Advertisement

- United States

- /

- Auto Components

- /

- NasdaqGM:SYPR

Is Sypris Solutions (NASDAQ:SYPR) Weighed On By Its Debt Load?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Sypris Solutions, Inc. (NASDAQ:SYPR) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Sypris Solutions

How Much Debt Does Sypris Solutions Carry?

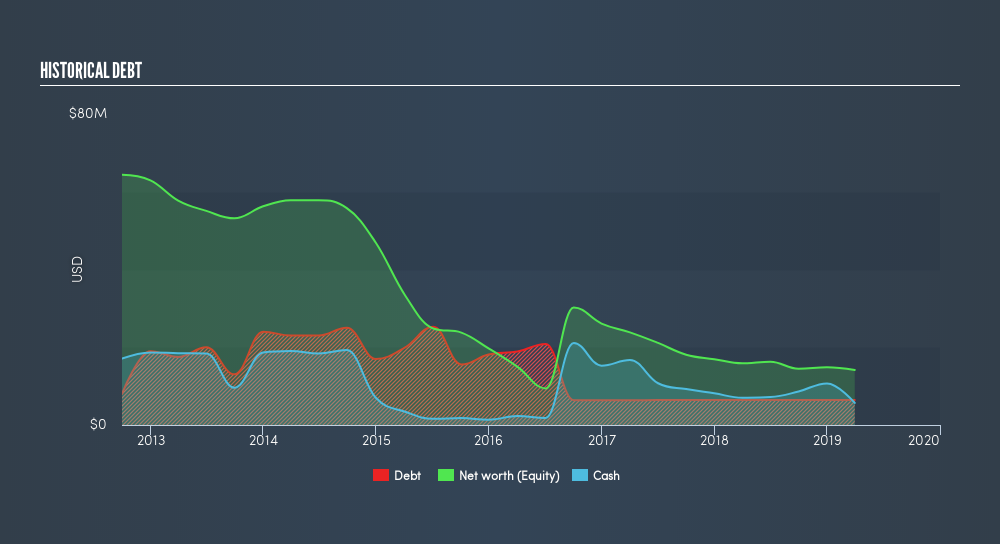

The chart below, which you can click on for greater detail, shows that Sypris Solutions had US$9.97m in debt in March 2019; about the same as the year before. On the flip side, it has US$5.69m in cash leading to net debt of about US$4.29m.

How Healthy Is Sypris Solutions's Balance Sheet?

We can see from the most recent balance sheet that Sypris Solutions had liabilities of US$28.0m falling due within a year, and liabilities of US$23.5m due beyond that. Offsetting these obligations, it had cash of US$5.69m as well as receivables valued at US$9.67m due within 12 months. So it has liabilities totalling US$36.2m more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$20.2m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt At the end of the day, Sypris Solutions would probably need a major re-capitalization if its creditors were to demand repayment. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Sypris Solutions's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Sypris Solutions reported revenue of US$88m, which is a gain of 4.2%. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

Caveat Emptor

Importantly, Sypris Solutions had negative earnings before interest and tax (EBIT), over the last year. Indeed, it lost a very considerable US$4.2m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. Not least because it burned through US$3.9m in negative free cash flow over the last year. That means it's on the risky side of things. For riskier companies like Sypris Solutions I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGM:SYPR

Sypris Solutions

Provides truck components, oil and gas pipeline components, and aerospace and defense electronics in North America.

Adequate balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

JH

JH7 on LVMH Moët Hennessy - Louis Vuitton Société Européenne ·

The Luxury Titan Mispriced by a Short‑Sighted Market

Fair Value:€68032.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Woodside Energy Group ·

Does WDS Have More in the Tank?

Fair Value:AU$36.611.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Treasury Wine Estates ·

Is TWE Aging Well?

Fair Value:AU$7.0733.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

80 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

183 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative