Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:QXO

Is SilverSun Technologies, Inc.'s (NASDAQ:SSNT) CEO Paid At A Competitive Rate?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Mark Meller became the CEO of SilverSun Technologies, Inc. (NASDAQ:SSNT) in 2004. First, this article will compare CEO compensation with compensation at similar sized companies. Then we'll look at a snap shot of the business growth. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for SilverSun Technologies

How Does Mark Meller's Compensation Compare With Similar Sized Companies?

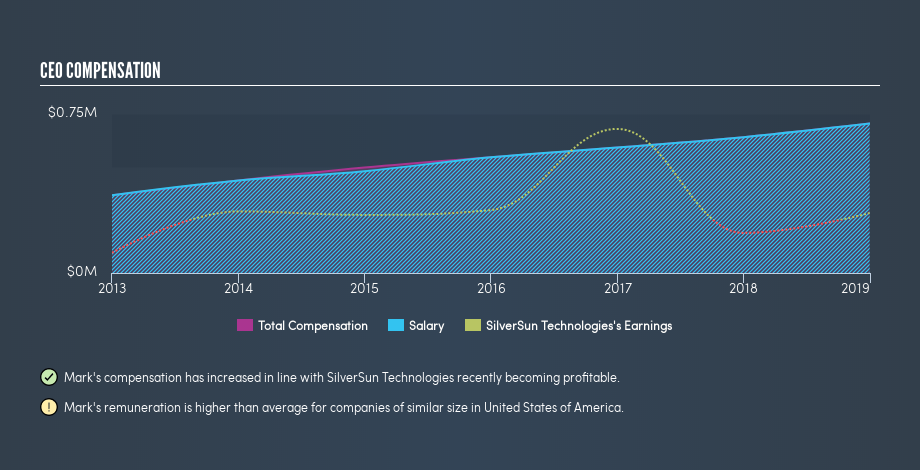

Our data indicates that SilverSun Technologies, Inc. is worth US$13m, and total annual CEO compensation is US$705k. (This figure is for the year to December 2018). Notably, the salary of US$705k is the vast majority of the CEO compensation. We looked at a group of companies with market capitalizations under US$200m, and the median CEO total compensation was US$463k.

As you can see, Mark Meller is paid more than the median CEO pay at companies of a similar size, in the same market. However, this does not necessarily mean SilverSun Technologies, Inc. is paying too much. A closer look at the performance of the underlying business will give us a better idea about whether the pay is particularly generous.

You can see a visual representation of the CEO compensation at SilverSun Technologies, below.

Is SilverSun Technologies, Inc. Growing?

On average over the last three years, SilverSun Technologies, Inc. has shrunk earnings per share by 63% each year (measured with a line of best fit). In the last year, its revenue is up 17%.

Unfortunately, earnings per share have trended lower over the last three years. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that earnings per share has gone backwards over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO.

Has SilverSun Technologies, Inc. Been A Good Investment?

Most shareholders would probably be pleased with SilverSun Technologies, Inc. for providing a total return of 105% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

We compared total CEO remuneration at SilverSun Technologies, Inc. with the amount paid at companies with a similar market capitalization. We found that it pays well over the median amount paid in the benchmark group.

Neither earnings per share nor revenue have been growing sufficiently fast to impress us, over the last three years.On the other hand, returns have been good, so the company is doing something right. Considering this, shareholders are probably not too worried about the CEO compensation. So you may want to check if insiders are buying SilverSun Technologies shares with their own money (free access).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:QXO

QXO

Distributes roofing, waterproofing and complementary building products in the United States and Canada.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

152 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

33 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Recently Updated Narratives

BL

Blaxland on Lincoln Minerals ·

Asymmetric potential

Fair Value:AU$0.002250.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Workday ·

Workday's Backlog Just Grew Faster Than Its Revenue.The Market Shrugged.

Fair Value:US$550.167.3% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2036.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

271 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

135 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

163 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0