Advertisement

Is Harrisons Malayalam Limited's (NSE:HARRMALAYA) 11% ROE Better Than Average?

Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). To keep the lesson grounded in practicality, we'll use ROE to better understand Harrisons Malayalam Limited (NSE:HARRMALAYA).

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Harrisons Malayalam

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Harrisons Malayalam is:

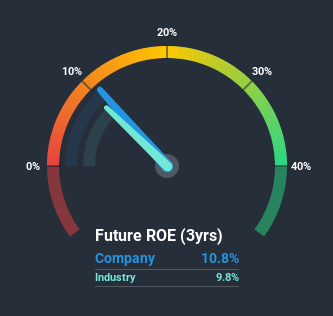

11% = ₹85m ÷ ₹789m (Based on the trailing twelve months to June 2020).

The 'return' is the income the business earned over the last year. So, this means that for every ₹1 of its shareholder's investments, the company generates a profit of ₹0.11.

Does Harrisons Malayalam Have A Good Return On Equity?

Arguably the easiest way to assess company's ROE is to compare it with the average in its industry. Importantly, this is far from a perfect measure, because companies differ significantly within the same industry classification. You can see in the graphic below that Harrisons Malayalam has an ROE that is fairly close to the average for the Food industry (9.8%).

So while the ROE is not exceptional, at least its acceptable. Although the ROE is similar to the industry, we should still perform further checks to see if the company's ROE is being boosted by high debt levels. If so, this increases its exposure to financial risk. You can see the 2 risks we have identified for Harrisons Malayalam by visiting our risks dashboard for free on our platform here.

Why You Should Consider Debt When Looking At ROE

Companies usually need to invest money to grow their profits. That cash can come from issuing shares, retained earnings, or debt. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt required for growth will boost returns, but will not impact the shareholders' equity. That will make the ROE look better than if no debt was used.

Harrisons Malayalam's Debt And Its 11% ROE

Harrisons Malayalam clearly uses a high amount of debt to boost returns, as it has a debt to equity ratio of 1.29. Its ROE is quite low, even with the use of significant debt; that's not a good result, in our opinion. Investors should think carefully about how a company might perform if it was unable to borrow so easily, because credit markets do change over time.

Summary

Return on equity is useful for comparing the quality of different businesses. Companies that can achieve high returns on equity without too much debt are generally of good quality. All else being equal, a higher ROE is better.

Having said that, while ROE is a useful indicator of business quality, you'll have to look at a whole range of factors to determine the right price to buy a stock. The rate at which profits are likely to grow, relative to the expectations of profit growth reflected in the current price, must be considered, too. So I think it may be worth checking this free this detailed graph of past earnings, revenue and cash flow.

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

When trading Harrisons Malayalam or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Harrisons Malayalam might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:HARRMALAYA

Harrisons Malayalam

Harrisons Malayalam Limited plants and sells tea and rubber in India and internationally.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This Gold Stock Could Triple if Its Gold Resource Grows

Fair Value:CA$466.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9720.3% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$23.861.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on CSG ·

CSG represents a high-quality industrial compounder operating in a structurally growing and geopolitically reinforced market,

Fair Value:€3037.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

artoflosing on BlackBerry ·

Accidental transformation from Phones to Physical AI.

Fair Value:CA$16.2228.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Andean Silver ·

Andean Silver, This ASX Silver Restart Story Smart Money is Loading Up On (111Moz AgEq + Ready Infrastructure)

Fair Value:AU$32.5793.6% undervalued

14 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.1% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6120.0% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative