Advertisement

Nassef Onssy Sawiris became the CEO of OCI N.V. (AMS:OCI) in 2013. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. After that, we will consider the growth in the business. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for OCI

How Does Nassef Onssy Sawiris's Compensation Compare With Similar Sized Companies?

According to our data, OCI N.V. has a market capitalization of €2.3b, and paid its CEO total annual compensation worth US$5.8m over the year to December 2019. That's actually a decrease on the year before. We think total compensation is more important but we note that the CEO salary is lower, at US$2.0m. Importantly, there may be performance hurdles relating to the non-salary component of the total compensation. We examined companies with market caps from US$2.0b to US$6.4b, and discovered that the median CEO total compensation of that group was US$2.6m.

Now let's take a look at the pay mix on an industry and company level to gain a better understanding of where OCI stands. Speaking on an industry level, we can see that nearly 34% of total compensation represents salary, while the remainder of 66% is other remuneration. OCI does not set aside a larger portion of remuneration in the form of salary, maintaining the same rate as the wider market.

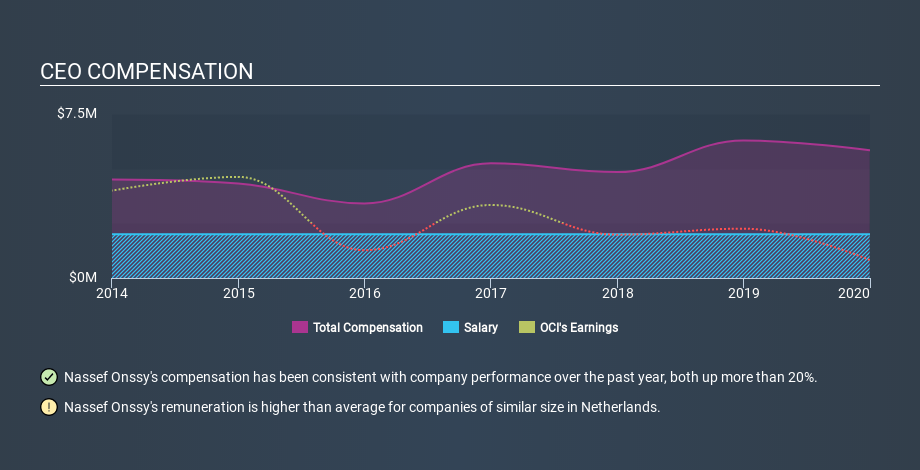

As you can see, Nassef Onssy Sawiris is paid more than the median CEO pay at companies of a similar size, in the same market. However, this does not necessarily mean OCI N.V. is paying too much. We can get a better idea of how generous the pay is by looking at the performance of the underlying business. The graphic below shows how CEO compensation at OCI has changed from year to year.

Is OCI N.V. Growing?

On average over the last three years, OCI N.V. has shrunk earnings per share by 86% each year (measured with a line of best fit). Its revenue is down 6.8% over last year.

Few shareholders would be pleased to read that earnings per share are lower over three years. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. You might want to check this free visual report on analyst forecasts for future earnings.

Has OCI N.V. Been A Good Investment?

Since shareholders would have lost about 41% over three years, some OCI N.V. shareholders would surely be feeling negative emotions. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

We compared the total CEO remuneration paid by OCI N.V., and compared it to remuneration at a group of similar sized companies. Our data suggests that it pays above the median CEO pay within that group.

We think many shareholders would be underwhelmed with the business growth over the last three years. Just as bad, share price gains for investors have failed to materialize, over the same period. Some might well form the view that the CEO is paid too generously! On another note, we've spotted 1 warning sign for OCI that investors should look into moving forward.

Important note: OCI may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ENXTAM:OCI

OCI

Produces and distributes hydrogen-based and natural gas-based products to agricultural, transportation, and industrial customers.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Enterprise, AI & Cloud Growth Ahead, Waiting For the Right Price 💸

Fair Value US$204.74|6.7% overvalued

FR

Community Contributor

Good foundation, but now it's all about the next steps

Fair Value US$147.87|23.9% undervalued

TO

Community Contributor

XTB's Path to 100–120 PLN by 2028 Amid Market Volatility

Fair Value zł100.96|33.3% undervalued

DZ

Community Contributor