Advertisement

Results: CapitaLand Mall Trust Exceeded Expectations And The Consensus Has Updated Its Estimates

CapitaLand Mall Trust (SGX:C38U) just released its latest quarterly results and things are looking bullish. CapitaLand Mall Trust delivered a significant beat to revenue and earnings per share (EPS) expectations, with sales hitting S$114m, some 18% above indicated. Statutory EPS were S$0.19, an impressive 50% ahead of forecasts. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for CapitaLand Mall Trust

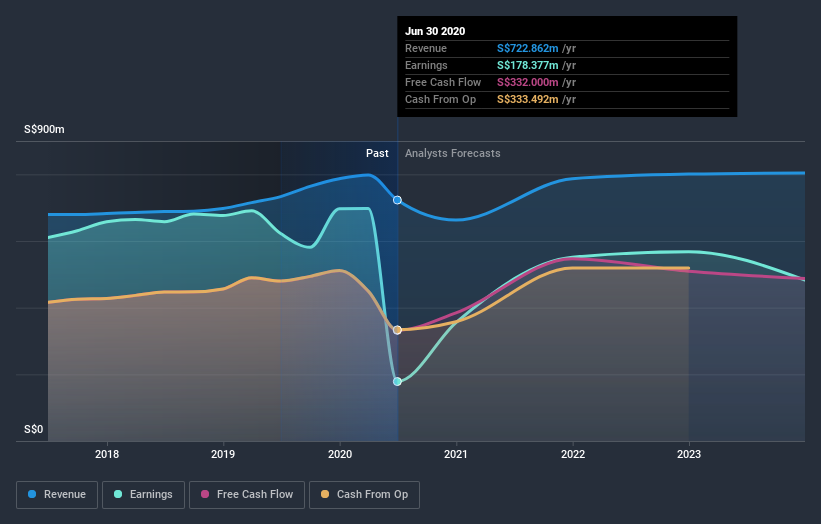

After the latest results, the consensus from CapitaLand Mall Trust's 14 analysts is for revenues of S$662.8m in 2020, which would reflect a chunky 8.3% decline in sales compared to the last year of performance. Per-share earnings are expected to soar 70% to S$0.082. In the lead-up to this report, the analysts had been modelling revenues of S$668.0m and earnings per share (EPS) of S$0.087 in 2020. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target was broadly unchanged at S$2.32, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic CapitaLand Mall Trust analyst has a price target of S$2.90 per share, while the most pessimistic values it at S$1.75. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that sales are expected to reverse, with the forecast 8.3% revenue decline a notable change from historical growth of 2.9% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.3% next year. It's pretty clear that CapitaLand Mall Trust's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that CapitaLand Mall Trust's revenues are expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for CapitaLand Mall Trust going out to 2023, and you can see them free on our platform here..

However, before you get too enthused, we've discovered 4 warning signs for CapitaLand Mall Trust (1 is a bit unpleasant!) that you should be aware of.

If you decide to trade CapitaLand Mall Trust, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SGX:C38U

CapitaLand Integrated Commercial Trust

CapitaLand Integrated Commercial Trust (CICT or the Trust) is the first and largest real estate investment trust (REIT) listed on Singapore Exchange Securities Trading Limited (SGX-ST).

Average dividend payer and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

9 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

6 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

69 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative