Advertisement

- United States

- /

- Commercial Services

- /

- OTCPK:WHLM

Our Take On Wilhelmina International, Inc.'s (NASDAQ:WHLM) CEO Salary

Bill Wackermann became the CEO of Wilhelmina International, Inc. (NASDAQ:WHLM) in 2016. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. Next, we'll consider growth that the business demonstrates. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. The aim of all this is to consider the appropriateness of CEO pay levels.

See our latest analysis for Wilhelmina International

How Does Bill Wackermann's Compensation Compare With Similar Sized Companies?

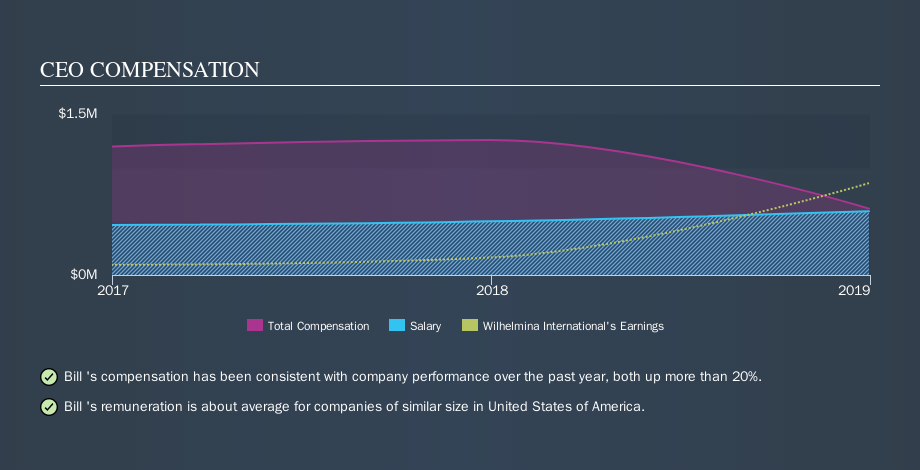

Our data indicates that Wilhelmina International, Inc. is worth US$27m, and total annual CEO compensation was reported as US$618k for the year to December 2018. Notably, the salary of US$593k is the vast majority of the CEO compensation. We looked at a group of companies with market capitalizations under US$200m, and the median CEO total compensation was US$496k.

So Bill Wackermann is paid around the average of the companies we looked at. This doesn't tell us a whole lot on its own, but looking at the performance of the actual business will give us useful context. We don't have analyst forecasts, but you might want to assess this data-rich visualization of earnings, revenue and cash flow.

You can see a visual representation of the CEO compensation at Wilhelmina International, below.

Is Wilhelmina International, Inc. Growing?

Over the last three years Wilhelmina International, Inc. has grown its earnings per share (EPS) by an average of 18% per year (using a line of best fit). Its revenue is up 1.9% over last year.

This demonstrates that the company has been improving recently. A good result. It's nice to see a little revenue growth, as this is consistent with healthy business conditions.

Has Wilhelmina International, Inc. Been A Good Investment?

Given the total loss of 36% over three years, many shareholders in Wilhelmina International, Inc. are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

Remuneration for Bill Wackermann is close enough to the median pay for a CEO of a similar sized company .

We think that the EPS growth is very pleasing, but it's disappointing to see negative shareholder returns over three years. We'd be surprised if shareholders want to see a pay rise for the CEO, but we'd stop short of calling their pay too generous. CEO compensation is one thing, but it is also interesting to check if the CEO is buying or selling Wilhelmina International (free visualization of insider trades).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OTCPK:WHLM

Wilhelmina International

Primarily engages in the fashion model management business.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.0% undervalued

28 followersusers have followed this narrative

5 commentsusers have commented on this narrative

9 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.4% undervalued

26 followersusers have followed this narrative

3 commentsusers have commented on this narrative

19 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8151.3% undervalued

49 followersusers have followed this narrative

4 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.225.4% undervalued

49 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on Fiverr International ·

Fiverr International will transform the freelance industry with AI-powered growth

Fair Value:US$43.3352.3% undervalued

82 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YI

yiannisz on Janus Henderson Group ·

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Fair Value:US$41.459.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

120 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8683.7% undervalued

78 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3930.1% undervalued

968 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative