Advertisement

Today we'll evaluate SKAKO A/S (CPH:SKAKO) to determine whether it could have potential as an investment idea. In particular, we'll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

First up, we'll look at what ROCE is and how we calculate it. Next, we'll compare it to others in its industry. And finally, we'll look at how its current liabilities are impacting its ROCE.

Return On Capital Employed (ROCE): What is it?

ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. In general, businesses with a higher ROCE are usually better quality. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.

So, How Do We Calculate ROCE?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for SKAKO:

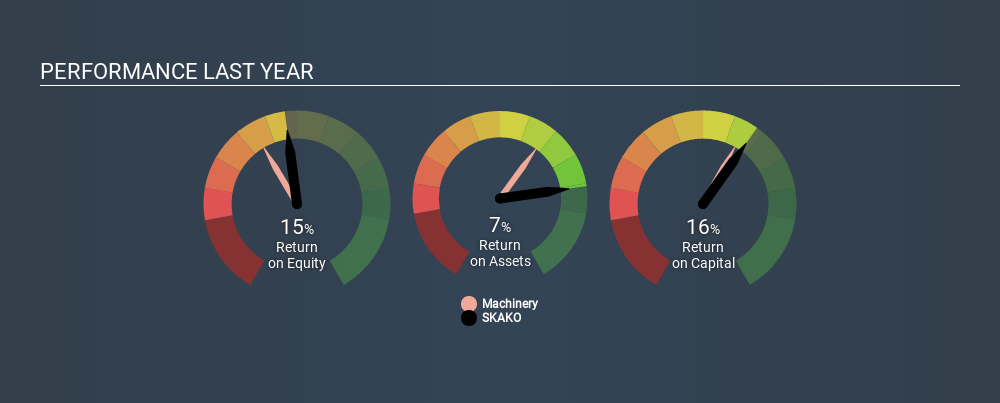

0.16 = ø20m ÷ (ø258m - ø134m) (Based on the trailing twelve months to September 2019.)

Therefore, SKAKO has an ROCE of 16%.

See our latest analysis for SKAKO

Is SKAKO's ROCE Good?

ROCE can be useful when making comparisons, such as between similar companies. In our analysis, SKAKO's ROCE is meaningfully higher than the 11% average in the Machinery industry. We would consider this a positive, as it suggests it is using capital more effectively than other similar companies. Regardless of where SKAKO sits next to its industry, its ROCE in absolute terms appears satisfactory, and this company could be worth a closer look.

You can see in the image below how SKAKO's ROCE compares to its industry. Click to see more on past growth.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. ROCE is, after all, simply a snap shot of a single year. You can check if SKAKO has cyclical profits by looking at this free graph of past earnings, revenue and cash flow.

What Are Current Liabilities, And How Do They Affect SKAKO's ROCE?

Short term (or current) liabilities, are things like supplier invoices, overdrafts, or tax bills that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

SKAKO has current liabilities of ø134m and total assets of ø258m. As a result, its current liabilities are equal to approximately 52% of its total assets. SKAKO's current liabilities are fairly high, which increases its ROCE significantly.

What We Can Learn From SKAKO's ROCE

The ROCE would not look as appealing if the company had fewer current liabilities. SKAKO shapes up well under this analysis, but it is far from the only business delivering excellent numbers . You might also want to check this free collection of companies delivering excellent earnings growth.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About CPSE:3NOV25

Investeringsselskabet af 3. November 2025

Investeringsselskabet af 3. november 2025 A/S designs, develops, and sells vibratory feeding, conveying, and screening equipment in Europe, the United States of America, Africa, and internationally.

Medium-low risk with excellent balance sheet.

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1939.7% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6527.1% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.6% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

PI

PittTheYounger on Erste Group Bank ·

An Austrian industry leader with attractive CEE exposure

Fair Value:€149.2321.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

EU

European_Hidden_Gem_Stocks on Yü Group ·

Massive Cash Pile. Accelerating Growth. Is the Market Mispricing Yü Group?

Fair Value:UK£44.4263.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PR

PrashhD on MRF ·

MRF to See 22.9% Future PE Growth in Five Years

Fair Value:₹117.53k12.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5451.0% undervalued

63 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3462.5% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative