysis , you should know about...

If you’re looking to trade UltraTech Cement, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:ULTRACEMCO

UltraTech Cement

Primarily engages in the manufacture and sale of clinker, cement, and related products in India.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor