Advertisement

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Indústrias Romi S.A. (BVMF:ROMI3) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Indústrias Romi

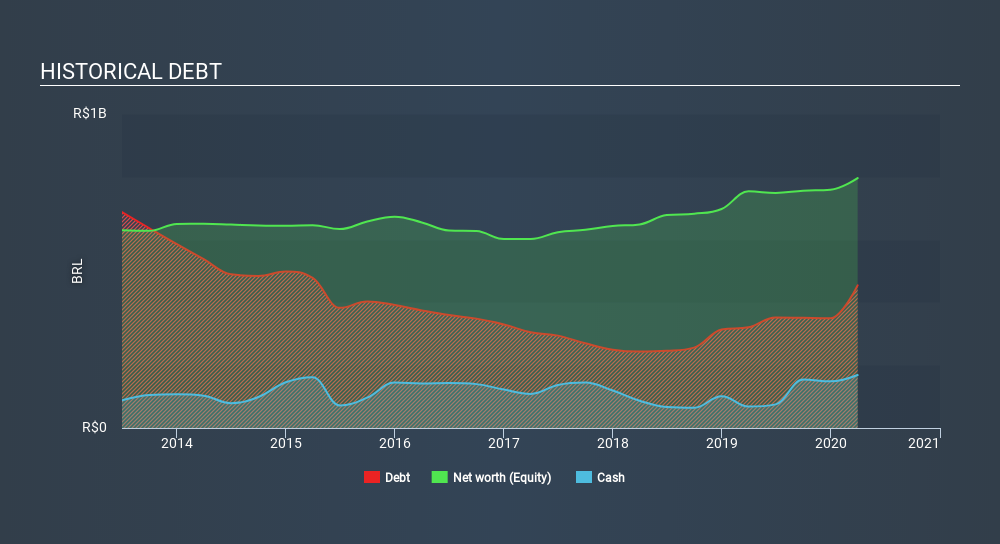

How Much Debt Does Indústrias Romi Carry?

The image below, which you can click on for greater detail, shows that at March 2020 Indústrias Romi had debt of R$454.1m, up from R$320.8m in one year. On the flip side, it has R$168.7m in cash leading to net debt of about R$285.4m.

A Look At Indústrias Romi's Liabilities

The latest balance sheet data shows that Indústrias Romi had liabilities of R$516.8m due within a year, and liabilities of R$228.9m falling due after that. Offsetting these obligations, it had cash of R$168.7m as well as receivables valued at R$276.3m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by R$300.8m.

While this might seem like a lot, it is not so bad since Indústrias Romi has a market capitalization of R$878.1m, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Indústrias Romi has a debt to EBITDA ratio of 3.5, which signals significant debt, but is still pretty reasonable for most types of business. However, its interest coverage of 1k is very high, suggesting that the interest expense on the debt is currently quite low. Pleasingly, Indústrias Romi is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 120% gain in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Indústrias Romi's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Indústrias Romi actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Indústrias Romi's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. Zooming out, Indústrias Romi seems to use debt quite reasonably; and that gets the nod from us. While debt does bring risk, when used wisely it can also bring a higher return on equity. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 4 warning signs for Indústrias Romi that you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Indústrias Romi, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:ROMI3

Romi

Develops, manufactures, and sells machine tools, plastic processing machines, and cast parts.

Moderate risk with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8228.9% undervalued

42 followersusers have followed this narrative

4 commentsusers have commented on this narrative

28 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6435.3% undervalued

30 followersusers have followed this narrative

4 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Hitit Bilgisayar Hizmetleri ·

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

Fair Value:₺61.1531.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22090.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

WealthAP on Alibaba Group Holding ·

BABA Analysis: Buying the Fear, Holding the Cloud

Fair Value:US$187.0417.4% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.4% undervalued

70 followersusers have followed this narrative

13 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.9% undervalued

1027 followersusers have followed this narrative

6 commentsusers have commented on this narrative

29 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25411.3% overvalued

71 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative